US equity markets seem to regain their confidence

JPY continues to weaken against the USD

The USD lost some ground yesterday yet seems to be back in the greens during today’s late Asian session. In the Far East JPY continued to lose ground against the USD, despite the weakening of the USD in the FX market, reaching levels not seen since 1986. Meanwhile, the rhetoric from Japan remains hawkish as it seems ready to intervene in the market to JPY’s rescue yet the effect of the last market intervention was short lived. Should there be a market intervention operation we may see USD/JPY tumbling.

US equities seem to regain their confidence

US equities ended their day largely higher in yesterday’s session with the Consumer Goods, Technology and Industrials sectors leading the way upwards. Characteristically Dow Jones, Nasdaq and S&P 500 ended their day in the greens, as the market’s confidence seems to be enhanced. Should we see the positive, risk on approach by the markets be maintained we may see US equities rising further.

Oil prices show low volatility but market sentiment remains bearish

Oil prices tended to edge lower yesterday yet the overall picture tends to resemble mostly stabilisation. Oil traders are keeping a close eye on the US-Iran negotiations in Doha, while at the same time the ceasefire deal in place seems to remain fragile. Should we see the market’s hopes for a normalization of the oil market in the Gulf region we may see oil prices losing further ground.

Gold’s bearish tendencies remain

Gold’s price also edged lower yesterday and is preparing for the largest drop since 2013. Overall, the strengthening of the USD weighs on the precious metal’s price, with the Fed’s hawkish intentions feeding gold bears. Overall, the negative correlation of the USD to gold’s price seems to persist, thus any further strengthening of the USD could weigh on gold’s price and vice versa.

Other highlights for today

Today we get UK’s GDP rate for Q1, France’s and Germany’s preliminary HICP rates for June, Switzerland’s KOF indicator for June, Canada’s GDP rate for April, from the US we get the Chicago PMI figure, the consumer sentiment both for June, the JOLTS job openings figure for May and later on the API weekly crude oil inventories figure. On a monetary level, we note that ECB’s Elderson and Lane as well as the Cleveland Fed President Hammack are scheduled to speak. In tomorrow’s Asian session, we get Japan’s Tankan indexes for Q2, Australia’s building approvals for May and China’s Rating Dog manufacturing PMI figure for June.

Charts to keep an eye out

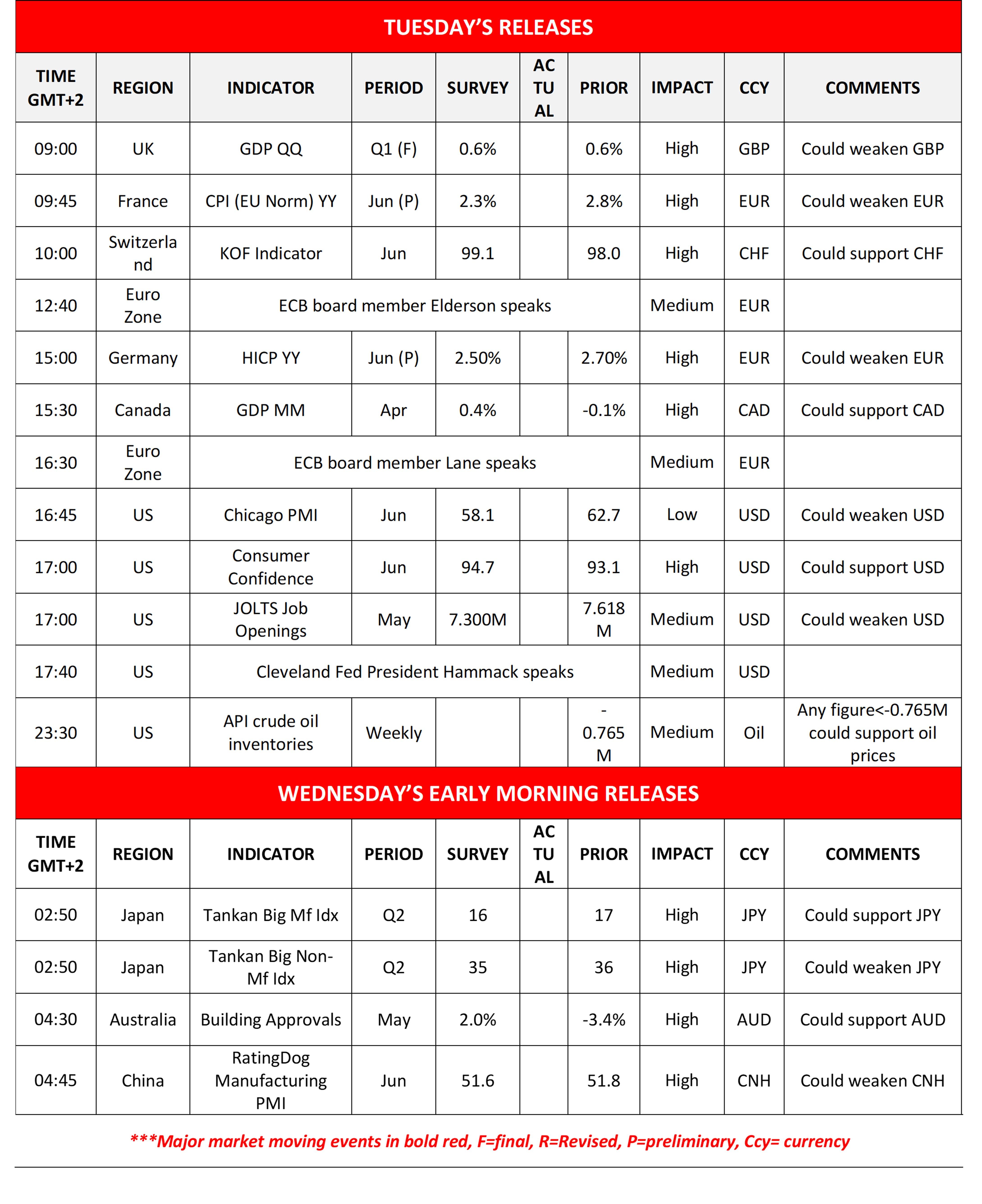

USD/JPY continued to edge higher placing more distance between its price action and the 160.50 (S1) support level. We remain bullish for the pair as the upward trendline remains intact, yet note that the RSI indicator has risen above the reading of 70, implying that the pair is at overbought levels and ripe for a correction lower. Should the bulls remain in charge, we may see the pair nearing the 164.40 (R1) resistance level. Should the bears take over, we may see USD/JPY breaking the upward trendline, the 160.50 (S1) support line and start aiming for the 157.50 (S2) support level.

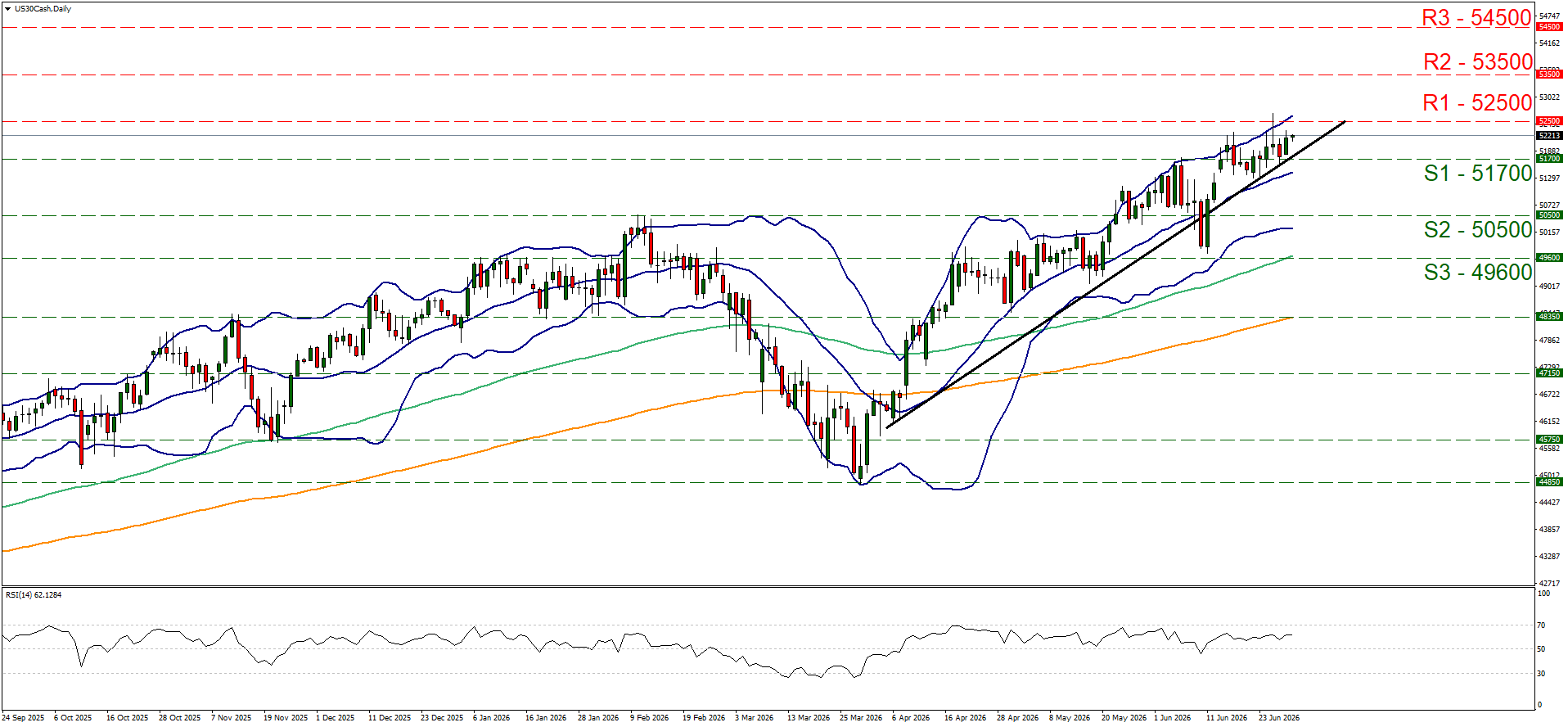

Dow Jones continued to rise yesterday aiming for the 52500 (R1) resistance line. We maintain our bullish outlook for the index given that the upward trendline continues to lead its price action. Should the bulls continue to lead the index as expected, we may see Dow Jones reaching if not breaching the 52500 (R1) resistance line. Should the bears take over, Dow Jones may break the prementioned upward trendline in a first signal of an interruption of the upward motion and continue to break also the 51700 (S1) support line, and start aiming for the 50500 (S2) support base.

USD/JPY daily chart

- Support: 160.50 (S1), 157.50 (S2), 155.00 (S3).

- Resistance: 164.40 (R1), 168.00 (R2), 171.60 (R3).

US30 cash daily chart

- Support: 51700 (S1), 50500 (S2), 49600 (S3).

- Resistance: 52500 (R1), 53500 (R2), 54500 (R3).

Author

Peter Iosif, ACA, MBA

IronFX

Mr. Iosif joined IronFX in 2017 as part of the sales force. His high level of competence and expertise enabled him to climb up the company ladder quickly and move to the IronFX Strategy team as a Research Analyst. Mr.