US Dollar Weekly Forecast: The Dollar pause that still feels like strength

- The US Dollar ended the week with marginal losses.

- Escalating geopolitical tensions continue to prop up the Greenback.

- Investors should keep their focus on US CPI and the FOMC Minutes.

The week that was

Looking at the weekly chart, the US Dollar (USD) has traded in a choppier, more volatile fashion, struggling to build on the strong gains seen the previous week.

As has been the case lately, markets have remained cautious, with uncertainty around the Middle East conflict still front and centre, compounded by the lack of a clear and consistent signal from the White House.

Against that backdrop, the US Dollar Index (DXY) has edged slightly lower, although it continues to hold comfortably above the key 100.00 psychological level.

The modest pullback in the Greenback has broadly tracked a softer tone in US Treasury yields across the curve, reflecting the back-and-forth nature of headlines surrounding the geopolitical situation.

Fed speakers: comfortable on hold, but inflation risks creeping back

This week’s Fed rhetoric leans toward patience, but with a subtle shift in tone. Policymakers are broadly comfortable with where rates are, yet they are increasingly aware that the inflation story, particularly through energy, is not fully behind them.

Powell and Williams anchored the centre. Both signaled that policy is in good shape and that there is no urgency to move. Inflation is still expected to return to target; the labour market is cooling but stable, and the Fed can afford to wait and watch how the data evolve.

But around that steady core, the message becomes more nuanced.

On one side, Miran struck a clearly dovish note, pushing back against inflation fears and pointing instead to signs of softening in the labour market. His message was simple: the Fed may already be doing enough, and there could be room to ease if conditions weaken further.

On the other side, Schmid and Logan kept the inflation debate alive. Both warned that price pressures may prove stickier than expected, especially if higher energy costs begin to feed through more broadly. Schmid, in particular, pushed back against the idea that inflation will smoothly glide back to 2%.

In between, Musalem and Goolsbee highlighted the growing complexity of the outlook. Policy is well-positioned, but risks are now clearly two-sided. Energy shocks, tariffs and geopolitical tensions are adding uncertainty, making it harder to find a clean policy path.

The common thread is clear.

The Fed is not rushing to act, but it won't declare victory over inflation.

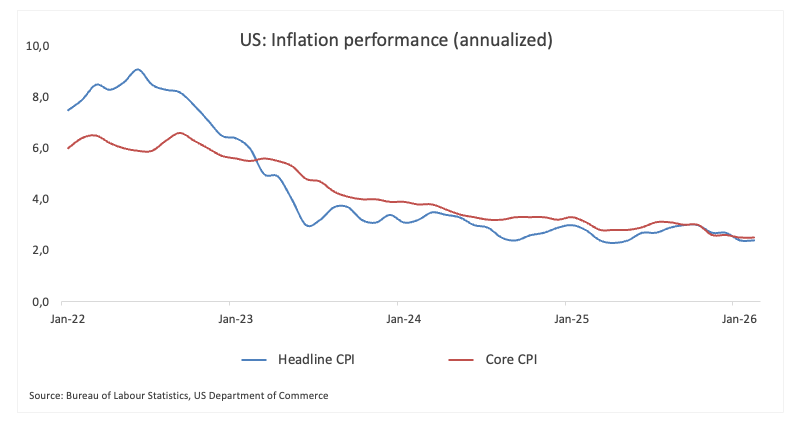

Inflation remains elevated

The US started the year with a slightly softer inflation backdrop. Headline Consumer Price Index (CPI) rose 2.4% YoY in February, matching January’s pace, while the core measure held steady at 2.5% YoY.

At first glance, that suggests inflation is moving in the right direction, even if it is still running above the Fed’s 2% target.

For markets, that has been enough to keep the disinflation narrative alive, gradually reviving expectations that rate cuts could come into view later on. But from the Fed’s perspective, this looks more like progress than victory, especially with the full impact of tariffs on prices still uncertain.

The Fed’s preferred gauge, the Personal Consumption Expenditures (PCE) index, tells a similar story, but with a slightly more cautious tone. January data showed inflation easing to 2.8% YoY from 2.9%, still comfortably above target.

Looking ahead, the inflation path could become more complicated. Rising Oil prices, driven by Iran’s closure of the Strait of Hormuz, risk feeding quickly into fuel and transport costs. If those pressures persist, the disinflation trend could start to look less straightforward in the months ahead.

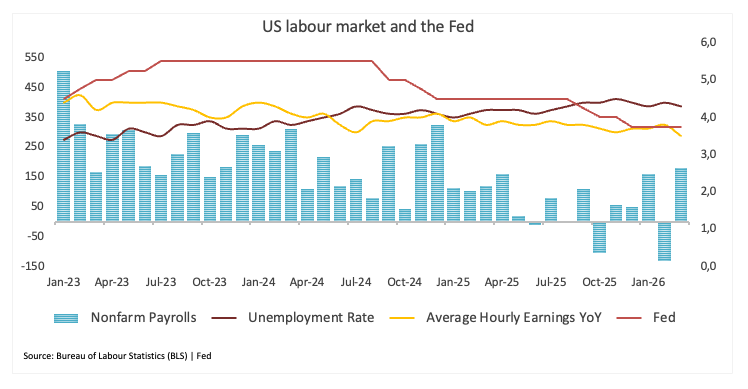

And the labour market gives no signs of further cooling

Indeed, the latest data from the Bureau of Labor Statistics (BLS) showed the economy added 178K jobs in March, crushing initial estimates and making for quite the reversal from February’s revised 133K drop. Adding to these figures, the Unemployment Rate ticked lower to 4.3%, while the Average Hourly Earnings, a proxy for wage inflation, rose 3.5% over the last 12 months, although easing from the previous month’s 3.8% reading.

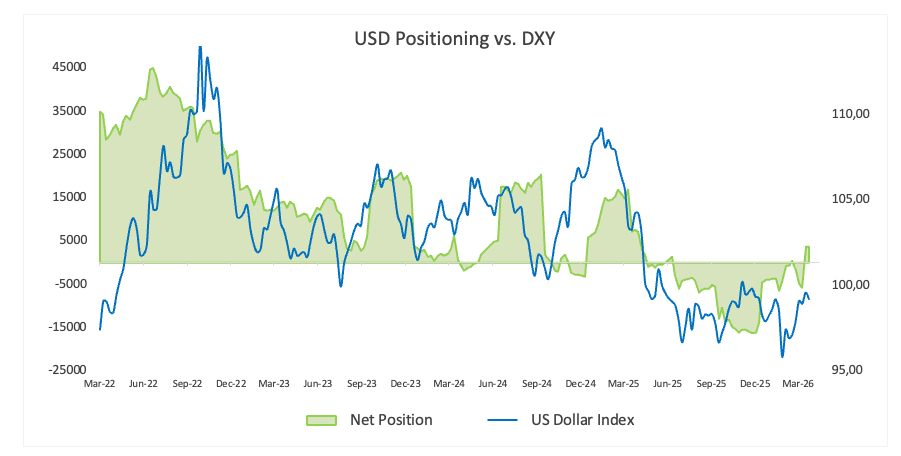

USD positioning: tentative rebuild of longs

The US Dollar is quietly regaining favour. After holding a small net short position earlier in the month, speculative accounts have flipped back into modest net longs, which have held broadly stable into the latest week.

At the same time, open interest has picked up, pointing to fresh positioning rather than just short covering. That shift fits perfectly with the broader resilience in the Greenback, supported by firm US yields and persistent geopolitical uncertainty.

The implication is that the Dollar may be in the early stages of a broader positioning rebuild. Although positioning is not yet stretched, the current trend reinforces the recent bullish price action and indicates that dips could begin to attract buyers more consistently, particularly if yields remain supported and risk sentiment remains fragile.

What’s next for the US Dollar

Next week, the US docket will be mostly focused on inflation, with the releases of prices tracked by the Consumer Price Index (CPI) and the Personal Consumption Expenditures (PCE). In addition, investors are expected to closely follow the publication of the FOMC Minutes after the hawkish hold at the March 18 meeting.

Bottom line

It is worth keeping in mind that the US Dollar’s rally, which began in late January, was initially driven by a run of stronger US data and a more consistent, steady message from the Fed.

That move gathered further momentum when President Trump nominated Kevin Warsh as Jerome Powell’s successor, a signal markets read as potentially less dovish than expected. Recently, rising geopolitical tensions have provided additional support, a dynamic that the recent FOMC meeting further reinforced.

At the same time, inflation remains just a bit too high for comfort. If the disinflation process starts to lose momentum, markets could quickly scale back expectations for early or aggressive rate cuts.

In that scenario, the Fed would likely double down on patience, maintaining a steady stance that could, over time, offer fresh support to the Dollar.

Fed FAQs

Monetary policy in the US is shaped by the Federal Reserve (Fed). The Fed has two mandates: to achieve price stability and foster full employment. Its primary tool to achieve these goals is by adjusting interest rates. When prices are rising too quickly and inflation is above the Fed’s 2% target, it raises interest rates, increasing borrowing costs throughout the economy. This results in a stronger US Dollar (USD) as it makes the US a more attractive place for international investors to park their money. When inflation falls below 2% or the Unemployment Rate is too high, the Fed may lower interest rates to encourage borrowing, which weighs on the Greenback.

The Federal Reserve (Fed) holds eight policy meetings a year, where the Federal Open Market Committee (FOMC) assesses economic conditions and makes monetary policy decisions. The FOMC is attended by twelve Fed officials – the seven members of the Board of Governors, the president of the Federal Reserve Bank of New York, and four of the remaining eleven regional Reserve Bank presidents, who serve one-year terms on a rotating basis.

In extreme situations, the Federal Reserve may resort to a policy named Quantitative Easing (QE). QE is the process by which the Fed substantially increases the flow of credit in a stuck financial system. It is a non-standard policy measure used during crises or when inflation is extremely low. It was the Fed’s weapon of choice during the Great Financial Crisis in 2008. It involves the Fed printing more Dollars and using them to buy high grade bonds from financial institutions. QE usually weakens the US Dollar.

Quantitative tightening (QT) is the reverse process of QE, whereby the Federal Reserve stops buying bonds from financial institutions and does not reinvest the principal from the bonds it holds maturing, to purchase new bonds. It is usually positive for the value of the US Dollar.

Author

Pablo Piovano

FXStreet

Born and bred in Argentina, Pablo has been carrying on with his passion for FX markets and trading since his first college years.