UK and EU come to an agreement, sterling rallies

Market Overview

Sterling has rallied as the UK seems to have come to an agreement with the EU that should allow them to move to the next stage of negotiations. Having had a false start at the beginning of the week, finally it seems as though a deal has been done. With Theresa May seemingly able to give assurances to Arlene Foster of the DUP that there will be no hard border either within the island of Ireland, or in the Irish Sea, it seems as though all sides are happy. The Irish government is now happy to vote for this deal. The Northern Ireland border has become the key sticking point of the three red lines for the EU (the others being the divorce bill and the rights of EU citizens in the UK). Now it seems that all sides are happy and the UK and the EU can now hopefully move on to the next phase of negotiations, trade talks. Sterling has been very reactive to progress in the negotiations but should now be underpinned by this news. The initial rebound last night on the rumours of a deal have turned into a bit of a choppy reaction today, but support seems to now be in place. In other news, the US Congress has agreed a two week extension of the US debt ceiling suspension which will give lawmakers further time to try and come to an agreement on the budget and raising the ceiling. It is also Non-farm Payrolls today. This is the final payrolls report in front of an expected rate hike by the FOMC at next week’s meeting. Key issues will be whether wage growth can begin to build again.

Wall Street found some support after a few days of declines, with the S&P 500 +0.3% at 2637, whilst Asian markets were positive again, with the Nikkei leading the way +1.4%. European markets are also positive today, but with sterling strength having come through, the FTSE 100 is an underperformer. In forex, there is a degree of dollar strength through the markets with the yen the main underperformer. In commodities, despite the dollar strength, gold has found support after sharp losses yesterday whilst oil is ticking slightly lower.

Non-farm Payrolls will be the big focus for traders today. The US Employment Situation report is released at 1330GMT and after two months of wild swings on the headline and wages will this be a month where the data begins to settle down again? If the ADP employment change is anything to go by then possibly so. The headline Non-farm Payrolls are expected to show +200,000 jobs created which would be down from +261,000 last month but above the six month average which is around +165,000. Average hourly earnings dropped to +2.4% year on year last month (from +2.9%), but the expectation is that monthly data will grow by +0.3% which would mean pulling the year on year higher to +2.5%. Look also for the Unemployment reading which is expected to remain flat having fallen to 4.1% last month whilst the U6 Underemployment dropped to 7.9%. If these unemployment rates continue to fall whilst average earnings fail to pick up this would be dollar negative. Participation rate also dropped back to 62.7% last month which was a disappointment with the six month average around 62.9%. Aside from payrolls, traders will also be looking for the prelim reading of Michigan Sentiment at 1500GMT which is expected to improve to 99.0 (from an upwardly revised 98.5 last month).

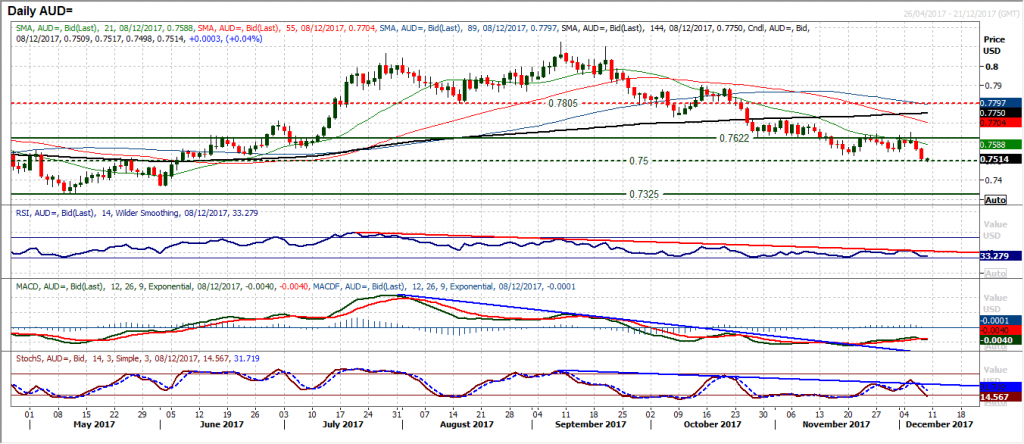

Chart of the Day – AUD/USD

The Aussie has come under significant corrective pressure in the days since GDP numbers missed expectations. Coupled with renewed US dollar strength, the move has resulted in a downside break below $0.7530 support to a new six month low. With a second consecutive strong bear candle yesterday, the market has now have broken down from a near term consolidation range between $0.7530/$0.7660 and continues what has been a strong move lower in recent months. The downside implied target of 130 pips implies $0.7400 whilst the historic pivot around $0.7500 is first to be tested. Rallies are now set to be sold into, with the hourly chart showing resistance in the range $0.7530/$0.7550 initially with negative configuration across the hourly indicators. The market seems to be consolidating this morning in front of payrolls, however with the downside break and renewed negative outlook, any volatility higher today should be used as a chance to sell.

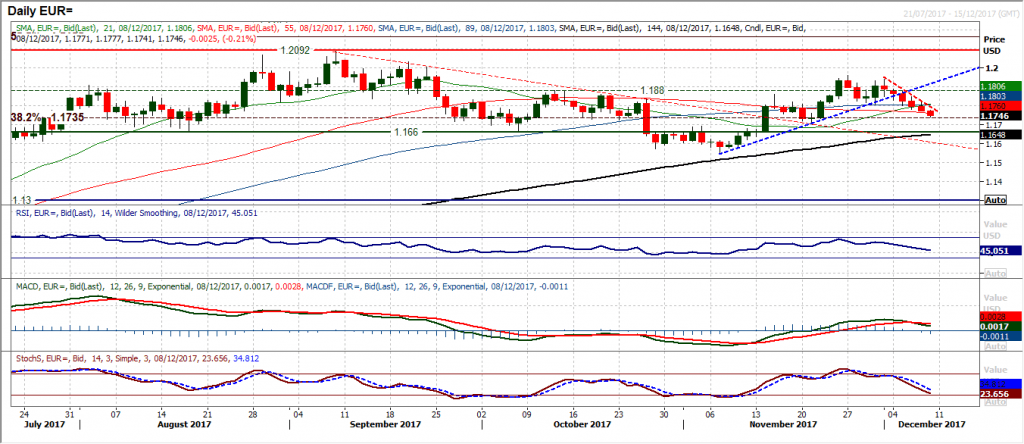

EUR/USD

The negative candles continue to rack up as the drift lower on EUR/USD continues. With a four week uptrend having been broken this week there is a new formation of a downtrend developing. This comes with the decisive breach of the previous support at $1.1807 and a move now seemingly towards the next reaction low at $1.1712. The momentum indicators are decisively corrective now with the MACD lines posting a bear cross, the RSI falling below 50 and the Stochastics tracking ever lower. This suggests that on a technical basis, rallies should be sold into now. The hourly chart shows yesterday’s high failing at $1.1815 whilst there is further resistance in the band $1.1830/$1.1850. The big caveat today is clearly Non-farm Payrolls which are likely to drive some volatility through the chart. However barring a terrible report the expectation is that the dollar strength will prevail.

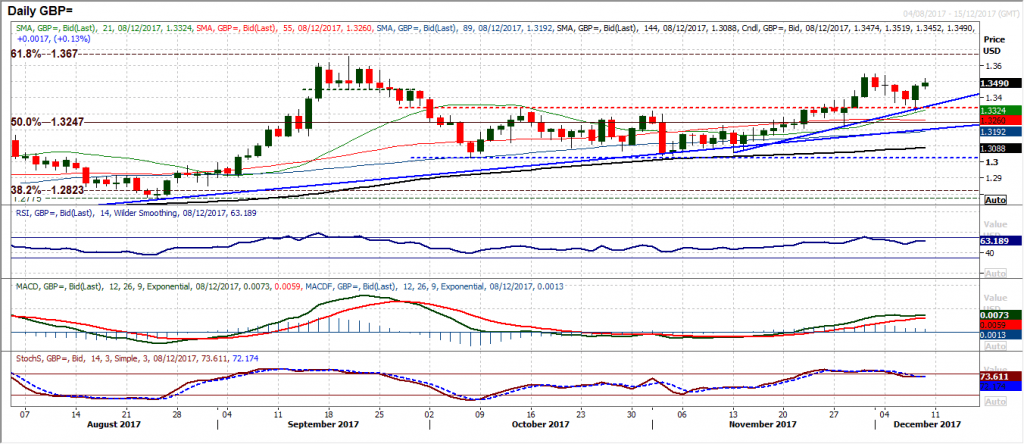

GBP/USD

Cable is highly politically driven as a pair currently. News this morning is that there has been a breakthrough in the UK’s negotiations with theEU and a deal has been done that should allow the UK to move on to the next phase of negotiations (trade talks). The success or failure of the UK’s Brexit negotiations have been having directional impact on sterling recently. The position has improved markedly in the past 24 hours with suggestions of progress and subsequently Cable has rallied. Having confirmed this it should help to underpin sterling now. On a technical basis the rebound yesterday formed a bullish engulfing candle and has improved the near term outlook no end. The corrective slip of the past few days seems to have been settled and reversed, interestingly around the old breakout support at $1.3335 (yesterday’s low was $1.3318) and also the support of what is coming up to be a four week uptrend. The daily momentum indicators have ticked higher again and the corrective configuration on the hourly technical studies has been reversed. There is support in the band $1.3400/$1.3450, whilst the recent high at $1.3550 is back in sight again. Payrolls will add to the volatility today but for now the sterling strength is back on.

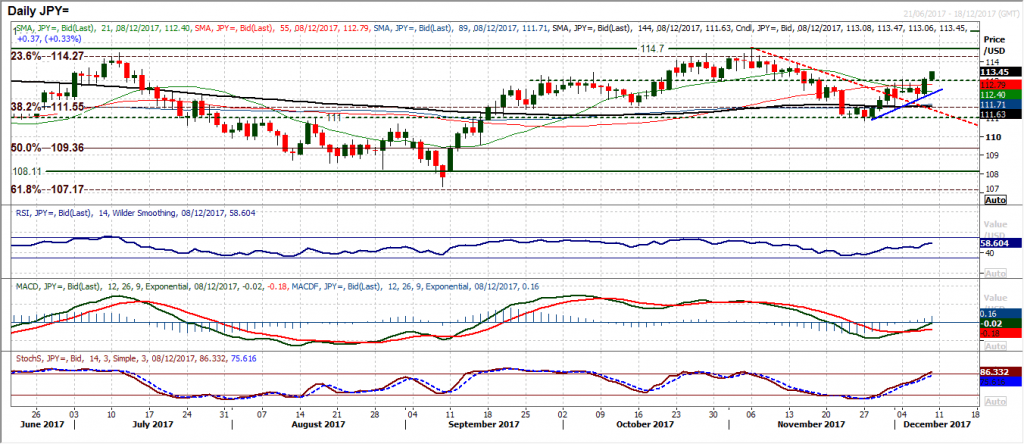

USD/JPY

With risk appetite seemingly on a more sure footing, the yen is underperforming and the dollar bulls are pulling a far more positive outlook once more. The minor blip on USD/JPY mid-week has been long forgotten now with yesterday’s strong bull candle and the further gains today which have taken the market decisively above the near to medium term pivot around 113.00. This now means that the resistance band from the nine month range 114.25/114.70 is back into play. This comes with the momentum indicators significantly improving, as the MACD lines have crossed higher and the Stochastics rise strongly. This would suggest that any volatility on payrolls today that might pull the pair back to find support in the area between the 113.00 pivot and what is now building as a two week uptrend at 112.30 should be seen as a chance to buy. The next resistance is a minor lower high at 113.90 before getting into the nine month range resistance again.

Gold

There has been a hugely decisive breakdown of the 10 week range as yesterday’s strong bear candle has not only closed below the key October low at $1260 but also the next support at $1251. There seems to have been a key shift out of gold in the past few days as risk appetite has improved. This key breakdown below $1260 completes a $40 breakdown of a trading range an implies $1220 at least now in the coming weeks. Rallies will be seen as a chance to sell. The old support band $1251/$1260 will also become an area of resistance now. The momentum indicators are taking a deterioration with the MACD lines gaining downside traction and the Stochastics in negative territory, whilst the RSI in the low-30s is at its lowest level since July. The market looks a touch settled this morning ahead of payrolls but any rebound is likely to be met with selling pressure now. The initial support is at $1243.

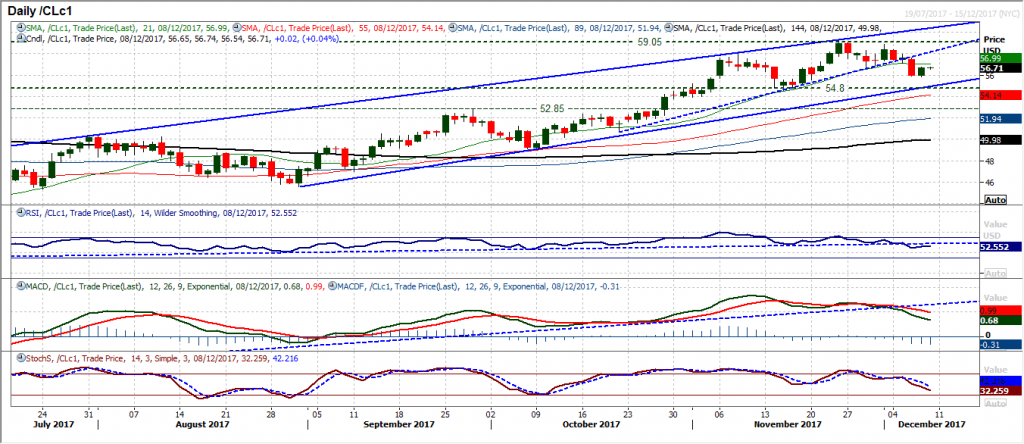

WTI Oil

Having broken below $56.75 and forming near term lower highs and lower lows, the market looks to be turning more corrective within the medium term uptrend channel. The reaction to rallies will be key to this outlook continuing and is why watching the reaction to yesterday’s positive candle will be very interesting. Medium to longer term momentum uptrends have been broken and the MACD and Stochastics lines are in decline now. The old support band at $56.75/$57.10 is now a near term zone of overhead supply and the hourly chart shows yesterday’s rebound is simply unwinding negative momentum. A failure on the hourly RSI around 60 and MACD lines below neutral would be seen as a sell signal. Yesterday’s low at $55.80 is now initial support, whilst the trend support comes in around $54.80 today.

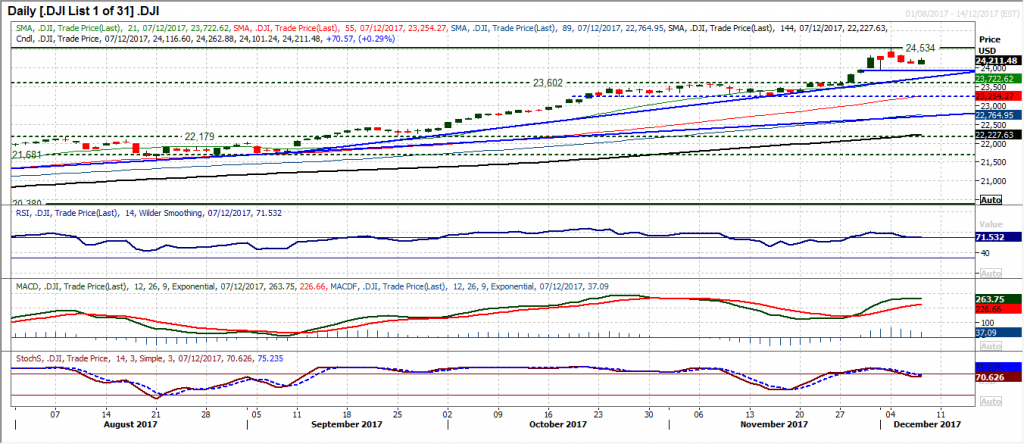

Dow Jones Industrial Average

After falling over in recent sessions, the bulls found a degree of support yesterday to post a positive session. This has formed a positive candle that has settled the near term corrective momentum, at least for now. It is interesting to see the daily RSI still holding up above 70 but it is too early to say whether this is sustainable support coming in. Corrections within the three month uptrend remain an opportunity to buy but until the market begins to put together a run of positive candles it is difficult to ascertain the strength of the support. The hourly chart offers some encouragement though with the RSI having unwound to find support at 40, whilst the MACD lines are looking to bottom around neutral. A move above 24,230 would improve the outlook with a push above 24,277 subsequently adding to momentum signals that are picking up now. The support at 24,101 is initially now protecting 23,922 and the uptrend around 23,770.

Author

Richard Perry

Independent Analyst