Türkiye’s fight to save the Lira comes at a high cost

Türkiye is once again in a spot nobody likes to be: defending its currency while trying to avoid crushing its economy with higher interest rates. With inflation risks rising due to higher Oil prices and investors increasingly questioning the country’s strategy, the cost of protecting the Lira may be too high to handle.

Risk-sensitive emerging market assets have come under heavy selling pressure from early March as the beginning of the conflict in the Middle East triggered an intense flight to safety. Türkiye hasn’t been an exception.

Although recent data point to a recovery in demand for these types of assets, Türkiye might find it difficult to shake off the impact of the US-Iran war on its economic state. Citing data published by the Institute of International Finance, Reuters reported that “emerging market portfolio flows - the balance of bond and stock market buying and selling - rebounded to $58.3 billion in April, reversing most of the $66.2 billion outflow in March when the escalating Middle East conflict rattled markets.”

Draining reserves to avoid raising interest rates

The Central Bank of the Republic of Türkiye’s (CBRT) official Balance of Payment Developments report showed that Türkiye’s official reserves declined by $43.4 billion in March, marking the biggest one-month decline on record.

Moreover, an analysis conducted by Metals Focus suggested that the CBRT sold 52 tonnes of Gold between February 27 and March 27, dragging net central bank holdings to the lowest level in over two years at 440 tonnes. The Financial Times said that the CBRT also “arranged about 79 tonnes of Gold swaps” in this period. At current prices, the combined sales and swaps amounted to nearly $20 billion worth of Gold. At the end of April, 31 tonnes of Gold returned to CBRT’s reserves as a 1-month USD-Gold swap matured, the central bank data showed.

These actions taken by the CBRT highlight the fragility of the Turkish economy and how attentive the central bank must be to limit the depreciation of the Turkish Lira (TRY) and avoid a deanchoring of inflation expectations. Still, the TRY lost nearly 3% against the US Dollar (USD) since the beginning of the conflict, lifting USD/TRY to a new all-time high near 45.60.

CBRT Governor Fatih Karahan announced on May 14 that they have paused providing inflation forecast ranges due to the environment of high uncertainty amid the Iran war. While presenting the central bank’s quarterly inflation report, which showed the year-end inflation forecast was revised higher to 26%, Karahan acknowledged that the direction of the medium-term inflation outlook is not clear and noted that even though their policy stance has not changed, they have the flexibility with the rate corridor when risks are on the upside.

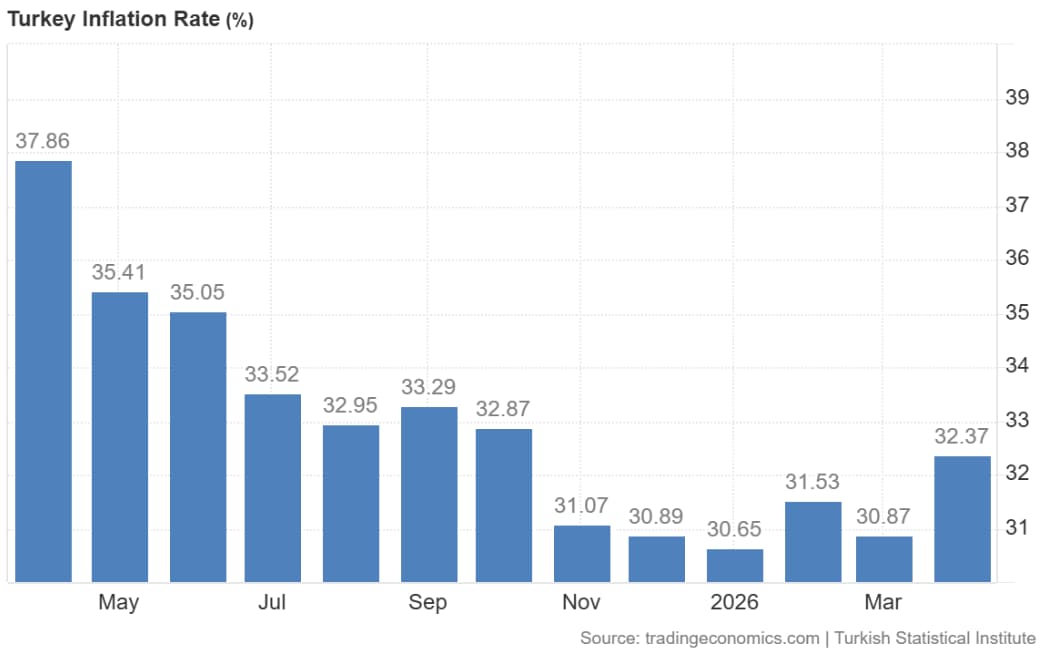

Türkiye’s inflation rate accelerated in April to the highest reading since October 2025.

A “shadow” hike

While classical theory dictates a binary choice between explicit rate hikes or currency depreciation, the CBRT chose a more nuanced approach in March by keeping the policy rate unchanged and avoiding a potential political backlash. While maintaining the interest rate at 37.0%, the central bank decided to halt traditional one-week repo auctions on March 1, practically forcing commercial banks to source liquidity from the upper band of its corridor.

This action was assessed as a hidden tightening mechanism that raised the effective interbank reference rate up to 40.0%. Combined with the liquidation of foreign exchange and Gold reserves, the CBRT managed to absorb the initial shock from the Middle East crisis.

Is there any upside potential for the Turkish Lira?

By controlling the rate of increase in USD/TRY exchange rate and keeping it below domestic inflation, the CBRT aims to make the TRY stronger in real terms and reduce imported inflation. In the quarterly inflation report, the CBRT raised its average Brent Oil price forecast for 2026 to $89.4/bbl from $60.9. In case the Middle East conflict prolongs and Oil prices settle at higher levels, the 26% inflation rate by year-end might be difficult to achieve.

Another upward revision to inflation projections could suggest that the CBRT might allow USD/TRY to rise at a faster pace than currently estimated, since that is the threshold the exchange rate needs to be below for the real appreciation of the TRY to continue.

In summary, CBRT’s policy rate could be obsolete in trying to project where USD/TRY might land at the end of the year. Instead, inflation projections could provide the real clue to how much the central bank is willing to allow the TRY to depreciate.

Not all analysts are convinced the CBRT’s unusual methods will hold the line. Commerzbank’s Tatha Ghose noted that their worst-case scenario for the TRY materialised after the CBRT opted to FX intervention and ad hoc liquidity tightening instead of raising rates after the April policy meeting.

“Core inflation momentum remained far too high, and the improvement in the current account had begun to reverse as policy had been eased prematurely. In that context, the war simply exposes an already weakening framework rather than creating a fundamentally new problem," Ghose explained and warned that this structural vulnerability is highly likely to yield renewed pressure on the local currency moving forward:

"This situation is likely to be followed by renewed pressure on the Lira and a more noticeable rate of depreciation. The annualized rate of depreciation since the beginning of April works out to 47%. We expect USD/TRY to reach 55.0 by year-end, compared with market expectations of around 52.0."

Türkiye’s central bank is used to hard choices. This time, the CBRT’s room to maneuver is shrinking.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

FXStreet Team

FXStreet

Composed of a group of economic journalists and FX experts, the FXStreet content team produces and oversees all content published on FXStreet. It provides a purely journalistic approach to the Forex market.