The VIX gained 28% on the day as equities fell

Highlights:

Market Recap: The VIX gained 28% on the day as equities fell. The S&P 500 was down -2.41% finishing at 2811.87. The weakness in equities occured as trade tensions continued to heat up. The US 10 Year yield dropped -7 basis points, closing at 2.40%. Gold closed up 1.12% finishing above $1300 per ounce.

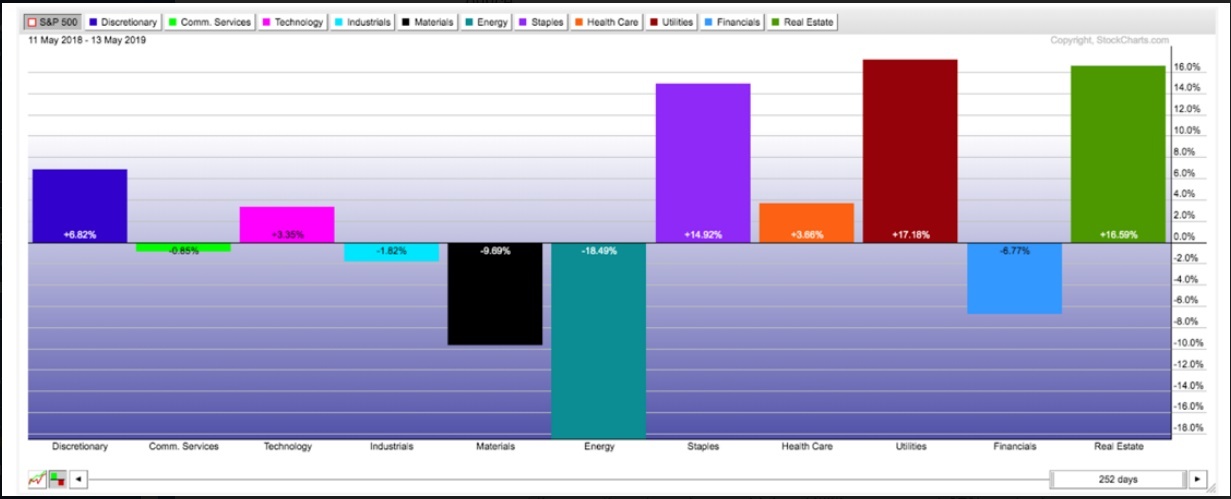

Sectors: Over the last 12 months, utilities are the strongest sector relative to the S&P 500. Utilities have outperformed the S&P 500 by over 17%. REITs and staples have also outperformed by a healthy margin (16.59% and 14.92%). Energy is the worst performer relative to the S&P 500.

Utilities: Utilities continue to show strong relative strength and remain in a positive trend. Momentum has weakened considerably since the start of the year, yet they continue to make new highs. Utilities were up 1.07% yesterday despite the market being down over -2%.

REITS: The real estate sector is close to breaking out to new highs relative to the S&P 500 (XLRE:SPY). This would suggest a potential defensive rotation within the equities markets. REITs are near all time highs on an absolute basis. REITs gained 2.58% against the S&P 500 yesterday.

Technology: After leading the way up this calendar year, technology is also leading the way down. The technology sector (XLK) dropped -3.77% yesterday. The sector is still in a positive trend relative to the broad market; however, momentum has weakened considerably as of late.

Semiconductors: Semiconductors were early leaders in the stock market rally. Relative to the S&P 500, semiconductors bottomed ahead of the market in late 2018. They also broke to new highs before the broad market indices. Now they are breaking through support on the downside. This is not encouraging, especially since earnings comparables will be tough in the second and third quarter on a year over year basis. Early indications suggest that this sector could come under pressure. Does this mean that the market will follow?

Futures Summary:

News from Bloomberg:

Donald Trump buoyed markets, at least for now, saying he'll meet Xi Jinping at the G-20 in June and musing that he has a feeling the talks may be "very successful." Even so, his team unveiled a list of about $300 billion of Chinese goods including kids' clothes, toys, mobiles and laptops that he's threatened to whack with a 25% tariff. Trump also cautioned China against "substantial" retaliation.

The tariffs are already starting to increase inflation and will have a greater impact as they go up, New York Fed chief John Williams said on Bloomberg TV. Tariffs act like a negative supply shock on the U.S. and the inflation effect could be significant. Central banks around the world should prepare for a future of slow economic growth and low interest rates, he also said at an event in Zurich.

Uber rose pre-market as questions are flying after its 18% decline in the first two days of trading: Why did bankers including Morgan Stanley's suggest a $120 billion valuation last year that Uber couldn't deliver? Did the banks set the IPO's price too aggressively? And did they steer too much stock to big investors who made hollow pledges to hold it long term? The debate is complicated by the trade war and Lyft's poor performance.

Bayer lost its third Roundup trial, sending shares down in Frankfurt. A California jury awarded more than $2 billion to a couple who said they got cancer from using the Monsanto weedkiller. While the amount will probably shrink, it may bump the potential settlement value on the remaining 13,400 cases to as high as $10 billion, Bloomberg Intelligence said. Bayer plans to appeal. Here's a QuickTake on the Roundup trials.

The global stock selloff mostly subsided, with U.S. equity-index futures rising along with European shares. Asian equities posted moderate losses, dragged down by China and Hong Kong, which re-opened after a holiday. The yuan was mostly steady. The yen, gold and Treasuries all fell. Oil slipped. Most industrial metals rose.

Author

Clint Sorenson, CFA, CMT

WealthShield