The UK inflation numbers aren’t as bad as they look

Services inflation, which rose much further than expected, was driven by a big change in road tax and the timing of Easter. It should fall back from April’s 5.4% figure to the 4.5% area this summer, keeping the Bank of England on track for quarterly rate cuts through this year and into 2026.

The latest UK inflation data puts the final nail in the coffin of a Bank of England rate cut in June, though of course that already looked highly unlikely.

Headline inflation rose by almost a full percentage point between March and April to 3.5%. Much of that was down to the well-advertised rise in household energy and water bills. But crucially for the BoE, services inflation surged too, from 4.7% to 5.4% in April. Remember, this is the part of the inflation basket that the BoE cares most about. And this was a much larger pick-up than we or the Bank had expected.

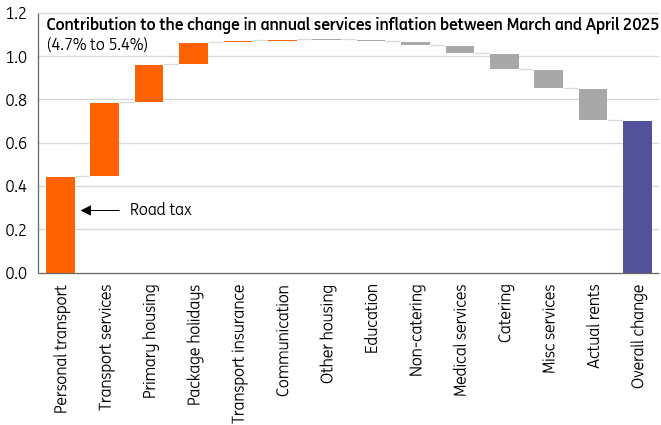

When you drill into it, though, the rise doesn’t look nearly as problematic as it might at first glance. We calculate that half of that change was solely down to the rise in road tax – the contribution from “personal transport” services rose by 0.5ppt. That will stick around for the next 12 months, then drop out of the annual comparison. The Bank of England will almost certainly ignore this, as it does with changes in other taxes like VAT.

The rise in services inflation was down to road tax and the timing of Easter

Source: Macrobond, ING calculations

Aside from road tax, the remainder of the latest increase in services inflation can be almost entirely accounted for by air fares and package holidays, both of which were affected by the timing of Easter. Last year, Easter was in March, which skewed the annual rate of change. But the day these prices were collected this year fell right before Good Friday itself, which is unusual. In other words, the rise in plane tickets – 28% on the month – was even more exaggerated than usual. This will drop out over the next few months.

As we wrote yesterday, the news on services inflation should be about to get much better. Away from road tax and travel, several other key areas saw further disinflation in April. Restaurants/cafes, medical care services and rents all saw their respective rates of annual inflation fall.

Rent is particularly interesting because it is contributing a full percentage point to services inflation right now, but that contribution is set to halve by the start of next year. That’s partly because the government cap on social housing costs is much lower this year than last.

More generally, surveys show that pricing power is ebbing away. We expect services inflation to fall back to the 4.5% area this summer and lower still in 2026, when things like road tax drop out of the annual comparison.

That’s still too high for many of the Bank of England’s rate-setters, which is why we have long argued policymakers are unlikely to speed up the pace of easing this year. But we think an August cut is still highly likely, and the quarterly pace of rate cuts can continue through this year and into 2026.

Read the original analysis: The UK inflation numbers aren’t as bad as they look

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.