The lockdown could start to be a thing of the past, but the impact on the economy will be permanent

Barclays CEO Jes Staley reckons that after Covid-19 the idea of sticking thousands of people in a building may be a thing of the past. I heartily agree. Working from home is clearly working rather well. Also, banks are no doubt looking at this and thinking they can cut costs by closing offices, call centres and branches. Nevertheless, it highlights how bosses and government have a very hard task in exiting lockdown. Moreover, what about the Pret or the pub that depends on lunch trade from the City workers filling up these offices every day? The impact on the economy will be permanent.

Shares in Barclays popped over 5% despite the lender taking a £2.1bn credit impairment charge, five times the level of a year before. Like its US peers, trading revenues soared by 77% but this offset may be a one-off for banks as volatility returns to more normal levels. Shares were due a rally - they’ve been beaten down so much and haven’t really participated in the upturn. Investors may need to wait for dividends but UK banks could be in much better shape their share prices indicate.

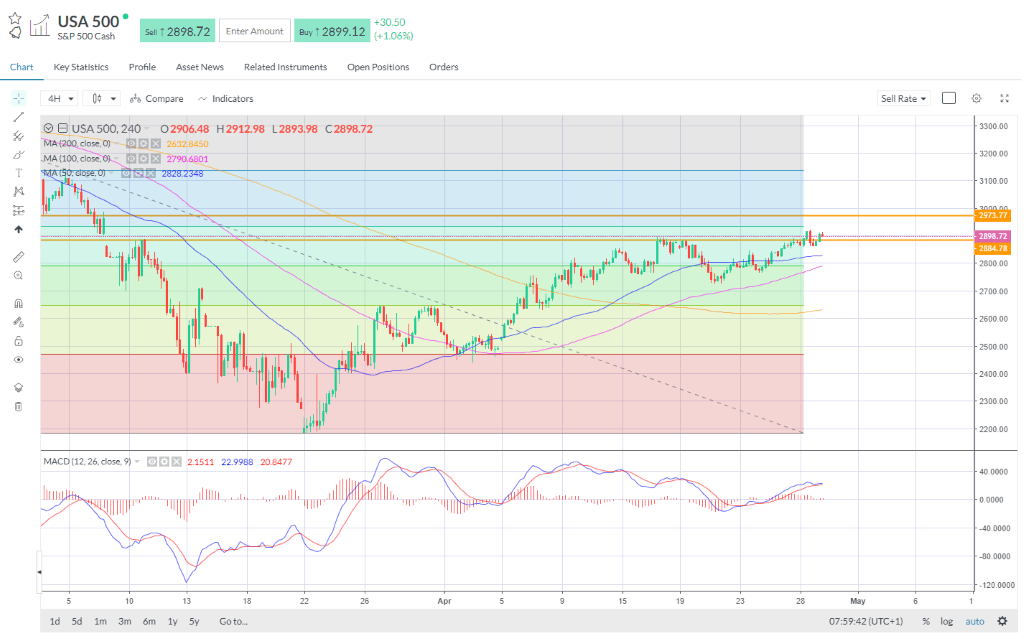

The S&P 500 failed a major test yesterday as bulls stumbled amidst a blitz of earnings releases and doubts about oil prices. The broad index rallied on the open to trade above 2900 but closed lower and crucially below the key 2885 resistance at 2,863, forming a dark cloud cover bearish signal.

Futures though are higher again today, but we will need to see these levels broken decisively on a close before we consider a push to the 61.8% retracement of the drawdown at 2934. For that we will look to earnings and the US advanced GDP print – seen at -4% - but more importantly the messaging from the Fed today will be crucial for sentiment in equity markets.

Asian markets were broadly firmer overnight with traders expecting the Fed to make clear it will not remove any accommodation until the threat from Covid-19 has passed.

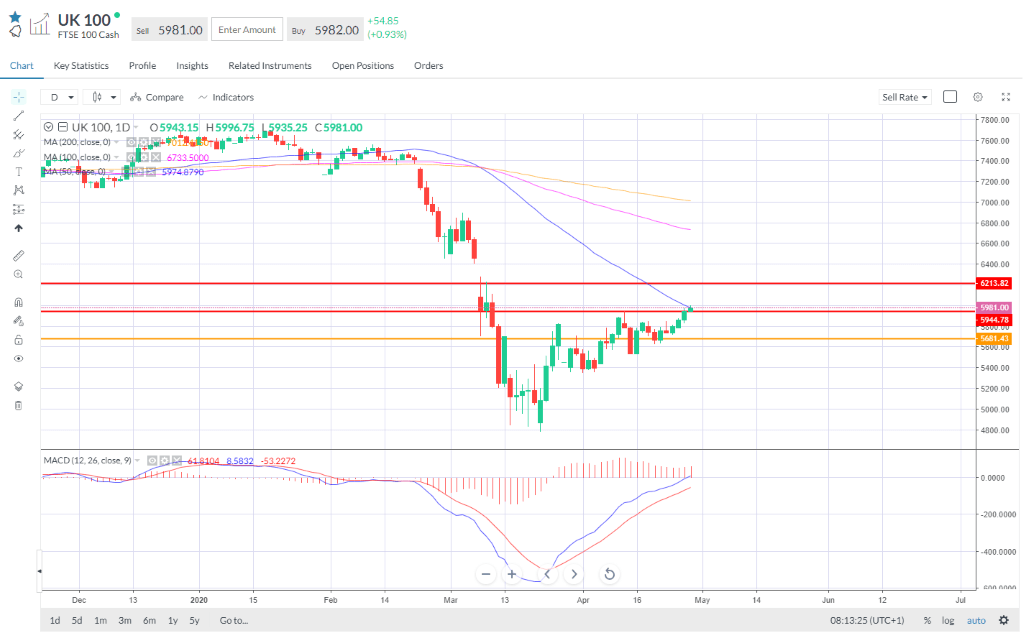

European indices opened strongly, building a very solid session on Tuesday that saw the FTSE 100 rally almost 2% and close above the Apr 14th swing high, but then we saw weakness creep in after half an hour’s trading outside of the UK market, which looks pretty solid as it taps on 6,000.

Italian bonds have softened after Fitch cut the country’s debt to one notch above junk. This unscheduled move followed S&P affirming Italy’s status but with a negative outlook. The yield on Italian 10-year BTPs spiked to 1.83%, the highest since Friday, and it just causes a little added worry for the ECB ahead of its meeting tomorrow. BTP-Bund spreads widened.

Alphabet dealt with a sharp decline in ad revenue growth in the first quarter as a result of the Covid-19 outbreak and lockdown measures that are stifling consumer spending, but management pointed to a rebound in April and outline spending cuts that sent shares up 8% after hours.

The fact that Alphabet sees ‘some signs users are returning to normal behaviour’ does not in itself mean the global economy is anywhere near to normal. Alphabet is one of the best placed companies to grow out of the crisis and should benefit from consumers increasing screen time in lockdown and no doubt growing digital ad spend as economies recover in the latter part of 2020 and through 2021. Structural shifts boosting digital ad growth that Covid-19 is accelerating will also be factor. Facebook and Microsoft report today.

Elsewhere, front month WTI bounced off the lows after testing $10 to move up through $14 by the European session open. API data showed inventories rising almost 10m barrels in the week to Apr 24th, but this was lower than estimates. As ever we are looking at the EIA figures with more interest. A slowing in inventory builds from the +15M we’ve seen in the last three weeks can be expected as we reach tank tops at Cushing. Expect volatility in the front month WTI to be very high until expiry.

Charts

S&P 500 looks to clear key resistance again, still worried about rolling over

FTSE 100 looks to breakout of recent range, taking out the horizontal resistance and looking to breach 6,000 but first it’s got the 50-SMA to deal with.

Author

Neil Wilson

Markets.com

Neil is the chief market analyst for Markets.com, covering a broad range of topics across FX, equities and commodities. He joined in 2018 after two years working as senior market analyst for ETX Capital.