The international energy agency says “demand for gasoline has peaked”

Gasoline demand is down 10% from a year ago and is unlikely to ever surpass the record usage in 2019.

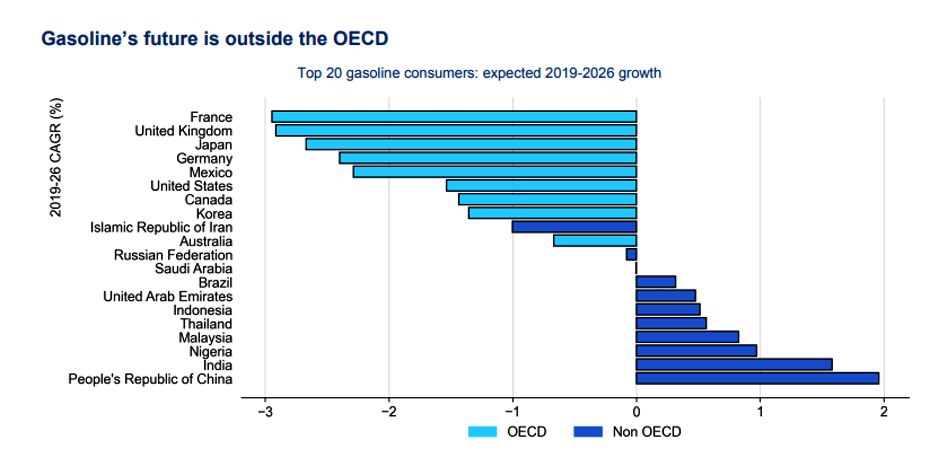

Peak Gasoline usage

The IEA Oil Forecast shows gasoline demand has peaked but overall oil demand is another matter.

The speed and depth of the recovery is likely to be uneven both geographically and in terms of sectors and products. Gasoline demand is unlikely to return to 2019 levels, as efficiency gains and the shift to electric vehicles eclipse robust mobility growth in the developing world. Aviation fuels, the hardest hit by the crisis, are expected to slowly return to 2019 levels by 2024, but the spread of online meetings could permanently alter business travel trends.

In the current policy environment, US production growth is set to resume as investment and activity levels pick up in tandem with rising prices. Yet any increase is unlikely to match the lofty levels of the recent past.

Global oil demand, still reeling from the effects of the pandemic, is unlikely to catch up with its pre-Covid trajectory. In 2020, the start of our forecast period, oil demand was nearly 9 mb/d below the level seen in 2019, and it is not expected to return to that level before 2023.

Further fuel efficiency improvements, increased teleworking and reduced business travel, much stronger electric vehicle penetration and new policies to curb oil use in the power sector and more recycling could reduce oil use by as much as 5.6 mb/d by 2026, which would mean that oil demand never gets back to pre-crisis levels.

In the absence of more rapid policy intervention and behavioural changes, longer-term drivers of growth will continue to push up oil demand. As a result, by 2026, global oil consumption is projected to reach 104.1 mb/d. This would represent an increase of 4.4 mb/d from 2019 levels. Oil demand in 2025 is set to be 2.5 mb/d lower than was forecast a year ago in our Oil 2020 report.

Demand growth relative to 2019 is expected to come from emerging and developing economies, underpinned by rising populations and incomes.

Behavior changes

-

The new working-from-home models to cuts in business and leisure air travel.

-

More governments are focusing on the potential for a sustainable recovery as a way to accelerate momentum towards a low-carbon future.

-

A shift towards electric cars will accelerate.

-

Better efficiency in gas-powered cars.

Electric cars

The IEA expects global electric car sales to reach over 12 million in 2026, with a total fleet size close to 60 million. More than half of all electric cars will be situated in China, which took an early lead in their development, a quarter in Europe, the rest in Japan, the United States and other countries. By 2026, electric cars and buses will displace more than 1 mb/d of oil demand – 700 kb/d of gasoline demand and 300 kb/d of diesel – compared to 2020 levels.

Future Gas demand

The OECD’s 37 members are: Austria, Australia, Belgium, Canada, Chile, Colombia, Czech Republic, Denmark, Estonia, Finland, France, Germany, Greece, Hungary, Iceland, Ireland, Israel, Italy, Japan, Korea, Latvia, Lithuania, Luxembourg, Mexico, the Netherlands, New Zealand, Norway, Poland, Portugal, Slovak Republic, Slovenia, Spain, Sweden, Switzerland, Turkey, the United Kingdom and the United States.

Oil refinery demand

The combined demand for refinery-supplied gasoline, kerosene and diesel is forecast to decline by 170 Kb/d from 2019 to 2026, a sharp contrast to the previous seven years, when it increased by 6.2 mb/d. These products usually price at a premium to crude oil and are essentially the backbone of refinery economics.

The pandemic has effectively offered refiners a sneak peek into the future of sharply lower transport fuel demand. They should use this opportunity to adjust their strategies accordingly. This bears bad news for petrochemical producers, too. Barring higher than expected NGL output, they will have to share some of their margins with refiners to secure feedstock production in refineries.

Demographics and changing attitudes

The article did not mention changing demographics. The baby boomers had a love relationship with cars unlike any other generation.

Millennials and Gen Z are more content to use public transportation, work closer to home, text or play online games, etc. rather than take a casual spin in the car.

Author

Mike “Mish” Shedlock's

Sitka Pacific Capital Management,Llc