Sweden: Eventful week with Riksbank rate decision and April flash CPI

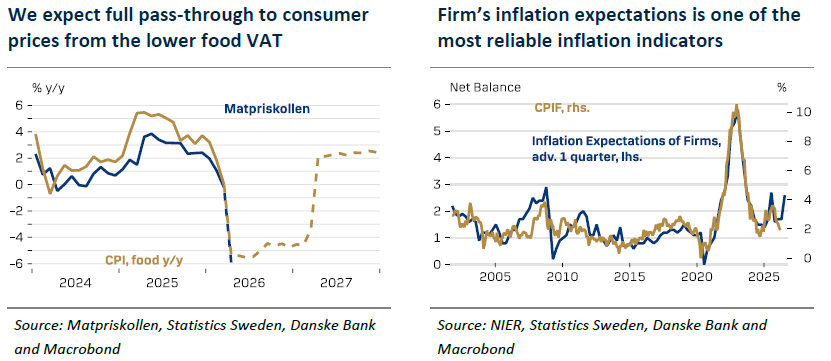

Preliminary inflation figures for April are expected to indicate a clear decline compared to March. Core inflation, measured as CPIF excluding energy, is anticipated to be 0.3% year-over-year, down from 1.1% in March. CPIF is projected at 1.2% year-over-year, while the CPI is expected to be 0.3% year-over-year. For more details, see the table to the right. The significant decline is due to changes in the VAT on food, which has been temporarily reduced from 12% to 6% and is expected to be restored in December 2027. We anticipate full impact on food prices and a partial effect on takeaway food prices from restaurants, which will lower year-over-year inflation by at least 0.8 percentage points in the coming months. These tax-related effects are added to other existing tax measures, which are already reducing headline inflation by 0.3 percentage points before the lower VAT. These adjustments are expected to provide temporary relief to consumers while moderating inflationary pressures in the short term.

Data from Matpriskollen confirm the expectation that the lower VAT on food will have its full effect (see chart below). It is important to note that Matpriskollen measures prices differently from Statistics Sweden, as it does not account for offers or sales campaigns, which Statistics Sweden includes. However, since the reduced VAT primarily affects regular prices, Matpriskollen’s predictions are likely to be more accurate than usual.

PMI, the NIER survey and the Riksbank

Input prices in Manufacturing PMI surged to 81.3, which is the highest level since 2022, and delivery times increased to 64.3 (see charts on next page). During normal circumstances, high delivery times indicate high demand, but it is reasonable to believe that the increase in delivery times now is rather a result of supply chain disturbances. The April NIER survey, released last week, is the first to capture the effects of the war in Iran. As expected, price expectations and inflation expectations rose. Firms’ inflation expectations surged from 1.7% to 2.6%. Although the level itself is not alarming, the substantial fluctuations highlight that inflation expectations remain less anchored than during the previous decade. Firms’ inflation expectations have proven to be one of the most reliable inflation indicators over time (see chart above). We expect the Riksbank to keep the policy rate unchanged at 1.75% in May and maintain our view that they will hike in June and August, aligning with our ECB call for two hikes in June and July.

Author

Danske Research Team

Danske Bank A/S

Research is part of Danske Bank Markets and operate as Danske Bank's research department. The department monitors financial markets and economic trends of relevance to Danske Bank Markets and its clients.