Student Housing Outlook: Steady as She Goes

Student Housing Developers Are on the Lookout for Overlooked Markets

Lower mortgage rates appear to finally be giving the housing market, and the overall economy, a much needed lift. Sales of both new and existing homes have perked up in recent weeks, though demand is still being held back by a lack of affordable homes for sale. Sales of homes priced at or below the median have remained strong throughout the cycle but the inventory of such homes remains exceptionally thin in nearly every market. Moreover, development of entry-level homes has been slower to get back on track in this cycle because of sharply higher land development costs and increased regulatory burdens. Shortages of workers and buildable lots have led many builders to focus on higher margin projects, many of which are in-fill projects or tear-down and rebuilds, where development costs tend to be less burdensome.

Continued affordability challenges in the single-family market have provided a tailwind for apartments. More people are choosing to rent and renters are remaining in apartments longer than they have in the past. Apartments account for a larger proportion of multifamily construction today, as condominium development has been hindered by regulatory issues, a drop-off in foreign buying and changes in the tax law, which have made home buying in many higher-priced markets, particularly those with high state & local taxes, less attractive. Much recent apartment development has focused on luxury/lifestyle units, typically in and around the largest employment centers of rapidly growing metro areas. While rental vacancy rates remain low nationwide, some of the nation's more active submarkets are currently absorbing massive amounts of new units.

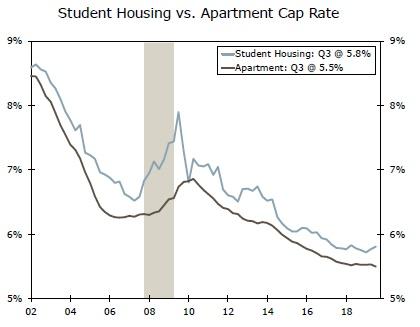

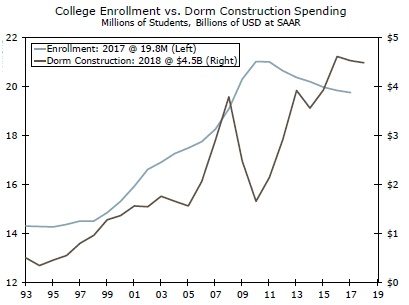

Student housing is another area of the housing market that has received increased attention. Over the past decade, cap rates for student housing have fallen steadily and the gap relative to apartments has narrowed (Figure 2). It is easy to see why investors have become enamored with student housing, particularly properties close to major universities. Enrollment rates remain elevated, which provides a steady stream of tenants (Figure 3). Tight university budgets have also meant there has been less traditional dorm construction, and much of the existing dormitory stock is old and outdated.

With limited budgets, many schools have turned to public-private partnerships to develop more upscale options. Universities have also become more aggressive at attracting international students and students from higher income and higher net worth families, who typically pay higher tuition and favor off-campus housing options or demand high quality on-campus housing. This reliance on international students has given some developers pause, as increasingly stringent visa requirements and the lingering trade dispute with China have slowed the inflow of international students. The competition for high-end students remains fierce, with many universities adding honors colleges and other amenities targeted toward high-performing students from private high schools.

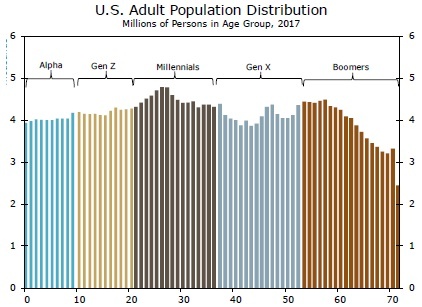

Without some easing of the hurdles foreign students are facing to secure visas to study in the United States, enrollments may have a tough time rising from their recent levels. While enrollment rates remain elevated, the huge wave of Millennials—the youngest of which are now 24—recently graduated, leaving schools with a smaller pool of potential candidates (Figure 4). An evertightening labor market may also dissuade potential students from pursuing higher education in lieu of high-paying jobs in skilled trades. Among students going to college, the current strong job market along with the increased awareness of the long-term burden of student loans are encouraging students to finish their education more quickly. Fewer students are lingering beyond the four years needed to secure a bachelor degree. The rising number of universities offering online programs is another potential headwind for student housing demand.

Development of student housing has tended to focus on the largest and fastest growing universities, particularly in the South and West. Texas and Florida are home to a number of the largest and fastest growing universities, reflecting their burgeoning economies and strong in-migration over the past few decades. Texas A&M and the University of Central Florida top the list of the largest oncampus enrollment in 2018. There are some inconsistencies in the data across colleges, with some schools including part-time students, online students and satellite campuses in their enrollment figures. The bulk of student housing is being developed close to campus, as recent studies have indicated that students that live on campus or within walking distance of campus tend to be more engaged in college activities and perform better academically than students that live further away from campus, particularly during their freshman and sophomore years.

Given the sustained rapid growth in the South and West, enrollements at many of the state's flagship universities have been essentially capped, which has led to rapid growth at other state schools and private universities within the region. Many of the communities that house these schools lacked the large stock of rental housing found in larger college towns and have seen extensive student housing construction in recent years. There has also been a surge in enrollment at engineering schools, reflecting the rapid growth in the tech sector, particularly in California, Texas, Florida and Georgia. On the flip side, growth in most universities in the Northeast and Midwest remains tepid at best.

Author

Wells Fargo Research Team

Wells Fargo