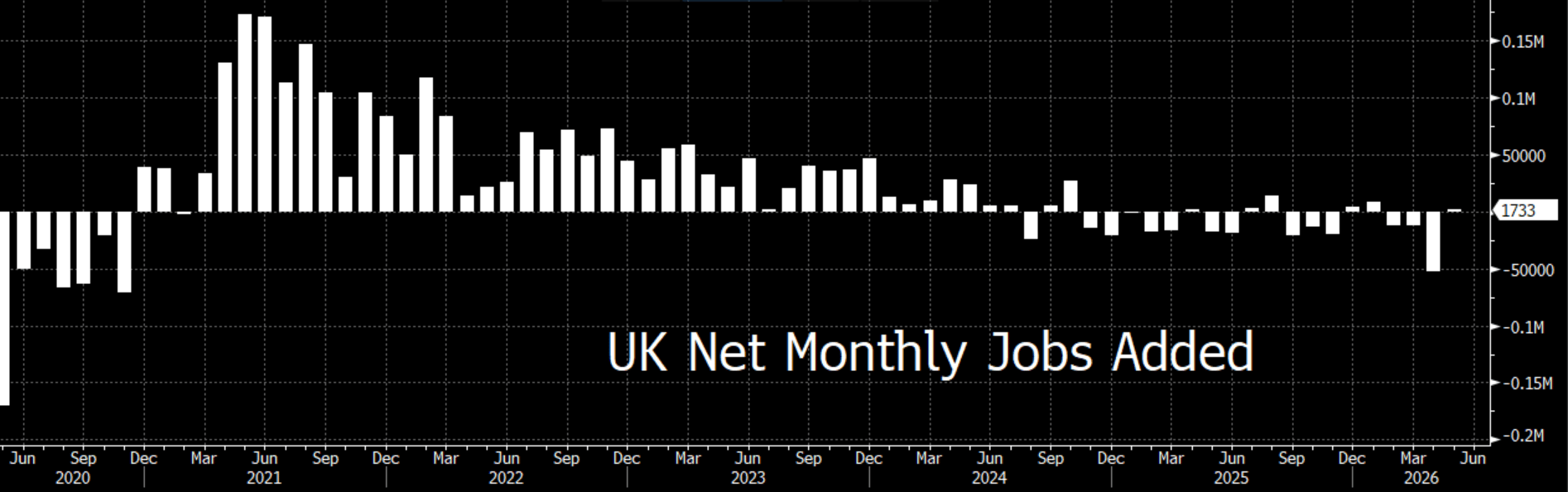

Since August of 2024 UK unemployment has only fallen twice

UK unemployment data has become an almost permanent bearish thorn in the Pound’s side; since August of 2024 UK unemployment has only fallen twice. The three months through to April happened to be one of these periods however. Today’s data shows that the three months to April saw the economy add jobs for the first time since January, even if it was only just shy of 2,000 jobs net.

AI, constraining government legislation and sluggish growth have all acted to pummel the UK employment market over the past 3 years and despite today’s improvement in numbers, this data is ultimately just “less bad” than previous figures.

It gives the Bank of England even less reason to hike rates, especially when the data is considered alongside the recent peace between the US and Iran and the failure of higher energy prices to materialise in UK CPI figures. Whilst the increase of the energy price cap in July and the scarcity of fertiliser for next year’s crop will eventually feed through into inflation, these concerns are likely both distant and sufficiently spread out to not move MPC members into action.

Instead, a prolonged pause seems likely before the cutting campaign can recommence in 2027. Today’s Makerfield byelection does present somewhat of a risk, if leadership hopeful Andy Burnham does clench the seat and then takes his expansionary fiscal ideas onto the national stage, it could lead to demand inflation.

Much more of concern however would be the likely significant softening in the Pound that would accompany such policy.

Today’s decision, a 7-2 vote to maintain the base rate at 3.75% is more than meets the eye, especially with regard to where the MPC sees inflation peaking, at just 3.25%. Given the likely transitory nature of this latest energy shock and the already elevated base rate, I suspect only a serious pickup in UK economic figures would change minds at the BoE.

Considering such a pickup has alluded the UK since the GFC, I maintain my Sterling bearish stance.

Author

David Stritch

Caxton

Working as an FX Analyst at London-based payments provider Caxton since 2022, David has deftly guided clients through the immediate post-Liz Truss volatility, the 2020 and 2024 US elections and innumerable other crises and events.