Silver enters industrial divergence phase as inflation and growth expectations collide

Key takeaways

Silver enters Thursday’s session at the intersection of two powerful macro forces: easing inflation pressure and uncertain industrial-growth expectations.

Yesterday’s softer US CPI report reduced pressure across real yields, while today’s ECB decision and US PPI release will help determine whether that shift extends across global markets.

Silver continues trading as both a monetary asset and an industrial metal, making it particularly sensitive to changes in growth expectations, manufacturing activity and rate pricing.

Recent price action suggests participation is beginning to recover after a prolonged period of weakness, although the broader structural trend remains under pressure.

Silver sits between two macro worlds

Silver enters today’s trading session in a uniquely complex position.

Few major commodities are simultaneously influenced by monetary conditions and industrial activity to the same extent.

That dual identity has become particularly important following yesterday’s US inflation report.

Core CPI slowed to 0.2% on a monthly basis, below expectations, helping ease pressure across Treasury yields and encouraging a modest reassessment of Federal Reserve expectations.

For gold, that development primarily affects real yields and reserve positioning.

For silver, the transmission mechanism is broader.

The metal must absorb changes in monetary expectations while also reflecting the outlook for industrial activity, manufacturing demand and investment across strategic sectors.

That combination explains why silver often behaves differently from gold during periods of macro transition.

Markets are not simply evaluating inflation.

They are evaluating the relationship between inflation, growth and industrial participation.

Industrial divergence remains the dominant theme

The most successful silver narratives of the past year have emerged when industrial considerations become more important than traditional precious-metals dynamics.

That framework remains highly relevant today.

Copper continues functioning as the primary industrial transmission asset across the metals complex.

Manufacturing expectations remain mixed across major economies.

European growth remains uneven.

Chinese industrial activity continues generating selective rather than broad-based support.

Against that backdrop, silver occupies a particularly interesting position.

The metal benefits from long-term structural demand linked to electrification, solar installations and industrial modernization.

At the same time, cyclical growth expectations remain less decisive than they were during previous expansion phases.

The result is an environment characterized by industrial divergence.

Participation remains visible across strategic industrial themes, while broader manufacturing confidence remains more selective.

Silver increasingly reflects that divergence.

Real yields continue shaping monetary participation

Monetary conditions remain an essential part of the silver story.

Yesterday’s CPI report reduced some of the upward pressure that had dominated real-yield pricing over recent weeks.

That shift matters because silver remains highly sensitive to the opportunity cost of holding precious metals.

The transmission channel remains clear.

Inflation influences Treasury yields.

Treasury yields influence real yields.

Real yields influence participation across precious metals.

Silver reacts to the same chain.

The difference is that industrial demand adds an additional layer of complexity.

Investors must therefore evaluate both monetary conditions and industrial expectations simultaneously.

That makes silver one of the most information-sensitive commodities during periods of macro transition.

Today's ECB decision and US PPI release will provide additional evidence regarding the broader inflation and growth landscape.

Both events have the potential to influence how investors assess future participation across industrial metals.

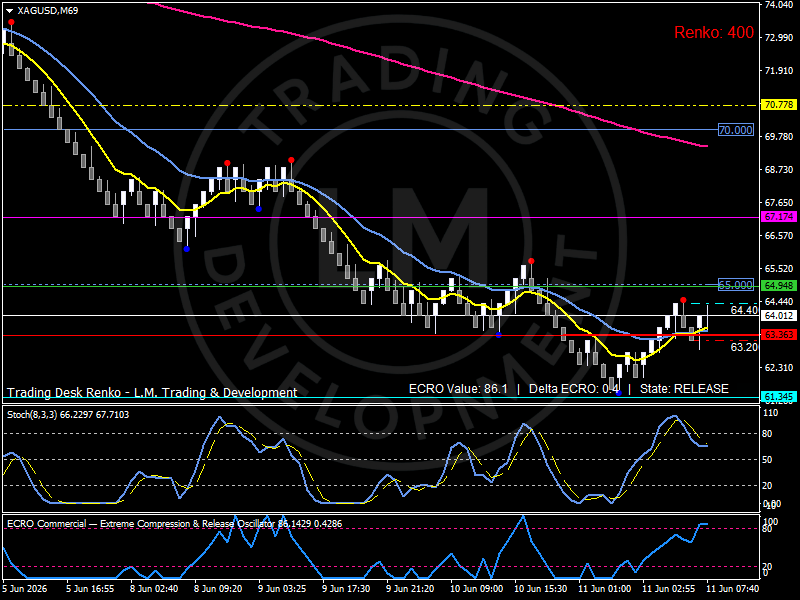

Technical structure: Silver participation begins to recover

The technical structure reflects a market attempting to rebuild participation after an extended repricing phase.

The broader H4 trend remains negative.

The decline from the 78 region toward recent lows near 63 generated one of the most significant corrections seen across the metals complex over recent weeks.

That broader structure remains visible.

The pace of decline, however, has moderated.

Recent sessions have produced a stabilization process rather than continued acceleration lower.

The Renko framework provides additional evidence of improving participation.

Following the recent low near 61.3, silver has gradually rotated higher and reclaimed the 63.2 participation area.

The current structure is approaching the 64.4–65.0 corridor, which now represents the first important recovery zone.

The ECRO indicator has advanced toward the mid-80s and remains in a release state, suggesting participation has improved significantly relative to the conditions that dominated the previous decline.

Momentum has strengthened.

Confirmation remains incomplete.

Resistance begins near 64.4 and extends toward 65.0, followed by the broader recovery corridor around 67.2.

Support remains concentrated near 63.2, with deeper stabilization developing around 61.3.

The overall structure remains consistent with a market transitioning from exhaustion toward re-engagement.

Bird’s eye view

Silver currently operates at the intersection of monetary repricing and industrial participation.

Yesterday’s softer CPI reading reduced pressure across real yields, while today’s ECB decision and US PPI release will determine whether that adjustment broadens across global markets.

Structurally, the market has stabilized above the 63.2 participation zone and is now challenging the 64.4–65.0 recovery corridor, while 67.2 remains the next major upside reference point.

The dominant variables remain real yields, copper leadership, manufacturing expectations and industrial participation.

Outlook

Silver enters the second half of the week inside a market where inflation expectations and industrial demand are sending different signals.

The metal continues benefiting from its role as a strategic industrial asset while remaining sensitive to changes in monetary conditions.

That combination explains why silver often becomes one of the most dynamic commodities during periods of macro transition.

The next phase will depend on whether improving participation can attract broader industrial engagement and whether easing inflation pressure continues supporting the precious-metals complex.

For now, silver remains one of the clearest expressions of industrial divergence across global commodity markets.

Author

Luca Mattei

LM Trading & Development

Luca Mattei is a market analyst focusing on FX, metals, and macroeconomic trends. He develops trading tools for retail and professional traders, coding indicators and EAs for MT4/MT5 and strategies in Pine Script for TradingView.