Rates Spark: The worry about curve inversion

Hawkish central banks and low market growth expectations have kept rates in a range. This has largely benefitted risk appetite but is also resulting in a more inverted curve, hardly an encouraging macro signal.

Powell and Schnabel might accelerate the curve inversion trend today

We tend to be sceptical of the overall impact central bank comments can have on day-to-day market rate movements. One reason is the abundance of central bank communication. The other is their data-dependent setting (see yesterday’s note) which put economic releases firmly in the driving seat of market moves. Unfortunately, today is, like yesterday, much heavier on central bank communication than on economic data. This means the signal to noise ratio is likely to remain low. Still, today’s headliner, Fed chair Jerome Powell, is probably the world’s most watched central banker, so his testimony will carry weight with investors. Similarly, we think Isabel Schnabel’s interventions are amongst the most listened to out of the European Central Bank (ECB).

This year in rates has been characterised by a tug-of-war between hawkish central banks and pessimistic markets, at least when it comes to growth. A hawkish tone in the face of sticky core inflation makes sense but central banks have hurt their credibility by reinforcing their message with overly upbeat growth forecasts. This makes sense up to a point, as markets are much more likely to believe a hawkish central bank if economic growth allows it to tighten policy further. However it seems markets collectively disagree with central banks’ forecasts, by pricing subsequent rate cuts. In short, central banks’ sphere of influence doesn’t extend much beyond the front-end of the curve.

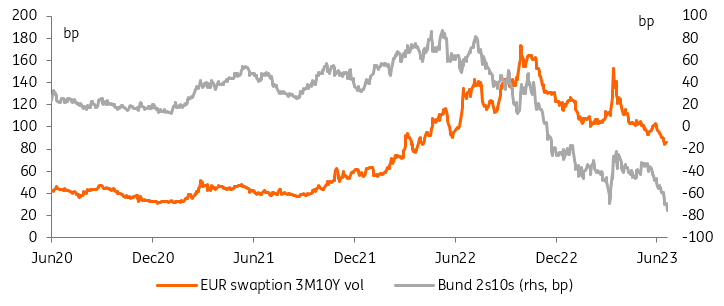

The resulting curve inversion has accelerated in countries where economic sentiment is weakest. For instance, in the Eurozone the 2s10s swap curve flattened to its most inverted level on record: -78bp. Looking at the same segment of the German sovereign curve for longer history, this seems to be at its most inverted since the early 1990s. So far this year, the lack of interest rate direction, despite elevated day-to-day volatility, has been a supportive factor for risk appetite. The tug-of-war between hawkish central banks and pessimistic market growth expectations has kept rates in a range but it is also bringing about a more inverted curve, a sure sign of worsening economic expectations. This fragile equilibrium continues, for now.

Falling rates volatility and inverted yield curves send contradictory signals about the health of the economy

Source: Refinitiv, ING

Read the original analysis: Rates Spark: The worry about curve inversion

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.