Pound Plummets on U.K Political Woes

After a quiet week on the economic front, the pace of fundamental releases picks up this week.

Japan, the Eurozone and Germany will release preliminary Q3 GDP.

In the U.K, British assets are expected to be in for a choppy ride as key consumer and producer price data along with the latest data on the labor market and retail sales tops the agenda, as too does a threat to PM May’s leadership.

Stateside, U.S inflation and growth numbers will take priority, as they could be key to the Fed’s determination to hike rates in December. Talks on tax legislation will also be playing into market thinking.

From China, a raft of closely watched economic releases is due this evening, including industrial production, fixed-asset investment and retail sales.

1. Stocks mixed results

In Japan, the Nikkei dropped to a two-week low overnight as many sectors weakened after recent rallies, offsetting gains in companies with strong results. The Nikkei ended -1.3% lower, the lowest closing level since Oct. 31 and its fourth straight daily decline. The broader Topix dropped -0.9%.

Down-under, gains by mining stocks weren’t enough to offset two of Australia’s big banks trading ex-dividend as the S&P/ASX 200 fell -0.1% following a choppy overnight session. In South Korea, the Kospi index was down -0.5%.

In Hong Kong, stocks rose slightly overnight, reflecting general market caution as investors wait for details on whether U.S Republicans could pass a tax reform deal quickly. The Hang Seng index added +0.2%, while the Hong Kong China Enterprises Index lost -0.5%.

In China, stocks extended their climb, powered by banks on financial deregulation. The blue-chip CSI300 index rose +0.4%, while the Shanghai Composite Index also gained +0.4%.

In Europe, regional indices are giving up most of their early with U.S tax reform uncertainty as well a question over the U.K PM May’s leadership weighing on stocks.

U.S stocks are set to open unchanged.

Indices: Stoxx600 -0.4% at 387.3, FTSE +0.2% at 7449, DAX -0.1% at 13111, CAC-40 +0.3% at 5368, IBEX-35 -0.2% at 10075, FTSE MIB -0.5% at 22436, SMI +0.3% at 9165, S&P 500 Futures flat.

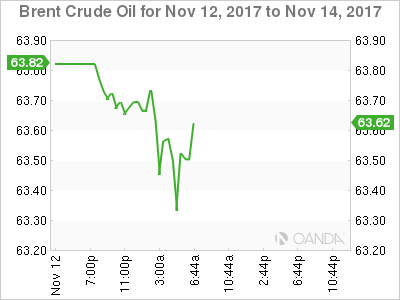

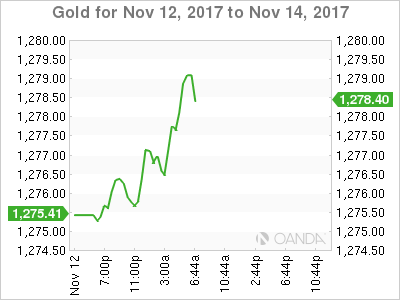

2. Oil markets cautious on Middle East tensions, gold lower

Oil trading remains cautious amid ongoing tensions in the Middle East and after a rising rig count in the U.S suggested producers there are preparing to increase output.

Brent crude futures are at +$63.57 per barrel, up +5c from Friday’s close. U.S West Texas Intermediate (WTI) crude is at +$56.78 per barrel, up +4c.

Crude prices have generally being well supported as ongoing output cuts led by the OPEC and Russia have contributed to a significant reduction in excess supplies that have been pressuring markets over the past three-years.

On the supply side, tensions in the Middle East is raising the prospects of disruptions, along with yesterday’s strong earthquake that hit Iran and Iraq – the market is still accessing the impact on the region’s oil production.

Last week, U.S drillers added nine oilrigs in the week to Nov. 10, the biggest jump since June, bringing the total count up to 738 according to Baker Hughes.

Gold prices continue to drift in a narrow range overnight, but held near the previous session’s low, pressured by a firmer dollar and expectations of a series of interest rate hikes by the Fed. Spot gold is nearly unchanged at +$1,276.61 per ounce.

Note: On Friday, gold dropped -0.7% for its biggest intraday percentage fall since Oct. 26, weighed down by a rise in U.S. Treasury bond yields.

3. Sovereign yield curves flatten

Eurozone bond yields have slipped from recent highs this morning, but are to be tested this week by a series of government bond sales, starting with today’s Italian auction.

Yields across the region rallied towards the end of last week, triggered by a large seller of Bund futures on Thursday. This curbed a rally that began after the ECB’s October policy meeting, when it extended its bond-buying scheme until at least September 2018.

Note: More than €30B EUR’s of new bonds are set to enter the market this week.

Stateside, uncertainty around tax reforms in the U.S pushed Treasury yields higher on Friday. This week’s U.S inflation numbers are expected to move markets again, as investors look for clues on future Fed rate increases.

The yield on U.S 10-years has declined -3 bps to +2.37%, the largest drop in more than a week. In Germany, the 10-year Bund yield fell -2 bps to +0.39%, the biggest fall in a week, while in the U.K, the 10-year Gilt yield fell -4 bps to +1.305%, the largest drop in more than a week.

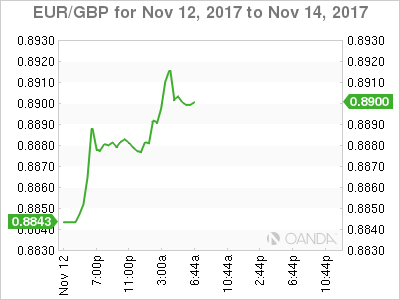

4. Sterling folds under political pressure

The pound (£1.3083) starts the week under pressure as 40 MP’s supposedly have agreed to sign a letter of ‘no confidence’ in PM May’s leadership.

Note: Only eight more MP’s are required to start a formal leadership challenge.

Any U.K political turmoil is likely to dent any clarity on Brexit negotiations. Tech analysts note that a break below £1.30 would suggest more downside momentum. EUR/GBP cross testing above the €0.89 level as a result.

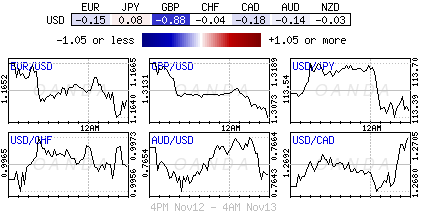

Elsewhere, the USD is trading somewhat mixed against G10 currency pairs. The EUR/USD is lower by -0.2% at €1.1640, USD/JPY remains little changed at ¥113.35.

5. Fed’s Harker leaning toward an interest rate hike

Federal Reserve Bank of Philadelphia President Patrick Harker said overnight that he is still leaning toward supporting an interest-rate increase at next month’s Fed meeting.

Fed Harker stated “pressing forward with rate rises and reducing the balance sheet is the right path for the Fed” and that he still “has another +25 bps rate increase penciled in for this year, although perhaps I should say, lightly penciled in.”

Note: Strong job growth and solid activity gains support the case for a rate increase, but weak price pressures complicate the outlook, and some believe boosting the cost of short-term borrowing is a mistake in the current environment.

Author

Dean Popplewell

MarketPulse