Pivotal moment for USD/JPY

USD/JPY

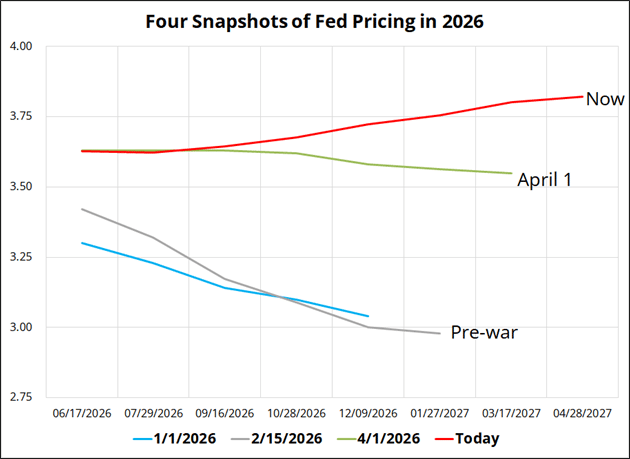

The MOF is in an interesting spot here after a decent nonfarm payrolls, hot CPI, flaming PPI, and a flip to pricing FOMC hikes. Here is 2026 evolution of Fed pricing:

The market is not pricing a lot of hikes, but it’s a regime change from what we had before the war. This is not helpful for the MOF as the G7 mantra is that intervention is meant to push back only when FX does not reflect fundamentals. If the BOJ is on hold and the Fed are priced to hike, intervention becomes less palatable. Bessent has come and gone from Japan with no news, and USDJPY is creeping back towards the key 158.00 level.

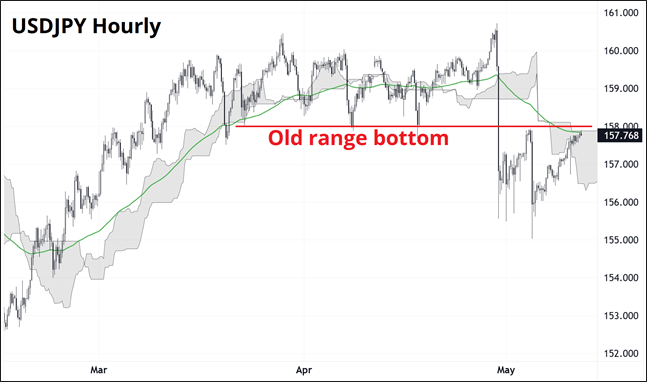

You can see in that chart that the bottom of the old range (red line), the 100-hour (green line), and the top of the hourly ichimoku cloud all come in at 158.00. Above there, JPY bears will be emboldened, and the MOF will be in an extremely unpleasant spot. And! We get a BOJ speech tonight at 10 p.m. NY time from board member Masu Kazuyuki. I will turn the mic over to Simon Flint, our Asia FX specialist.

Simon flint: BoJ thoughts after a few days in Tokyo

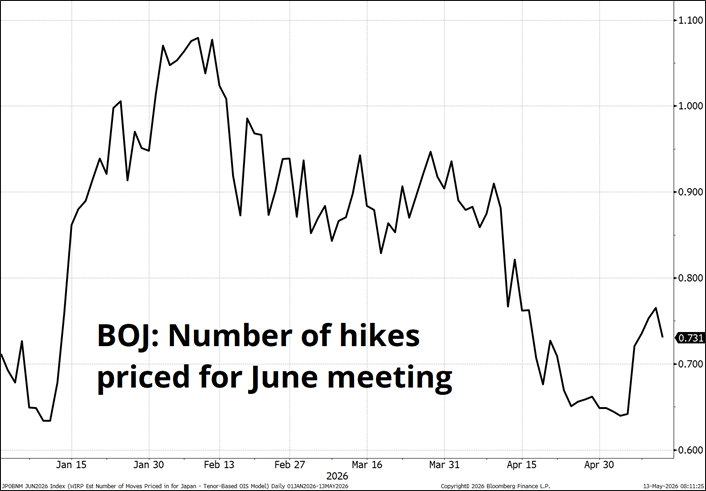

My conclusion after day one of my meetings was that there was only a 40% chance of a BoJ hike in June (versus 75% priced). This is purely on the basis that Takaichi prefers that the BoJ don’t hike. Were it purely a BOJ decision, 75% (& rising as time passes; ceteris paribus) would be reasonable odds.

However, I thought it worth reporting that one BoJ expert with vastly better qualifications than me disagreed & put the odds at 80%; given that the first test of his thesis comes tomorrow with Masu’s speech.

One thread of his reasoning went as follows:

- With three dissents, we are close to a critical mass for a further hike.

- There’s a decent chance that Masu & Koeda join the dissenters & create a 5/4 split.

- Masu & Koeda were already more hawkish than Nakagawa - the third (surprise) dissenter at the April meeting.

So, an imminent test of this thesis is Masu’s speech in Kagoshima. (NB/ Dept Govr Himino speaks on May 16, Koeda is on May 21, and Ueda on June 3, BoJ next decides on June 16.)

You’re not in England anymore

Ueda-san would then switch to endorsing a hike in the face of a potentially embarrassing defeat for the core of the board. The BoJ Governor has never lost a vote in the modern public-vote era; this is NOT the BoE.

Ueda, staring down the tunnel at a train wreck (of a 5/4 defeat or a clash with the Govt), would present these facts to the Govt, which would be forced to give its assent (as the market consequences of a “train wreck” would be far greater than any economic distress from the rate hike).

Indeed, my meetings in Tokyo confirmed that the Government’s anti-hike conviction is only (say) 60/40 IMO.

This is, in part, because a new political consensus has evolved that a weak JPY is politically poisonous, as it is associated in the minds of the public with a cost-of-living squeeze. Furthermore, Bessent has been clear in his belief that the BoJ is behind the curve, and he resents the spillovers into FX and JGBs (& hence USTs). As a side note — & idle speculation on my part — it was surely no coincidence that Ueda chose to fly to neutral Switzerland for a routine BIS meeting (it’s the bimonthly outing), rather than be subjected to a meeting with Bessent.

Either 1) the train-wreck thesis, or: 2) further upside in USD/JPY that the MoF is unable to contain, or 3) a significant rise in inflation expectations, or 4) evidence that a BoJ hike would calm the JGB market***, would convince the Govt to give its consent to a hike.

So, this makes Masu’s speech tomorrow of considerable importance. Masu has described himself as “right in the middle” of the pack, is considered fairly pragmatic, & (as I said) was previously believed to be more hawkish than Nakagawa.

***The evidence that a BoJ hike would help calm JGBs is NOT strong, and (for good reason) the Govt’s default belief is that a BoJ hike will raise JGB yields. Indeed, if one looks at the rapid pricing-in of a Dec. hike (which rose from 16% priced on Nov. 21), it was associated with a clear rise in JGB yields (out to 30Ys). Similarly, the pricing-out of the April hike (from 55% on April 10) was associated with a drop in JGB yields. So, good luck convincing the govt that a rate hike will lower longer rates!

Masu’s last speech

In fact, Masu’s last speech, delivered on Feb. 6, already reads fairly hawkish. Hence, one would need to see an upgrade of this language for confirmation of the BoJ hike thesis.

Perhaps his speech will suggest that the BoJ cannot look through the supply shock presented by the war in Iran.

Perhaps stating clearly that “the war will bring forward the timing for underlying CPI inflation to reach 2 percent,” or “prices and inflation expectations will likely rise significantly” (expectations being key here), or “the Bank needs to address the risk of prices deviating upward.”

Key excerpts from his Feb. 6 speech:-

“The real interest rate… is at a significantly negative level.”

“I am convinced that continuing with further policy interest rate hikes will be needed to complete the normalization of monetary policy in Japan.”

“Attention should be paid to whether inflation triggered by the yen's depreciation may raise people's inflation expectations and, in turn, affect underlying inflation.”

“Highly likely that firms would continue to raise wages steadily this year.”

“Financial conditions in Japan remain assuredly accommodative. Given this, if the outlook for economic activity and prices presented in the January 2026 Outlook Report is realized, the Bank, in accordance with improvement in economic activity and prices, will continue to raise the policy interest rate and adjust its degree of monetary accommodation in the process of completing the normalization of monetary policy.”

“Although the underlying inflation rate remains below 2 percent, it is drawing very close to the 2 percent target.”

“As the behavior that took root during the period of deflation is now being unentrenched, Japan has clearly entered an inflationary phase. Given this situation, what is vital from now on is to ensure that, through timely and appropriate policy interest rate hikes, the underlying inflation rate remains below 2 percent. At the same time, it is critical to make sure that excessive rate hikes do not disrupt the virtuous cycle of a moderate rise in prices and wages that has finally begun to gain momentum in Japan. The Bank will therefore proceed cautiously with rate hikes.”

Given that February speech was fairly hawkish, anything dovish tonight would be a disaster for the JPY with market pricing high odds of a hike in June. If our man on the right is hawkish, that keeps the rate hike in play, and he would need to go uber-hawkish to increase hike odds. Without the BOJ supporting the MOF’s efforts, the JPY will likely fall victim to the trilemma and USDJPY will be above 162 in July. For now, it makes sense to assume that the BOJ and MOF are working in concert, but if they are not, as Simon’s 40/60 odds gently imply, that’s big.

Simon is also reducing his bearish USDCNH view for the short run as he believes it’s a bit short-term macro crowded into the Trump/Xi meeting. He has nailed the move from 6.90 to here and is less bullish CNH for the short run. If you are a Spectra FX trading client, you can receive Simon’s thoughts regularly. If you work at a hedge fund and don’t trade with Spectra: Ping me on Bloomberg and let’s get coverage going.

Final thoughts

G10 FX is calm even as equities collapsed and decollapsed, and we got the somewhat amusing overnight headline that NVDA insta-added 125 billion in market cap last night because the news dropped that Jensen Huang was joining Trump in China. Meanwhile, everyone wonders if forecasts of a supply shock from the closing of Hormuz were wrong or just a bit off on the timing.

When will the Fed see red?

Author

Brent Donnelly

Spectra Markets

Brent Donnelly is the President of Spectra Markets. He has been trading currencies since 1995 and writing about macro since 2004. Brent is the author of “Alpha Trader” (2021) and “The Art of Currency Trading” (Wiley, 2019).