Peace off, Petrodollar on

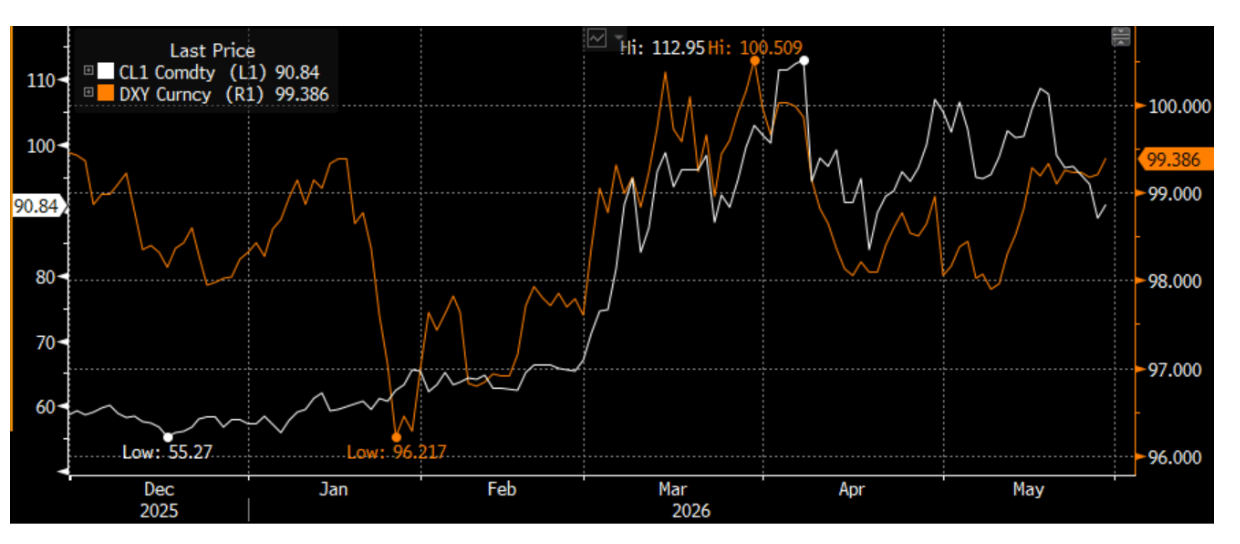

The whiplash of expectations from genuine expectations of a permanent peace in the Gulf yesterday to the harsh reality of today following the latest US strikes on Iran have laid bare just how strongly correlated the two have become over the past few months. One Bloomberg indicator suggests that the two are more closely related now than ever before, although as I have pointed out, the Dollar rally has widened from an almost pure Petrodollar move to one that also incorporates higher base rate expectations for the Fed as Warsh sounds more hawkish than anyone expected.

Swaps data indicates that the expected future base rate of the Fed has now risen both faster and higher than the BoE and ECB, which explains why the DXY was able to grind out gains on Tuesday and Wednesday even as Oil plummeted on peace talks. Stronger Dollar seems the default position of markets, if tensions spike, higher Oil prices and that left cheek of the Dollar smile curve (USD strengthens in times of geopolitical crisis as a safe haven) see USD higher.

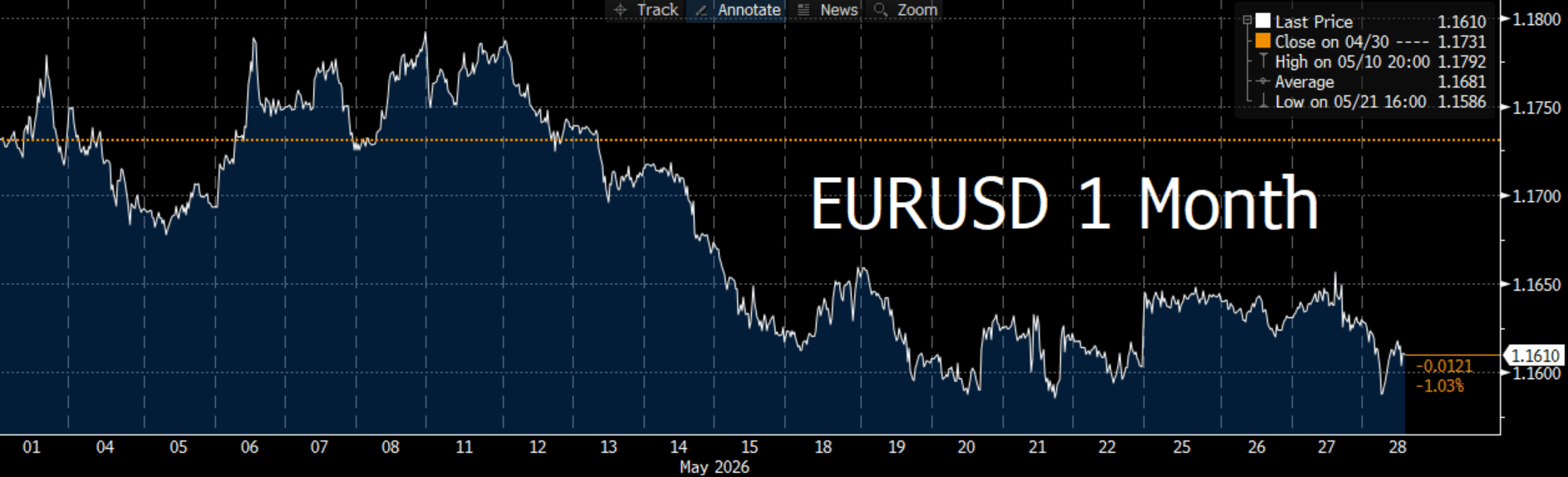

If tensions cool, USD still grind higher as traders keep revising higher their stock in Warsh as a hawk. The Pound is consumed with political risk and a likely hesitant Bank of England whilst the Euro seems to have already peaked in the near term and endures more tests of the $1.16.

The Yen is somewhat more supported due to the most recent actions of the Bank of Japan, although the long-term effectiveness of such interventions has a rather lacking history.

Every G-10 currency looks to finish this month weaker against the Dollar, despite many expecting that such strong expectations of peace would mark the end of the Dollar rally. Indeed, it’s becoming more and more difficult to see what will actually dull this charge, although a softer than expected statement at the June 17th Fed meeting could prove the silver bullet.

Still, given Warsh’s apparent distain for forward guidance, see his remarks at his senate hearing, we may still be operating in a “Dollar stronger regardless” market.

Author

David Stritch

Caxton

Working as an FX Analyst at London-based payments provider Caxton since 2022, David has deftly guided clients through the immediate post-Liz Truss volatility, the 2020 and 2024 US elections and innumerable other crises and events.