Oil cracks, the Dollar slips, and Wall Street starts pricing the peace dividend

- Markets are rapidly transitioning from pricing geopolitical fear toward pricing a potential peace dividend as Hormuz reopening expectations pressure oil and the dollar lower.

- Positioning dynamics now matter more than macro narratives in the short term as elevated index shorts, aggressive call buying, and underexposed managers create real squeeze risk higher in equities.

- Even if oil-driven inflation fades, structurally elevated bond yields may persist because governments and the AI investment boom continue competing aggressively for global capital.

Oil cracks

Markets opened the holiday shortened week with traders watching war clouds finally begin to part over the Strait of Hormuz, as the first hints of blue sky emerged after weeks of navigating a geopolitical hurricane. Oil collapsed more than 4.5% toward the $98 handle, the dollar softened across most of the G10 complex, Treasury futures rallied, gold climbed, and equity futures pushed higher as investors started pricing the possibility that the world’s most dangerous energy choke point may soon reopen to something resembling normal flow. The market response made perfect sense given how much inflation fear and hawkish rate pricing had been embedded into the curve during the recent energy shock. If oil and yields continue moving lower together as Hormuz traffic normalizes, equities could continue to extend higher simply because a significant portion of the inflation scare that helped push bond yields to multi-year highs would begin to reverse at the same time earnings season closes on a remarkably resilient note for corporate America.

That shift in psychology matters because the market spent most of the past month trading like a ship navigating through a minefield where every tanker headline threatened to detonate another inflation shock across global assets. Now, traders suddenly find themselves staring at the possibility that the same geopolitical risk premium which drove oil, yields, and the dollar higher could begin unwinding simultaneously. Treasury futures markets have already started leaning into that possibility, while equity futures continue to climb on the idea that softer energy prices could ease pressure on central banks, just as earnings season winds down with results still broadly supportive of risk appetite.

Under the surface, alongside the potentially improving macro backdrop tied to lower oil, lower rates, and easing inflation pressure, the squeeze dynamic itself is becoming increasingly real, with underweight and short positioning potentially becoming the market’s biggest fuel source. Hedge funds ramped up gross exposure last week at the fastest pace seen in years, with aggressive long buying flowing back into technology, semiconductors, software, communications equipment, and consumer discretionary names. Prime books are now carrying information technology exposure at five year highs just as bearish ETF positioning begins unwinding after weeks of defensive hedging. The tape increasingly resembles a market where too many managers remain underexposed to momentum while benchmarks continue grinding relentlessly higher, forcing reluctant buyers back into risk simply to avoid falling further behind performance targets.

Under this scenario, the market no longer needs spectacular economic data to rally. It simply needs enough stabilization in the macro backdrop to force underpositioned investors back into risk assets.

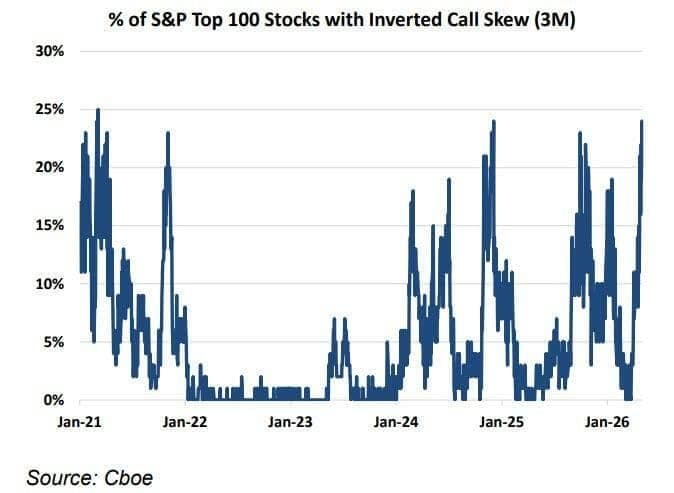

The options market is reinforcing that same dynamic. Upside optionality continues to dominate flows, the inverted call skew* is spreading across major S&P names, and speculative bullish positioning increasingly resembles the kind of momentum-chasing structure seen during previous melt-up phases. The market is effectively functioning like a casino where volatility sellers, passive inflows, dealer gamma, and AI momentum traders all keep reinforcing the same directional move. Every pullback gets absorbed because too many investors remain defensively positioned relative to benchmark performance risk.

What makes the resilience even more remarkable is that the macro backdrop underneath the surface still looks fragile in several places. Consumer sentiment readings remain weak, Chinese economic data continues to disappoint, and bond strategists still warn that yields may remain structurally elevated even if tensions in the Middle East cool. Massive government borrowing needs are not disappearing, while the AI capital expenditure supercycle continues absorbing extraordinary amounts of global capital. Governments, hyperscalers, and corporations are now simultaneously competing for funding across infrastructure, chips, power grids, cooling systems, and digital buildouts. The modern market increasingly resembles a global capital auction in which sovereign debt and AI infrastructure projects bid aggressively for the same pool of money.

That is why yields may not collapse even if crude continues retreating. The oil-driven inflation premium may ease, but structural funding pressures tied to deficits, reshoring, defence spending, and AI expansion still remain firmly in place. Investors are beginning to understand that this is not a traditional late-cycle slowdown environment. It is a world attempting to finance an industrial-scale transformation while carrying historically large debt burdens.

Still, for now, liquidity and positioning continue to overpower macro caution. The S&P 500 has now climbed for eight consecutive weeks despite volatile Iran-related headlines, weakening consumer confidence surveys, and higher bond yields, as the market increasingly behaves like a momentum machine powered by AI scarcity psychology and systematic inflows. Semiconductors continue to function as the central nervous system of the rally, while every major NVDA earnings release reinforces the belief that the AI buildout remains in its early innings despite increasingly crowded positioning.

The more fascinating contradiction within the rally is that markets continue to price in endless demand for chips, memory, and AI infrastructure while simultaneously ignoring the growing physical constraints on electricity generation and grid capacity. The tape increasingly resembles a boomtown pricing skyscrapers before checking whether enough power lines exist to keep the lights on. For now, scarcity continues to drive the narrative, and momentum remains self-reinforcing, but the structural contradictions beneath the surface are slowly becoming harder to ignore.

Meanwhile, the reopening of Hormuz itself is becoming increasingly tangible. Tankers are already moving back through the waterway after approvals were granted, commercial traffic is gradually resuming, and markets are starting to normalize the idea that one of the world’s most critical energy arteries may avoid prolonged disruption after all. Yet negotiations still remain fluid enough that volatility could easily re-emerge. Tehran continues to press for asset-unfreezing provisions, while Washington remains reluctant on several key clauses, leaving markets vulnerable to sudden reversals if diplomacy begins to fracture again. Oil volatility may ease from panic levels, but the geopolitical premium is unlikely to disappear entirely anytime soon.

Ultimately, this still feels like a market caught between two competing forces. On one side sits the peace dividend narrative, consisting of lower oil prices, softer inflation expectations, easing yields, resilient earnings, and systematic short covering, capable of driving equities materially higher into the summer. On the other side sits the structural reality that deficits, AI funding pressures, fragile consumers, and elevated bond yields never truly disappeared. For now, liquidity, momentum, and positioning continue winning that battle. But the higher this rally climbs, the more it resembles a suspension bridge stretched tighter above an increasingly volatile macro canyon. Stable while flows remain supportive. Potentially violent if positioning ever loses balance.

*Inverted (or reverse) call skew occurs when out-of-the-money (OTM) call options trade at a higher implied volatility (IV) than at-the-money (ATM), or OTM put options. It is a rare market anomaly indicating a "chase" for upside market exposure.

Author

Stephen Innes

SPI Asset Management

With more than 25 years of experience, Stephen has a deep-seated knowledge of G10 and Asian currency markets as well as precious metal and oil markets.