Natural Gas enters timing-sensitive phase as LNG risks persist

Key takeaways

- Natural gas continues trading inside a timing-sensitive framework shaped by LNG flows and shipping risk.

- European LNG concentration and Hormuz uncertainty continue tightening flexibility across the system.

- Price remains supported above the 2.80 participation zone as refill sensitivity drives positioning.

Natural Gas pricing increasingly reflects timing and access conditions

Natural gas continues operating inside a market shaped by LNG routing, shipping continuity and refill sensitivity rather than by immediate supply shortages alone. The broader energy system remains functional, though flexibility across the network continues tightening as geopolitical and logistical risks interact with storage dynamics.

This environment has become increasingly visible across European LNG infrastructure. Concentration inside the terminal system remains elevated, with the top three LNG nodes accounting for 33% of total European flows while the top five control nearly 47.5% of regional intake capacity. The Herfindahl–Hirschman concentration index currently stands at 647.5, confirming that LNG access continues depending on a relatively narrow group of strategic entry points.

The market therefore continues pricing timing efficiency and operational continuity alongside outright supply availability.

This distinction matters because LNG systems function through synchronization. Cargoes, terminal slots, storage injections, bunker conditions and shipping routes all operate inside narrow temporal windows. Delays or disruptions across one layer progressively influence the broader transmission chain.

Hormuz risk continues shaping LNG flexibility

Shipping intelligence remains dominated by Hormuz related developments.

Multiple LNG carriers continue attempting transit adjustments while security conditions across the corridor remain unstable. Recent reports confirming that additional LNG vessels are attempting passage through Hormuz reinforce the idea that the market remains focused on route continuity rather than on outright flow collapse.

This creates an important pricing dynamic.

The LNG market is increasingly reacting to:

- Access conditions.

- Routing security.

- Insurance costs.

- Scheduling reliability.

- Flexibility loss.

rather than to immediate production outages.

Shipping Radar data continues signaling an EXTREME STRESS regime, with risk signals remaining the dominant component across the transportation system.

At the same time, reports linked to possible Hormuz transit toll mechanisms and renewed naval positioning continue reinforcing uncertainty across regional energy routing.

The broader market therefore remains highly sensitive to timing disruptions even while physical LNG continues moving through the system.

Fleet expansion confirms expectations of structural LNG demand

The shipping layer also reveals another important signal: the industry continues expanding LNG transportation capacity despite elevated geopolitical stress.

Petronas recently chartered five newbuild LNG carriers from MISC, while BW LNG remains connected to additional vessel expansion projects in South Korea.

These developments matter because fleet expansion reflects long duration expectations around LNG demand and transportation requirements.

The market continues investing in future LNG mobility because global gas systems increasingly depend on flexible seaborne energy access. Asia, Europe and emerging industrial economies all continue competing for cargo reliability, storage stability and transport availability.

This creates a framework where LNG pricing responds simultaneously to:

- Weather expectations.

- Storage injections.

- Fleet capacity.

- Shipping security.

- Regional competition.

- Cargo timing.

The system therefore behaves increasingly like a timing market rather than a conventional commodity market.

European refill sensitivity remains active

European storage and refill dynamics continue reinforcing the broader LNG framework.

Although current flows remain operationally stable, the concentration profile of the European LNG system increases sensitivity to disruptions affecting key terminals or shipping corridors.

Gate Terminal, Dunkerque LNG and TVB continue representing the primary operational nodes across the European intake structure.

This concentration matters because refill systems depend on continuity across a relatively limited infrastructure network.

The latest LNG intelligence snapshot also showed no Italian LNG entries during the selected observation window.

This does not imply immediate supply stress. It does, however, highlight how regional balancing conditions can shift rapidly depending on timing, scheduling and cargo distribution.

European gas pricing therefore continues reacting to refill sensitivity rather than to outright scarcity conditions.

This framework becomes particularly important during periods of geopolitical uncertainty because storage systems lose flexibility when routing conditions tighten simultaneously.

Macro conditions continue supporting gas positioning

Natural gas also continues benefiting from a broader macro environment shaped by resilient energy demand expectations and stable industrial participation.

US inflation data earlier this week reinforced the idea that energy consumption conditions remain relatively stable across the broader economy. At the same time, industrial continuity across Asia and Europe continues supporting LNG utilization despite uneven manufacturing conditions.

The Dollar remains relatively firm while broader risk appetite across shipping linked assets stays mixed. Even so, natural gas futures continue outperforming several transportation categories during the latest session.

NG futures gained +0.77%, becoming one of the strongest components across the broader shipping and energy matrix.

This relative resilience reflects the market’s continued focus on LNG flexibility, storage timing and routing continuity.

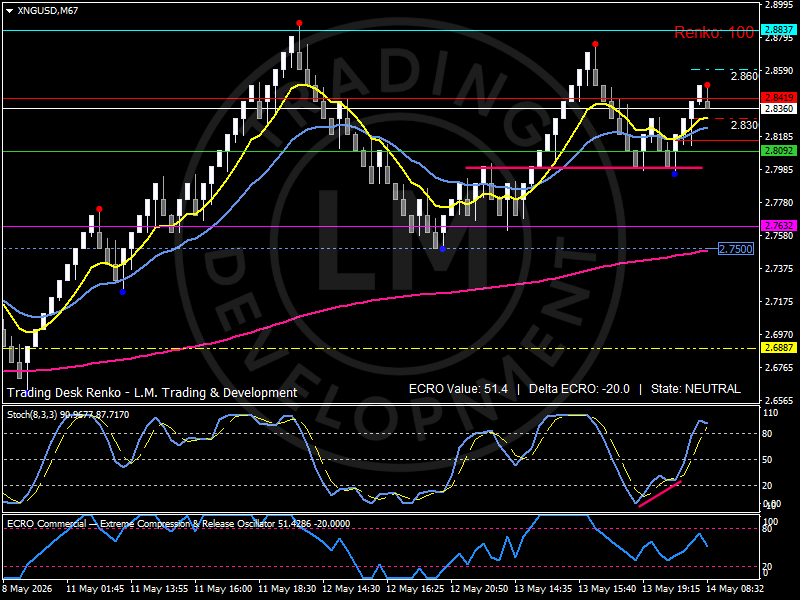

Technical structure: Natural gas consolidates above the 2.80 participation zone

Natural gas continues operating inside a constructive rotational framework centered around the 2.80–2.83 participation zone.

This region acts as the primary organizational layer of the current market structure, where price repeatedly pauses, rotates and rebuilds directional engagement following short term pullbacks.

The broader framework remains constructive despite recent momentum cooling.

Resistance develops near 2.86, where previous upward extensions lost continuity and generated rotational pauses across the structure. Acceptance above this zone would expose the broader 2.89 expansion layer.

Support develops around 2.80, followed by the stronger participation zone near 2.75, where buyers previously re-engaged aggressively during the latest recovery phase.

The EMA configuration continues supporting the broader framework. Short term averages remain aligned above the deeper participation layer while the market continues preserving constructive rotational continuity.

The Renko sequence shows alternating phases of upward extension and controlled pause while maintaining coherence across the broader structure. Higher reaction lows remain visible despite the latest pullback activity.

The ECRO indicator currently stands near 51 with a negative delta around -20, reflecting a neutral state where directional energy remains available while short term momentum cools following the recent expansion phase.

This configuration remains consistent with a market consolidating inside a broader constructive framework while awaiting the next directional catalyst.

Bird’s eye view: Natural Gas market map

Market Regime: Timing-sensitive rotational framework under elevated LNG risk.

Regime Pivot: 2.80–2.83.

Upper Participation Zone: 2.86.

Expansion Layer: Acceptance above 2.89 strengthens upside continuation.

Support Structure: 2.80 – 2.75.

Pressure Zone: A break below 2.75 weakens the broader recovery framework.

Systemic Indicators to Watch: LNG routing, Hormuz security, European refill dynamics, shipping stress and storage injections

Outlook

Natural gas continues operating inside a market increasingly shaped by timing efficiency, LNG routing and operational flexibility.

Shipping stress, terminal concentration and Hormuz related uncertainty continue tightening the tolerance for disruptions across the broader gas system while refill sensitivity remains active across Europe.

The current structure still supports constructive participation above the 2.80 zone as LNG flows continue preserving operational continuity across the broader network.

The next directional phase depends on how routing conditions, storage injections and geopolitical developments influence flexibility across the LNG system.

As long as shipping continuity remains active and refill conditions preserve stability, natural gas can continue maintaining engagement across the upper participation layer while the market absorbs elevated logistical and geopolitical sensitivity.

Author

Luca Mattei

LM Trading & Development

Luca Mattei is a market analyst focusing on FX, metals, and macroeconomic trends. He develops trading tools for retail and professional traders, coding indicators and EAs for MT4/MT5 and strategies in Pine Script for TradingView.