Japanese inflation quickened in March, complicating Bank of Japan outlook

Japanese inflation intensified in March despite the government's efforts to tame consumer prices. Even after policy effects, price pressures are strengthening and broadening. We still see an April hike possible if the BoJ gives priority to preventing inflation expectations from accelerating.

Inflation stronger than expected despite government subsidies

Japan’s headline CPI inflation rose 1.5% year-on-year in March (vs 1.3% in February, 1.4% market consensus) and core inflation excluding fresh food accelerated for the first time in five months to a 1.8% rate (vs 1.6% in February, 1.5% market consensus). The index increased by 0.4% month-over-month on a seasonally adjusted basis, reflecting increased pressure from goods, which rose by 0.6%, while services also increased by 0.2%.

Looking at the details, prices for fresh food (-4.8%), gasoline (-5.4%), utilities (-4.8%), and education (-5.5%) dropped. Fresh food prices dropped for four consecutive months, mostly due to a high base last year driven by rice prices. The last three price drops were due to government energy subsidies and social welfare programmes. Aside from these items, increases became more widespread with household goods (2.7%), transport (2.1%), and entertainment (2.35). Although core inflation is below 2% for a second month, excluding policy effects, inflation should stay well above 2%.

Inflation to accelerate further in coming months

We expect further inflation acceleration in the coming months. On top of rising global energy prices, the weak JPY should add more pressure on domestic prices. Producer prices and import prices increased quite sharply, too. Also, businesses usually adjust their retail prices in April, the first month of the fiscal year, which should further accelerate price gains. This year’s “shunto” negotiations resulted in wage growth above 5%, and increases for SMEs are quite firm as well. Thus, businesses are likely to pass these input cost hikes on to consumers.

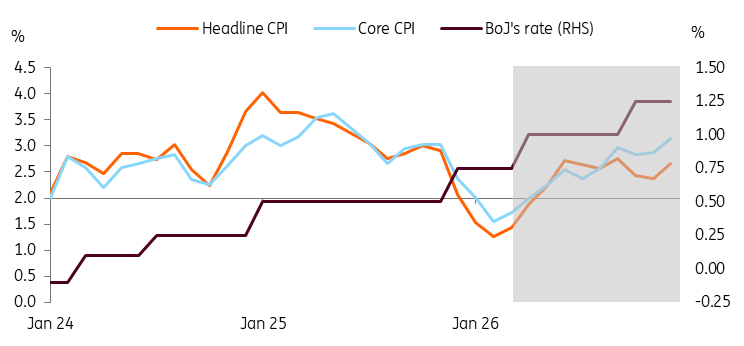

We expect Tokyo CPI (to be released on May 1) to rise to 1.7% YoY in April (vs 1.4% in March). We expect both good and service prices to rise more quickly in April. Also, from May, both headline and core inflation are expected to climb above 2% again. This should support the BoJ's further policy normalisation process. We currently have 50 bp hikes pencilled in by the end of 2026.

BoJ watch

Markets widely expect the BoJ to stay on hold after local wires quoted comments from people familiar with the matter saying the BoJ would not hike in April. We understand that the Middle East situation is fluid and uncertain. But in our view, recent data suggest that energy shocks are having a more prolonged and much larger impact on inflation than on growth. This will be reflected in the BoJ’s upcoming quarterly outlook report next week. We expect the inflation outlook to be revised sharply upward. Meanwhile, downward revision of growth should be limited. That said, this is a non-consensus call, but we still expect the BoJ to make a data-dependent decision on the hike. If the market is right about the BoJ skipping the hike in April, then the BoJ’s communication should give a much stronger signal for a rate hike in June.

Inflation is expected to grow faster, supporting the BoJ's rate hikes in 2H26

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.