January Flashlight for FOMC Blackout Period1

Executive Summary

If all goes according to the FOMC's plan, its January meeting will be considered a snooze. Consistent with the consensus, we expect the FOMC will keep interest rates on hold. Not only has the FOMC signaled it is comfortable with its current policy stance, but risks to the outlook have subsided, on balance, while recent economic data have been consistent with the Fed's outlook.

We will be watching closely for any guidance on how the Fed's response to recent funding pressure may change. The committee may decide to raise the interest rate that the Fed pays commercial banks on the excess reserves they hold at the Fed (i.e., IOER) to push the effective fed funds rate back toward the middle of the target range. That said, we view any increase in IOER, whether at this meeting or at subsequent meetings, as only a technical adjustment and not an indication of future policy changes. Meanwhile, there will be a new crop of voters as part of the regional Federal Reserve Banks' regular rotation, but we do not believe the new composition changes the policy outlook.

Reduced Risks and Soft Inflation Keep the FOMC in a Holding Pattern

Our view that the FOMC will keep rates unchanged at the January meeting stems from both the guidance in recent communications and recent data. Following its last meeting in December, the committee stated that the policy rate was "appropriate," a sentiment that has since been echoed in inter-meeting speeches and interviews. Even the FOMC's most dovish member, Neel Kashkari, who is a voting member of the FOMC this year, has said he is comfortable with the current stance of monetary policy.

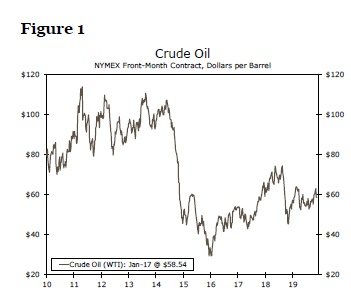

While risks to the outlook including trade policy, geopolitics and weak global growth remain elevated, they have subsided to some extent, with the exception of geopolitics, since the FOMC's last meeting. The United States and China signed Phase I of a trade deal on January 15, reducing the risk of further escalation in the trade war and taking some uncertainty off the table. Even with heightened tensions in the Middle East in recent weeks, oil prices are well within the past year's range and are far from posing a threat to real consumer spending (Figure 1). Global growth remains subdued, but PMIs continue to hint that activity is stabilizing.

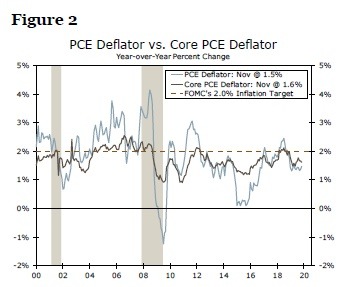

Recent readings on the U.S. economy have also indicated little need to change course. Hiring continues to be strong on trend and the unemployment rate remains at a 50-year low. Inflation is still struggling to meet the Fed's target, however (Figure 2). With households' inflation expectations near all-time lows and wage growth softening over the past year, most committee members do not seem compelled to take back last year's 75 bps of rate cuts even as risks to growth have ebbed.

Financial markets seem to be on board with the FOMC standing pat for the time being. Equity markets are at record highs, credit spreads are near the tightest levels this cycle and financial conditions broadly are the easiest in about six months. Currently, markets are pricing in no chance of a rate cut at next week's meeting.

Author

Wells Fargo Research Team

Wells Fargo