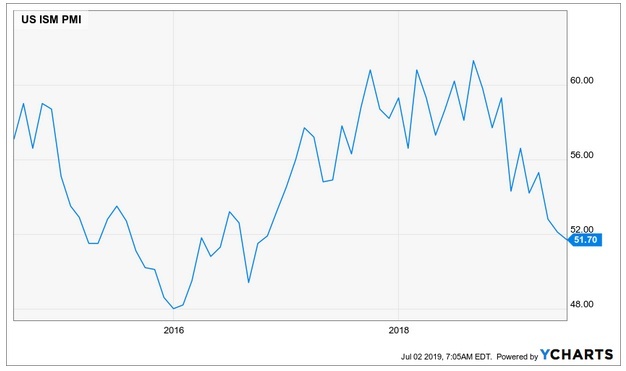

ISM manufacturing came in at 51.70, down from 52.1 the month prior

Highlights:

Market Recap: The S&P 500 rose 0.77% and 10-year yields rose 3 basis points on the back of the tariff truce with China. The U.S. Dollar was up 0.78% on the day, hammering Gold, which twas down -1.73%. Copper was also down -0.96%.

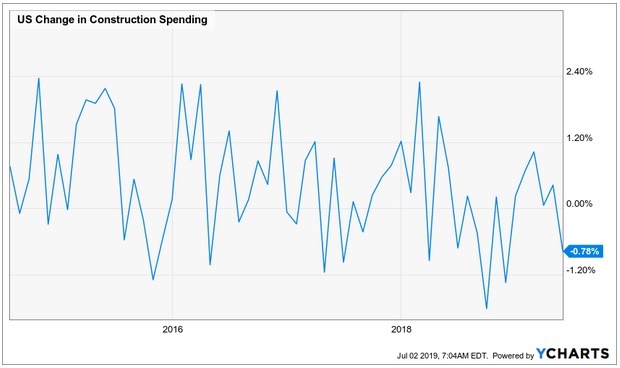

Economic Data: Yesterday we received ISM manufacturing data and construction spending. ISM manufacturing came in at 51.70, down from 52.1 the month prior. Construction spending was down -0.78% month over month.

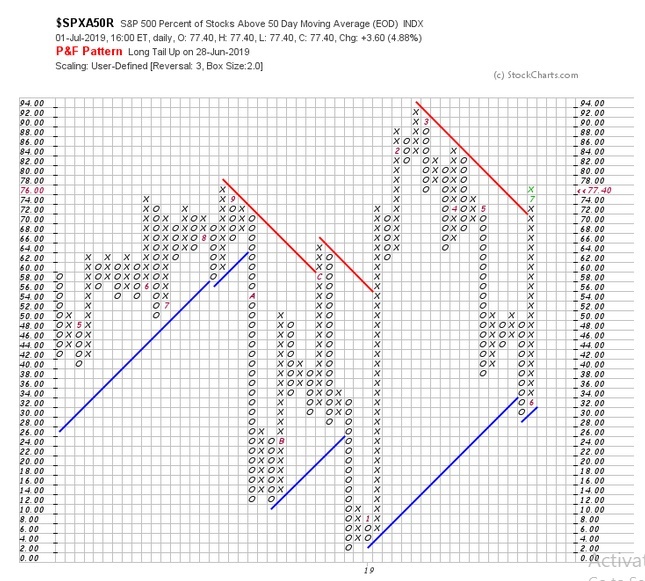

Market Internals: The percentage of stocks in the S&P 500 that are above the 50-day moving average continues to rise and is yet to be overbought. As long as it continues to strengthen, the market has the underpinnings of a continued rally.

Semiconductors: Semiconductors rallied against the S&P 500 over 1.90% yesterday. Semis are back above resistance and have broken out to new short-term highs. Semiconductors are in a positive trend. A breakout to new all-time highs relative to the S&P 500 would be a positive sign for broad markets.

Lumber/Gold: Lumber surged against gold yesterday after having a tough week last week. It is trying to find a bottom and is back above the 200-day moving average. Can Lumber continue to rally?

Oil: Crude oil rallied 1.06% yesterday, despite the move up in the dollar yesterday. Oil is still in a negative trend but is close to breaking higher. If tensions with Iran escalate, we would expect this to move higher.

U.S. Dollar: The U.S. dollar rallied 0.78% yesterday. It is back above the 200-day moving average. Will the dollar continue to rally with an easy Fed? Or will the Fed surprise the market and not cut rates in July, setting off a move higher in the dollar?

Futures Summary:

News from Bloomberg:

The U.S. added more EU products to a list of goods threatened with retaliatory tariffs in the long-running subsidy dispute between Boeing and Airbus. The $4 billion of goods includes cheese, cherries, pasta and whiskey. It adds to a list of $21 billion of products published in April. The EU has a case pending against Boeing and has readied retaliatory tariffs of its own.

President Trump said a new round of talks with China is underway and they began before he met Xi Jinping. He added that levies on Mexico are off the table after the country stepped up efforts to stem migrant flows. It's doing a great job and has had "a very big impact." Here's a guide to the U.S.-China trade dispute.

Saudi Arabia is reviving preparations for a potential IPO of Aramco, months after putting the planned listing on hold, people familiar said. Aramco recently held talks with a select group of investment banks to discuss potential roles on the offering, and detailed work may pick up speed later this year or early 2020. Here's a look at why the IPO stalled last time.

In other IPO news, AB InBev kicked off the biggest so far this year, offering 1.63 billion shares in its Asia Pacific unit at HK$40-HK$47 apiece. That may raise as much as $9.8 billion and value the company at up to $64 billion. The brewer's counting on Asia's growth potential as the beer business faces stagnating prospects elsewhere. Shares are expected to start trading July 19.

U.S. stock-index futures fell as investors sought haven assets on concern trade disputes may further slow economic growth. Equities in Asia and Europe drifted, with Hong Kong shares rising in a catch-up rally. Ten-year Treasury yields slid to 2.01%. Oil dropped with industrial metals.

Author

Clint Sorenson, CFA, CMT

WealthShield