Is a recession looming?

-

Wall Street skyrockets after Trump announces tariff delay.

-

But gains remain limited as Trade War with China continues.

-

Recession odds have eased, but investors remain fearful.

-

The worst may not be over, deeper market wounds still possible.

Trump delays several tariffs, but continues to hit China

With a new Trade War between the US and China unfolding, investors have been afraid that a recession may be looming for the US economy.

On so-called ‘Liberation Day’, US President Trump announced a 10% baseline tariff on all imports to the US, along with higher duties on some of the nation’s biggest trading partners. The 10% baseline duties went into effect on April 5, while the higher reciprocal rates that kicked in on April 9, were postponed by 90 days in less than 24 hours.

Wall Street skyrocketed that day, with the S&P 500 recording its biggest winning day since the Great Recession and the tech-heavy Nasdaq rallying more than 12%, the most since 2001.

That said, China had a different treatment. Following the announcement by the world’s second largest economy that they will raise levies on US products to 84% and proceed with restrictions on nearly 20 US firms, the US President raised the 104% tariff on Chinese imports to 145%.

The further escalation in the US-Sino trade conflict suggests that the worst may not be behind us, even after the 90-day pause announcement reduced the odds for a US recession. After all, no one can say with certainty that Trump will not change his mind in the following days.

Recession not fully factored in, but concerns remain

So, how likely is a recession, and how much of it did the markets price in?

Before the delay announcement, JPMorgan, which was among the most pessimistic commercial banks was estimating a 60% chance for a recession in the US, while Goldman Sachs was seeing 45%. Although the former bank maintained its forecast, the latter withdrew its recession odds, and it is now estimating growth.

What’s more, the Fed itself appears in no rush to lower interest rates aggressively, with Fed Chair Powell saying on Friday that this is not the moment for a “Fed put” – the term used for actions to shore up free-falling stock markets. This suggests that the Fed is not quite anticipating a recession, although they are acknowledging the increasing risks.

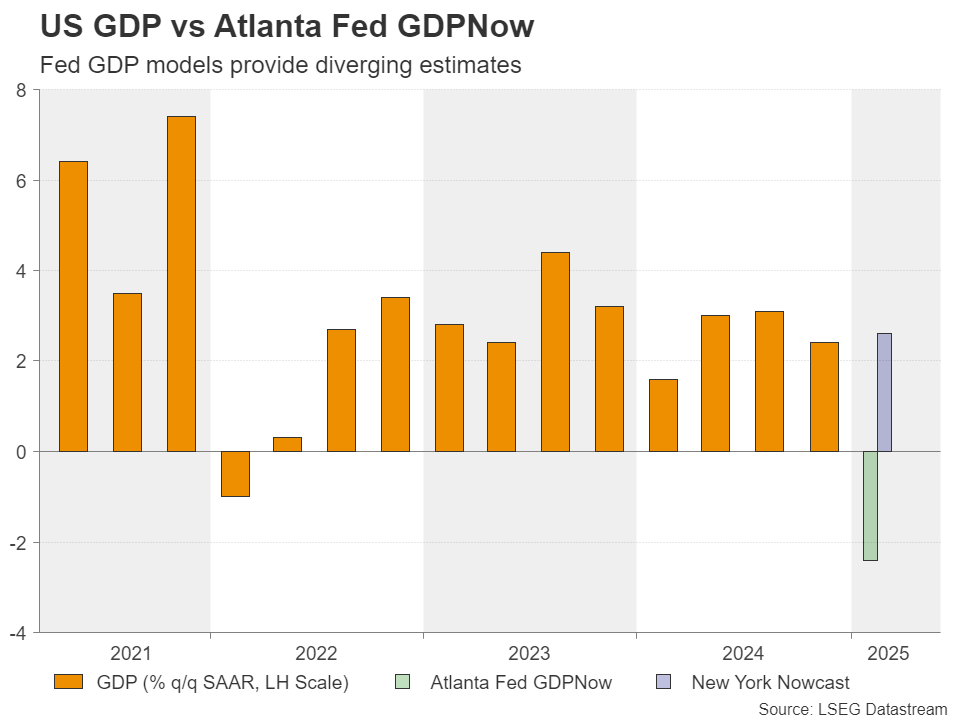

Fed models that estimate US GDP corroborate that view. Although the Atlanta Fed GDPNow model is expecting a 2.4% contraction for Q1, the New York Nowcast is anticipating a 2.6% expansion in Q1, and only a slowdown to 2.44 for Q2.

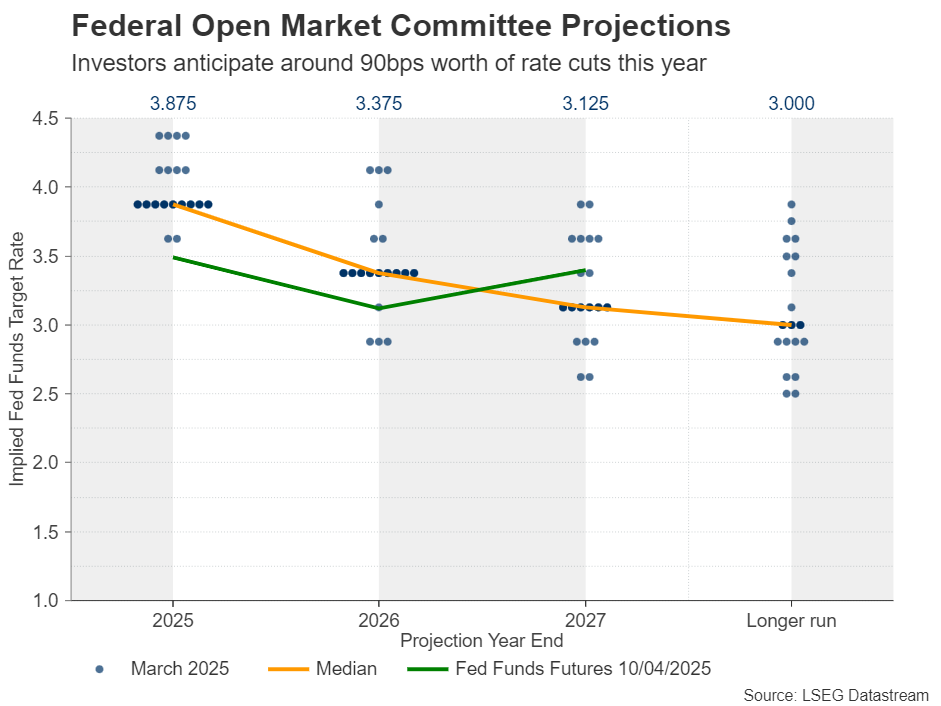

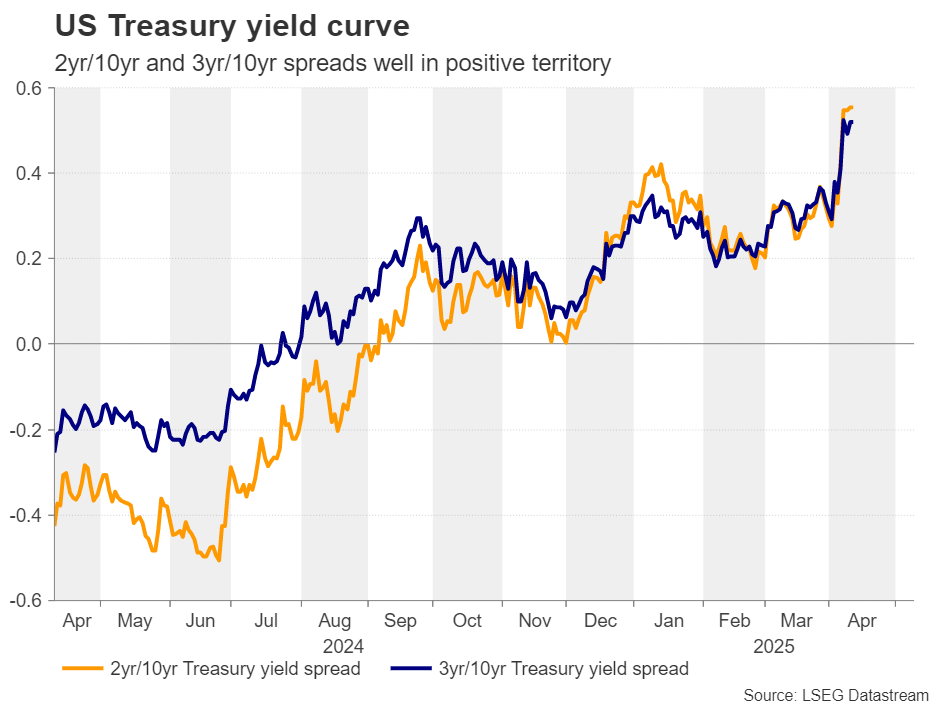

The market appears to be a bit more fearful, despite the impressive rally on Wall Street on April 9. After all, just the next day, equities pulled back again. Also, Fed fund futures are still pointing to around 90bps worth of rate cuts by the end of the year. Yet, investors are not certain about a recession, and this is evident by the fact that although that VIX – Wall Street’s fear gauge – surged to levels last seen during the COVID crisis, the US Treasury yield curve is not inverted.

Wall Street could still trade south

Therefore, there may be more to digest should the trade landscape worsen. Not only could US-Sino tensions intensify, but Trump could withdraw the delay adding pressure on the US allies to deal with a new reality. In other words, if the tit-for-tat tariff game between the US and other major economies continues, Wall Street may extend its decline as investors become even more convinced that a recession could occur this year.

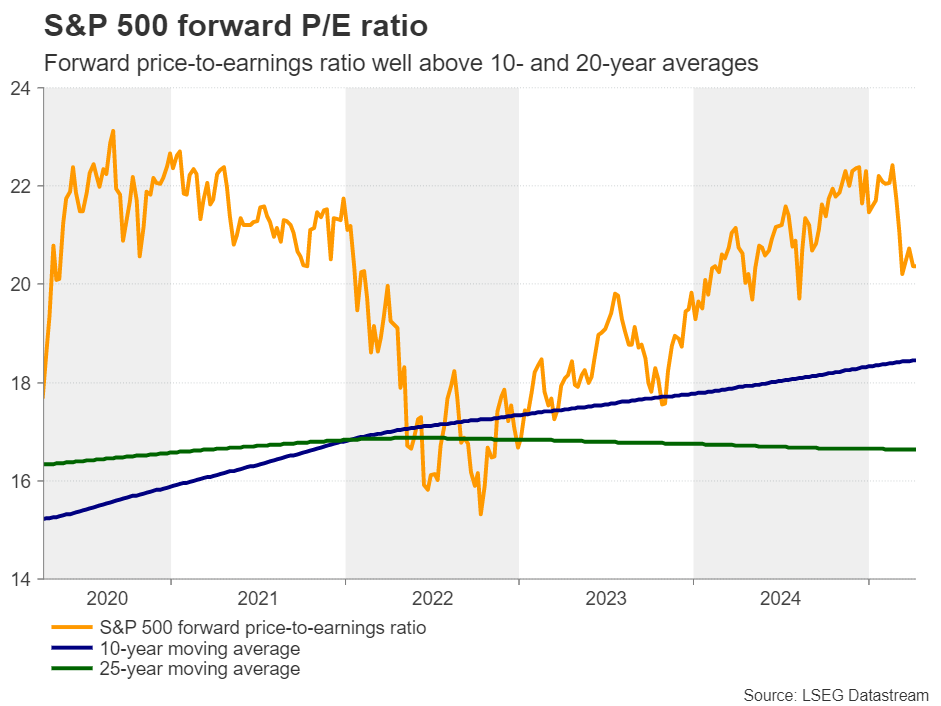

Looking at valuations, although the forward price-to-earnings ratios of stocks have fallen sharply, they are still at very high levels. For example, the forward P/E ratio of the S&P 500 is still above the levels seen in August 2024, and well above its 10- and 20-year moving averages. This adds more credence to the view that there may be more declines in store. Even bargain hunters may not feel comfortable to jump back into the action should things get worse.

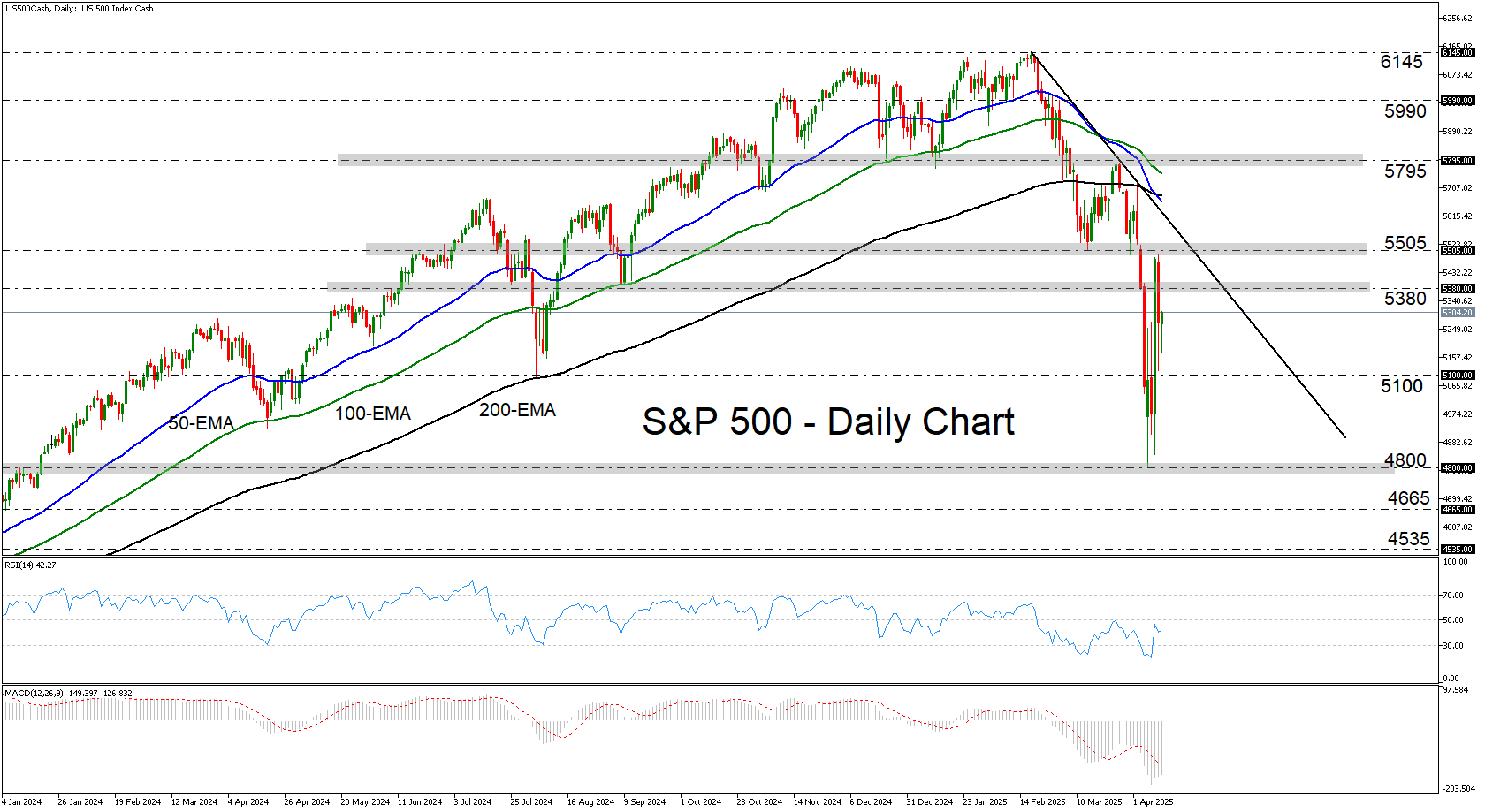

Despite impressive rally, S&P 500 remains below downtrend line

From a technical standpoint, the S&P 500 skyrocketed on Wednesday, but the rally was stopped near the 5505 zone, marked as support by the inside swing low of March 13. The bears took charge again from that zone, leaving the door open to further declines, as the index remains below all the plotted moving averages and below the downtrend line drawn from the high of February 19.

Should the bears stay in charge, they could aim for another test near the 4800 zone, the break of which would confirm a lower low and could aim for the 4665 and 4535 zones. For the outlook to turn positive, the index may need to stage a much stronger recovery than it did on Wednesday. Not necessarily within a day, but the price may have to rise above the peak of March 25 at 5795.

Author

Charalampos joined the XM Investment Research department in August 2022 as a senior investment analyst.