Iran has oil to sell, but Asia is not bidding

- Iran has supply, but not yet demand.

- China remains the key buyer, but refinery appetite looks weak.

- India is covered with Russian barrels and still wary of payment risk.

- The longer cargoes float, the larger the discount needed to clear them.

Asia is not bidding

Iran may have won the right to move barrels again, but getting oil onto the water is one thing. Finding a buyer is another.

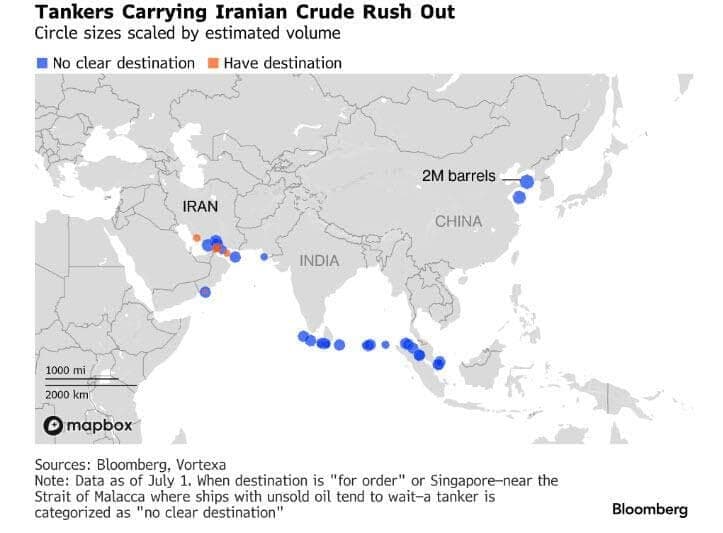

Since Washington opened a temporary window for Iranian exports, Tehran has moved quickly to push crude out of the Gulf and toward Asia. The problem is that the market is already full. More than 58 million barrels of Iranian crude and condensate are now floating offshore, with most cargoes showing no firm destination. “For orders” and Singapore are doing a lot of heavy lifting on tanker screens, which usually means the real work is being done quietly somewhere between the Malacca Strait, storage tanks, traders and discount negotiations.

Iran has until roughly mid-August to turn these barrels into cash. That matters not only for revenue, but for leverage. A country negotiating from a position of full tankers and no buyers is not negotiating from strength.

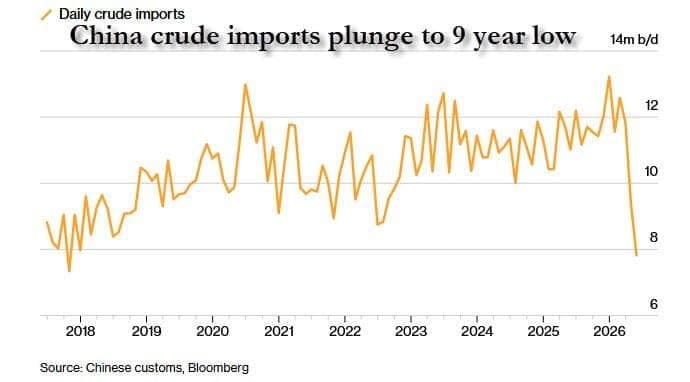

The obvious destination is China. It was always China. Independent refiners have been the natural home for discounted Iranian crude, while the state-owned refiners have little appetite to step in when banks, insurers and payment channels remain uncertain. But Chinese independent refinery runs are already weak, margins are compressed and domestic demand is not giving refiners much reason to chase extra barrels.

That is the real issue. Iran is not just competing against other Middle Eastern producers. It is competing against a market that has already bought heavily, has plenty of crude in the system and is not desperate for another cargo.

China’s imports of Iranian crude reportedly fell sharply in June, while a growing share of Iranian cargoes has been sitting idle in Asian waters for more than a week. That is never a great look when you are trying to demonstrate that sanctions relief has restored your export machine. The barrels may be moving, but they are not clearing.

India is also not riding to the rescue. Indian refiners already have Russian supplies secured into late summer, and there is still no clean answer around US-dollar payments or how durable Washington’s waiver really is. Nobody wants to load a cargo, arrange financing, insure the voyage and then find the political window slammed shut halfway through the transaction.

That uncertainty is probably the biggest reason buyers are standing back. The oil may be legal today, but nobody knows whether it will still be legal in thirty days. The risk is not the cargo itself. The risk is being left holding it when policy changes.

Iran can still move the barrels, but the price will have to do the talking. At a deep enough discount, Asian refiners can reshuffle supply, resell competing grades, free tank space and run harder. Cheap crude has a way of finding a home.

But the longer these tankers sit offshore, the more the market begins to smell distress. And once buyers sense distress, they do not rush in. They wait for the seller to blink.

For oil traders, this is the part of the post-conflict story that matters. The reopening of Hormuz removed the fear premium, but it also released a wave of deferred supply into a market that was already well stocked. Iran may have escaped the blockade, but it has sailed straight into a far less forgiving problem: too many barrels, too few natural buyers and a clock that is now running against it.

Author

Stephen Innes

SPI Asset Management

With more than 25 years of experience, Stephen has a deep-seated knowledge of G10 and Asian currency markets as well as precious metal and oil markets.