Iran deal takes Bank of England rate hike back off table

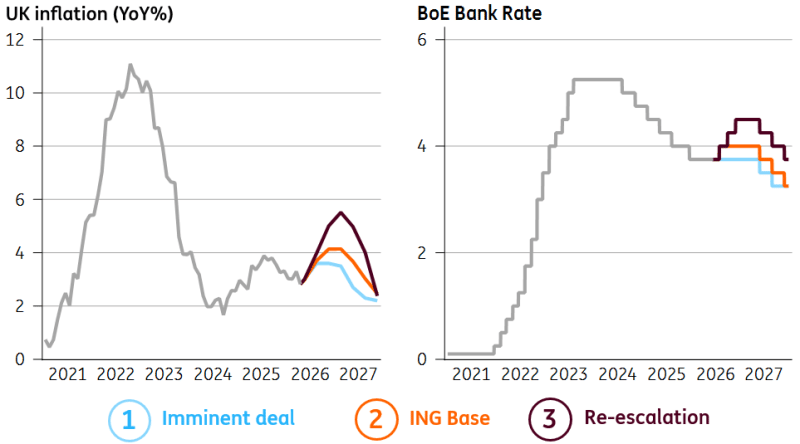

If the deal endures and oil starts flowing again, UK inflation would likely stay below 4% and enable the Bank of England to avoid a rate hike this summer. We expect a 7-2 vote in favour of 'no change' this Thursday.

A rate hike at this Thursday’s Bank of England decision had already become highly unlikely. And thereafter, the US-Iran deal has nudged the pendulum back towards a prolonged pause. Markets now price just a 25% chance of a July hike and only one rate increase this year, down from a peak of three.

Our view has long been that the Bank is somewhere between doing nothing and hiking once – and 4% inflation is an important line in the sand. The Bank argued last summer that when it exceeds that level, it’s more likely that inflation becomes more embedded and second-round effects more likely.

With energy prices where they are today, 4% inflation is unlikely. Natural gas futures for next winter and beyond are back to pre-war levels – and they play a big role in setting the quarterly household energy price cap. That cap is already set to rise 13% in July but if nothing changes, it’s likely to fall 7% in October. That would keep UK inflation between 3-3.5% through the autumn/winter. The bar for a rate hike wouldn't be met. Remember, the Bank argues that simply not cutting rates, as was otherwise likely, amounts to a de facto tightening of policy.

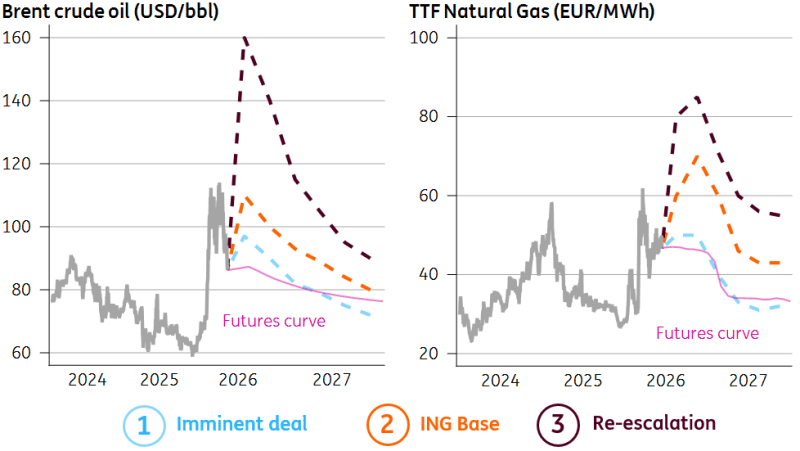

That said, our commodities team sees a decent case for energy prices to move higher again – even if the deal agreed this weekend endures. Oil inventories will need rebuilding, while Europe still needs to replenish its gas storage, which sits well below the seasonal average – at a time when Asia will increasingly compete with Europe for LNG supplies.

Even in a scenario where the disruption in the Strait of Hormuz eases significantly through June, our team sees oil averaging $97/bbl in 3Q. Natural gas prices could inch a little higher, too.

ING's scenarios for global energy prices

That still probably doesn’t warrant rate hikes, though. Our forecasts show inflation would peak around 3.8% in that scenario. And importantly, a sustained reopening of the Strait of Hormuz would shift the balance of risks on inflation. The tail risk of a long, messy period of disruption would diminish.

The problem comes if the US-Iran deal unravels or fails to prevent another summer energy spike. In a scenario where the Strait of Hormuz stays disrupted through June and July, our team reckons oil briefly spikes to $120/bbl in July and natural gas prices surge. That would take inflation above 4% next winter and would make it very hard for the Bank not to hike this summer. That was loosely our global base case when we released our latest numbers last week – and it’s why we tentatively added a July rate hike to our forecasts.

What ING's energy scenarios mean for the UK

All of that now looks less likely again, though time will tell. And as for this week’s meeting, in the absence of either new forecasts or a press conference, the main question is how many officials join Chief Economist Huw Pill in voting for an immediate rate hike.

Here, we’re likely to see a return to the old battle lines that existed on the committee before the war began. Back then, some officials – including Pill – argued that price setting behaviour had permanently shifted since the pandemic in a way that would keep inflation structurally higher. Megan Greene, who subscribes to that view, has all-but-said she’ll vote for a hike this week. Catherine Mann, another long-time hawk, could join her. We’re expecting a 7-2 vote in favour of no change this week.

But another four members – five if you include Governor Andrew Bailey, who sits somewhere between the two camps – argue that the risk of second round inflation effects have diminished since the last energy shock four years ago. And the latest data suggests they are right.

Headline inflation got pretty close to 4% last year on rising food prices. Yet the latest data shows minimal signs of that morphing into a more persistent bout of price pressure. The jobs market is still under pressure. And private-sector wage growth is likely to fall below 3% in the short-term, which is below the level the Bank said in February was consistent with a 2% inflation target over the medium-term.

That's ultimately why we expect a return to rate cuts in 2027 – something markets aren't currently pricing.

Author

James Smith

ING Economic and Financial Analysis

James is a Developed Market economist, with primary responsibility for coverage of the UK economy and the Bank of England. As part of the wider team in London, he also spends time looking at the US economy, the Fed, Brexit and Trump's policies.