Hungarian inflation slows more than expected in March

While headline inflation slowed in March, core inflation remained hot, and sticky price inflation increased. So, the overall picture can only be described as favourable with a bit of optimism. Inflation expectations also remain elevated, leaving no room for a change in monetary policy.

Decelerating headline inflation rate in March

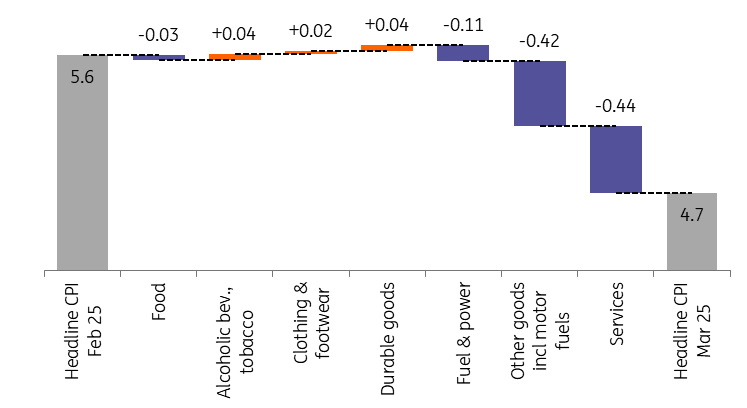

At first glance, March's inflation appears pleasantly surprising, coming in lower than expected. However, government communications already suggested that it had anticipated the indicator to drop below 5% year-on-year in March. What stands out is that this decrease is not primarily due to price controls, at least for now. On a monthly basis, the average price level remained unchanged in March, leading to a significant slowdown in the year-on-year inflation rate to 4.7%.

Main drivers of the change in headline CPI (%)

Source: HCSO, ING

The details

The slower pace of price increases is partly because food prices were unchanged on a monthly basis. We normally see stronger price increases in March due to seasonality, so some of the impact of the price freeze has already been felt. Price falls of up to 10% for some items suggest that either the data collected by the Statistical Office (HCSO) at the end of the survey period have been over-weighted, or the official food price fall in April could be even larger than previously thought, as the full impact will have been felt by then.

However, the real surprise was in services, where we saw a general slowdown. In this case, the monthly rate of price increases fell to just 0.3%, compared with a range of 1-2% in the previous two months. This suggests that the reassessment at the beginning of the year was more the result of one-off processes, i.e. the pass-through of earlier tax changes and a one-off large price adjustment due to wages.

There were also some upside surprises in March. Durable consumer goods rose more than expected, which could be a kind of pre-emptive decision in response to expected tariff changes. In addition, the seasonal rise in clothing prices was also stronger than usual.

The biggest one-off downward drag on the inflation rate came from a 4.1% monthly fall in fuel prices, roughly in line with our calculations. This item alone subtracted 0.3ppt from the monthly inflation rate.

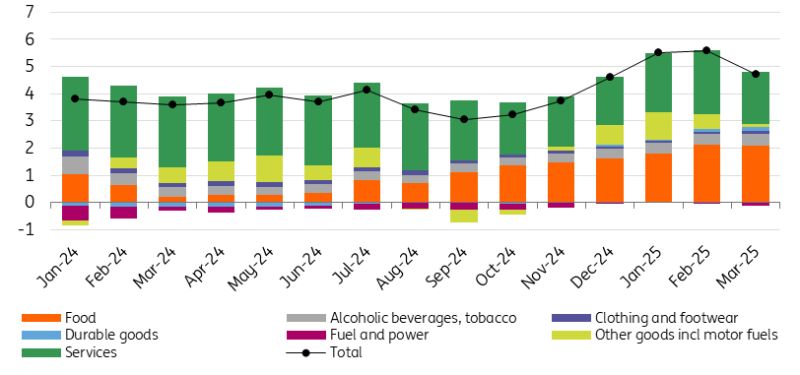

The composition of headline inflation (ppt)

Source: HCSO, ING

Underlying inflation remains a big issue

Looking at the annualised indices, the 0.9ppt slowdown in inflation is explained by the annual price developments of three main items: services and fuels, which made a downward contribution of 0.4-0.4ppt, and household energy, which made a negative contribution of 0.1ppt. Such a decline in services is mainly due to the base effect, as double-digit backwardation in the prices of contractual services (e.g. telecommunications, banking, insurance) was already noticeable at this time last year.

The impact of all these price changes on perceived inflation is difficult to assess at this stage. The key question will be whether consumers' inflation expectations can be brought down over the next month or two as a result of the price cuts. Given the temporary nature of the measure (as of now, the price cuts will end at the end of May), it may well be that neither perceived inflation nor inflation expectations will come down significantly. Especially if consumers still remember the unintended side-effect of the previous price control: a significant increase in the prices of other products. Indeed, the National Bank of Hungary's calculation shows that households' inflation expectations remain elevated after only a marginal decline in March.

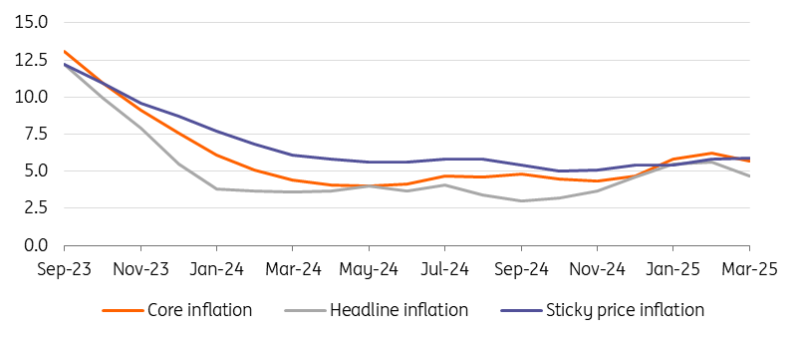

While it is at least encouraging that underlying inflation in services seems to be moderating, core inflation remains uncomfortably high at 5.7%, with sticky price inflation rising by 0.1ppt from February to March to 5.9% YoY, the highest pressure in the last 12 months.

Headline and underlying inflation measures (% YoY)

Source: HCSO, NBH, ING

We are lowering our forecast for the year due to the March data

There are still many question marks over the April inflation indicator, especially for food prices. In addition, it is expected that the inflationary price increases of telecommunications companies will only be reflected in the April indicator (a monthly change of 3.4-3.7%). Thus, there are still many uncertainties, and the underlying inflation process is still too strong, which should make the National Bank of Hungary cautious.

Indeed, in the current situation, premature monetary stimulus would create a new inflation shock through a further depreciation of the forint, which has already been damaged by the stock market meltdown in recent days.

Following the March inflation print, we have again revised our forecast for this year. For the rest of the year, we expect the rate to fluctuate between 4.0% and 5.5%. On average, inflation will be around 5% in 2025 (previous forecast: 5.4%). The current global market volatility and the impact of the trade war pose a balanced near-term risk to inflation, in our view. Upward pressure from a weakening forint and downward pressure from the collapse in energy-related commodity prices could offset each other in the short term.

Read the original analysis: Hungarian inflation slows more than expected in March

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.