How the war in Iran is impacting EM sovereigns

Renewed military action in Iran has driven a spike in energy prices and general risk-off sentiment, with Gulf Cooperation Council sovereigns feeling the pain from increased geopolitical risk, and EM credit in general facing a tougher macro backdrop.

Energy price spike drives a divergence across EM exporters and importers

The key global macro impact we have seen from the latest events in the Middle East is the significant spike in energy prices, with Brent crude up more than $82/bbl from below $70 in the middle of February and below $60 in late December.

For EM sovereigns, the impact is somewhat divergent, with large energy importers likely to feel the pressure of higher oil and gas prices in terms of price pressures and worsening external balances.

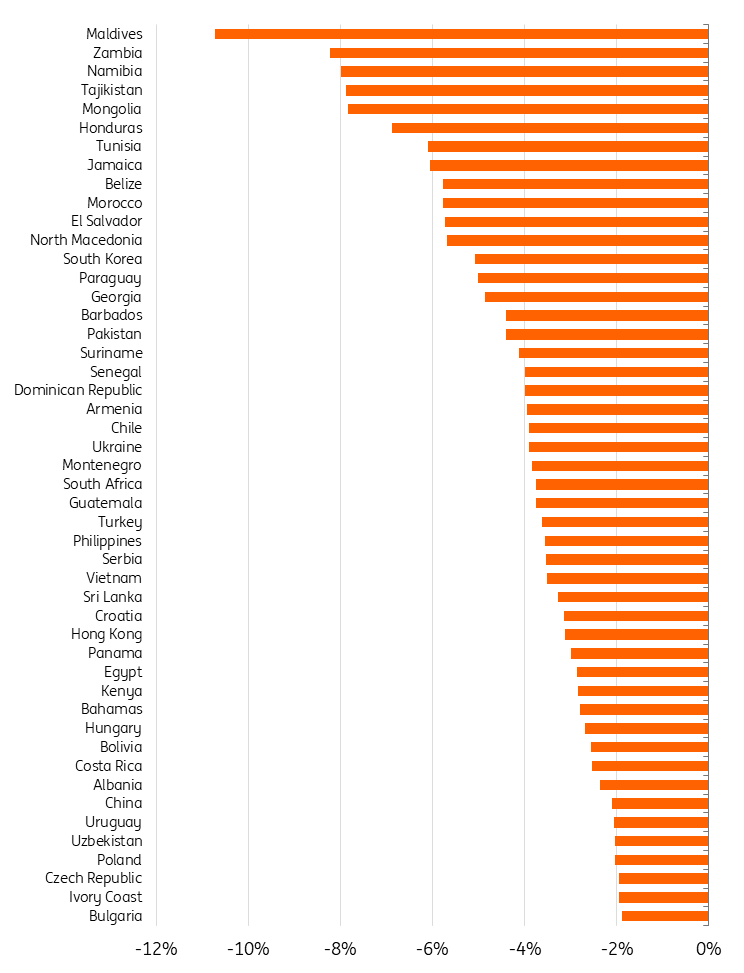

Given the experience of the gas market volatility in 2022, CEE sovereigns will understandably be in focus, with North Macedonia, Serbia, Hungary and Turkey the most exposed in CEE. They are far from outliers in the EM space, however, with large energy deficits seen in African frontier sovereigns such as Zambia and Senegal, along with Panama and El Salvador in Latin America, and Pakistan in Asia.

Net fuel imports as a % of GDP for significant importers

Source: ITC, UN COMTRADE, IMF, Macrobond, ING

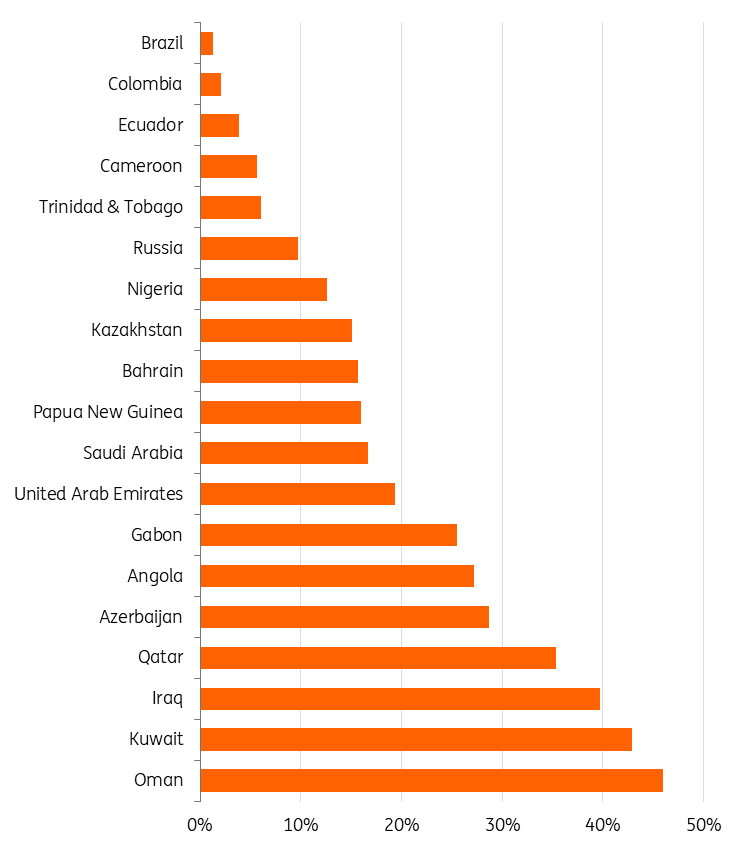

The flip side of this dynamic, of course, is that oil exporters generally should benefit from the spike in prices. The likes of Oman, Kuwait and Qatar broadly see a net fuel surplus of over 30% of GDP, with the caveat that the security risks for these credits in the region are likely to outweigh the benefits of higher oil prices.

In turn, investors will likely look to oil exporters outside the region as potential beneficiaries – in Africa, this includes Angola, Gabon and Nigeria. In Central Asia, Kazakhstan can also be seen as a beneficiary of higher oil prices.

The situation is somewhat more complex for Azerbaijan, given the country borders Iran and has a history of tense relations, while maintaining good relations with Israel. The Azerbaijani Foreign Minister Jeyhun Bayramov expressed his condolences to his Iranian counterpart Abbas Aragchi over the death of the country’s supreme leader, while emphasising ‘it is impossible for any country to use the territory of Azerbaijan against neighbouring and friendly Iran’. Last year, Iranian President Masoud Pezeshkian ‘urged’ his Azerbaijani counterpart Ilham Aliyev to investigate if Israel used Azerbaijani territory to launch attacks on Iran.

Net fuel exports as a % of GDP for significant exporters

Source: ITC, UN COMTRADE, IMF, Macrobond, ING

Regional impact varies but sentiment weakens for GCC

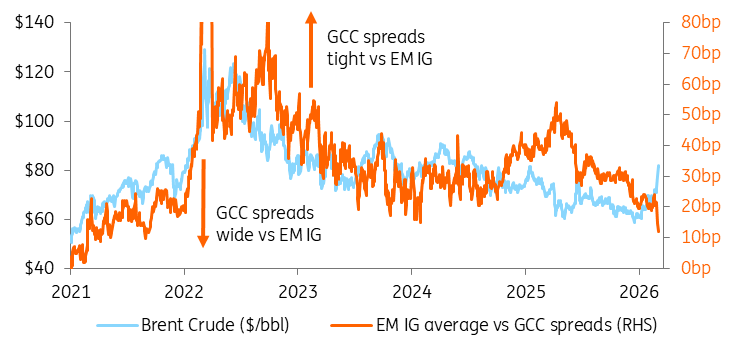

As previously mentioned, while higher energy prices should be a net benefit to oil exporters in the Middle East, the consequent security and geopolitical risks are outweighing this for now. For the GCC country group in particular, the correlation between oil prices and sovereign risk premium has broken down, with the spike in oil prices translating to relatively wider spreads for GCC sovereigns vs Investment Grade peers.

This has come amid Iran’s retaliation against both military bases and oil and refinery facilities across the GCC, along with the risk for tanker traffic that can impact export routes.

Oil prices versus GCC sovereign spread differential

Source: ICE, Refinitiv, Macrobond, ING

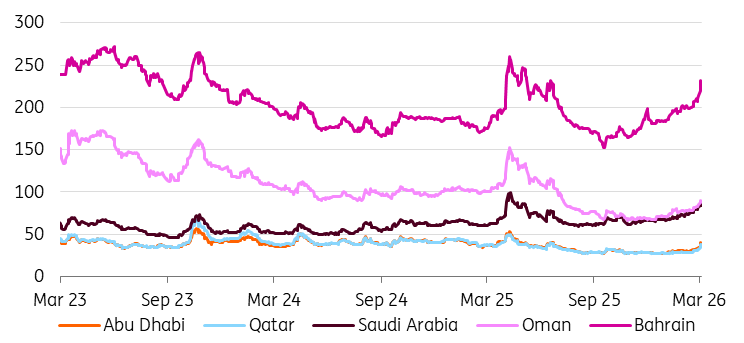

Once again, this impact should not be seen as uniform across the region. Across the GCC, Bahrain is clearly the most vulnerable from a credit perspective, with a far weaker balance sheet than the rest of the region and deteriorating fundamentals, made more stark by the improvement of Oman in returning to an investment-grade rating last year.

Oman itself can be viewed as the most openly neutral country diplomatically in the region, calling for immediate de-escalation, although it has still faced drone attacks. The country also would appear to be less constrained by export disruption to the Strait of Hormuz. In contrast, Qatar is heavily reliant on the Strait of Hormuz for LNG exports.

For the UAE, the hit to tourism, travel and transit will be key in terms of length of disruptions, while also coming at a tough time for hard currency bonds with the nation being removed from J.P. Morgan’s EMBI bond indices (albeit due to essentially ‘graduating’ from EM status).

For Saudi Arabia, disruption to energy infrastructure is the key risk to watch, while the country does at least have potential alternative export routes via the Red Sea – Pakistan’s Ministry of Energy recently requested supply through the Port of Yanbu on the Red Sea to help meet energy requirements.

GCC 5-year CDS spreads (bp)

Source: Refinitiv, ING

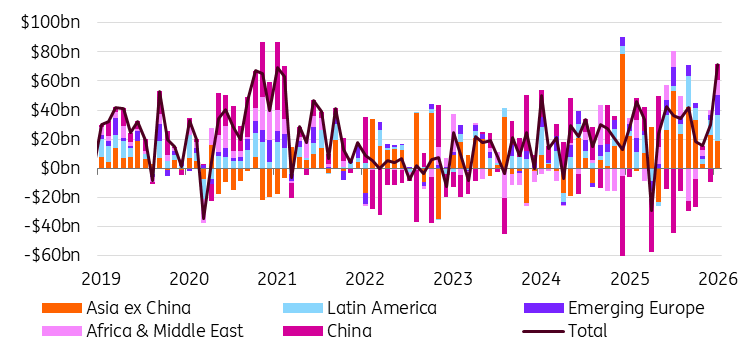

Risk-off mood may reverse the improvement in EM sentiment

More broadly on the global backdrop, the combination of a stronger dollar, higher UST yields and broad risk-off sentiment is a tough combination for EM credit markets. Once again, much is dependent on the duration and intensity of military action, but a key point to note is that the latest developments come on the back of a broadly positive shift in investor perceptions towards EM over the past year.

We have seen broad-based inflows into EM assets since ‘Liberation Day’ last year, including strong portfolios generally into EM debt across regions to start the year.

More recently, the strong pace of primary issuance has understandably taken a pause, while there remains the risk of a more prolonged reversal of these inflows into EM if the narrative around the asset class shifts from the more positive consensus seen to start the year.

Monthly EM debt portfolio flows

Source: IIF, Macrobond

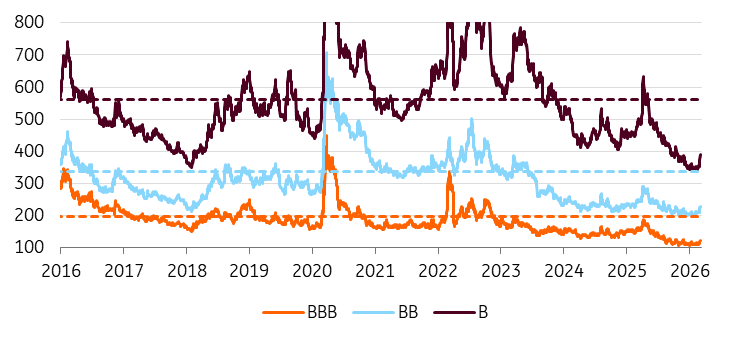

Further to this point, the broad grind tighter for EM credit has seen spread levels touching near all-time lows, with spreads significantly tight to long-term averages across all rating categories heading into the latest bout of volatility. We have since seen a relatively orderly sell-off, but the move so far barely registers as a blip in the longer-term picture – if a longer conflict and further global disruption persist, we should expect to see a further decompression of spreads from here, with single-B spreads on higher-beta, frontier names potentially at risk.

Egypt is one example of a name that has become an investor favourite and rallied strongly over much of the past year, but is now facing regional risks that could hit transit, tourism and remittance receipts.

EM USD sovereign index spreads by rating tier (bp)

Source: Refinitiv, ING

Read the original analysis: How the war in Iran is impacting EM sovereigns

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.