Hot, hot inflation

First 4,136 served as S&P 500 support, then 4,154 – stocks disregarded weak bond market posture, and half of the intraday progress in driving non-tech stocks lower, was lost. Yesterday was special in that the advance-decline line registered over -900 while the 500-strong index rose solidly.

The explanation is of course tech AI chase, and NVDA exuberant guidance based – tech market breadth deteriorated as well, and the stock market leadership became even narrower than it had been in recent weeks and months.

What‘s new, is the relief over the debt ceiling 2-year deal optimism – resolution in the making that still has to pass both chambers. Outshining inflation, tight lending, rising bankruptcies, deposits outflow and other signs of approaching recession such as no end in sight to declining LEIs. Those National Financial Conditions index the Chicago Fed publishes, would soon turn up, and see Treasury reversing position and withdrawing liquidity through replenishing its TGA at the Fed.

Keep enjoying the lively Twitter feed via keeping my tab open at all times (notifications on aren't enough) – combine with Telegram that always delivers my extra intraday calls (head off to Twitter to talk to me there), but getting the key daily analytics right into your mailbox is the bedrock.

So, make sure you‘re signed up for the free newsletter and make use of both Twitter and Telegram - benefit and find out why I'm the most blocked market analyst and trader on Twitter.

Let‘s move right into the charts – today‘s full scale article contains 4 of them.

S&P 500 and Nasdaq outlook

4,154 `has become support again, breaking which requires further swing in Fed tightening bets (as if 11% odds of two rate hikes till Jul weren‘t enough). Jun 25bp are priced in, yet the disconnect to expecting cuts in autumn, and between rising yields and tech being frantically bid up (AI stealing ever greater share of the appreciation), persist – slight improvement in the former, with even narrower leadership disregarding retail, banking, industrials and materials in the latter.

Needless to say, the times when tech was the sole outperformer while the rest lagged badly, which is true also about discretionaries, didn‘t end up well for the S&P 500.

Bears aren‘t going to have a field day today – 4,136 is in no way on the table. A little to no upset core PCE figure would result in rally continuation, and overcoming 4,177 with 4,188 – there will be attempts to shake off disappointments even if that means more hawkish Fed as a consequence. Higher targets require cooperation from non-tech, and that won‘t come today too easily.

Sell the news reaction to debt ceiling deal accompanied by dollar appreciation is on the table as money would flow away from the tech hiding place into inordinately beaten down long Treasuries (10-y yield is 3.83% already, and looking at rejection before getting much closer to 4%).

Also, the week preceding Memorial Day is usually a down one, but stock market gains next week (i.e. the week containing Memorial Day) happen more often than not.

That means if you‘re willing to jump in and out fast, you can take the upcoming intraday dip while benefiting from whatever upside next week brings – as a hedge to the medium-term bearish position.

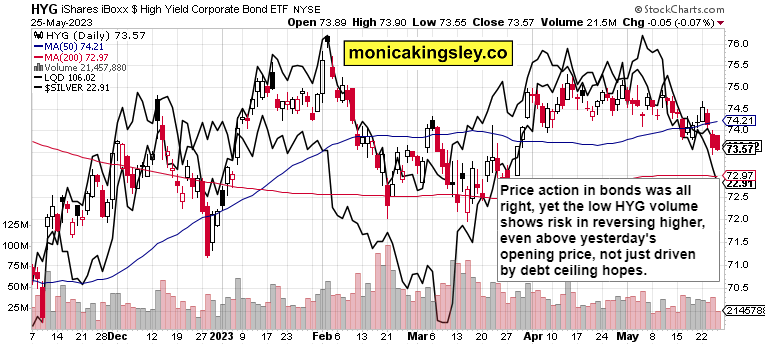

Credit markets

Pause in declining bonds seems at hand, and truly strong stock market bullish spirits would require high betas kicking in – last Wednesday‘s feat though won‘t be replicated I‘m afraid. I‘m looking for a modestly bullish turn up only.

Author

Monica Kingsley

Monicakingsley

Monica Kingsley is a trader and financial analyst serving countless investors and traders since Feb 2020.