Hawkish Fed drives the Dollar up

The Fed held the funds rate at 3.5-3.75% on Wednesday 17 June as widely expected but the dotplot suggested that at least one hike by the end of 2026 is more likely than many participants had expected. This article summarises recent changes in expectations for the Fed by the end of the year then looks briefly at the charts of EURUSD and USDCAD.

At least one hike looking likely in 2026

Traders had almost universally expected the Fed to hold on 17 June but there was considerable uncertainty about the timing of hikes. There was a reasonable possibility before the latest meeting that the Fed might hike as early as September 2026. That now seems to be the base case, though still with some uncertainty, since a majority of about 63% of participants at the time of writing expect at least one hike by 16 September according to CME FedWatch.

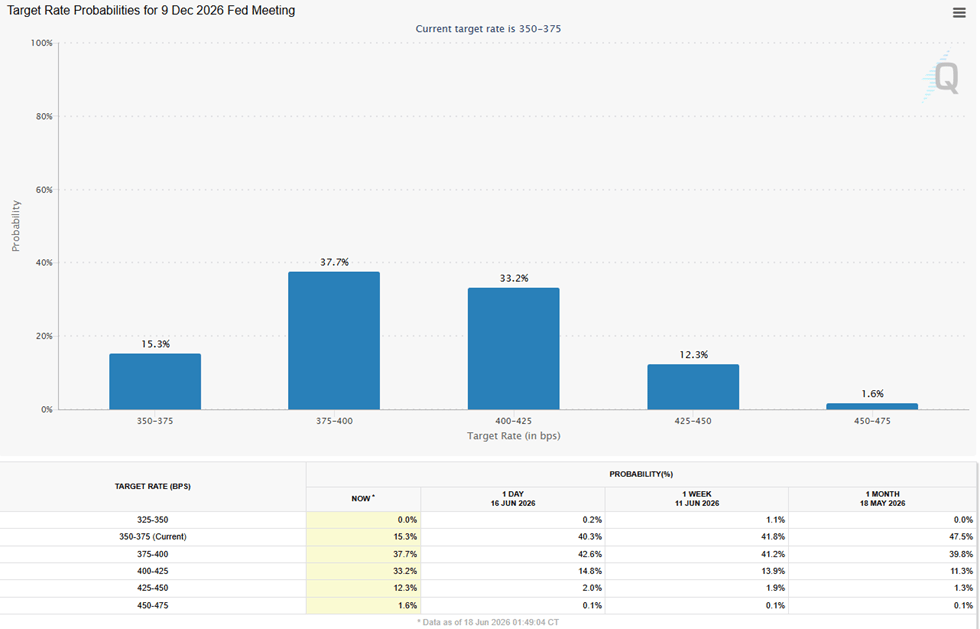

There has also been a significant change to FedWatch in December 2026, with the large majority of participants now expecting at least one hike by then:

The probability of a hike by the Fed in December 2026 surged dramatically after the meeting on 17 June with a large majority of participants now expecting at least one hike by the end of the year. Source: CME FedWatch

Before 17 June, the probabilities of the Fed holding into 2027 and hiking once this year were approximately even, but now the likelihood of a hold to the end of the year seems very low. Expectations for two or more hikes rose to nearly 45%.

Background to the Fed’s hawkishness: Inflation and jobs

Likely stick energy inflation seems like a probable scenario. The Fed’s statement on 17 June made specific reference to inflation being above the target of 2%. However, while a sustained drop by inflation over the next few months is unlikely it’s still a possible scenario. 2021’s inflation wasn’t being ‘transitory’ as the Fed initially expected; it wouldn’t be very surprising to see oil dropping, the job market returning to 2025’s averages and a hike by the Fed becoming less likely in late summer and autumn although currently this scenario is unfavourable.

March-April 2026 were the first consecutive months with positive NFPs for about a year. The job market in the USA seems resilient for now; however, that could change quickly as seen last summer. It’s probably too early to hail three good NFPs in a row as being a confirmed positive trend in the job market, so some traders might wait for at least a couple more strong job reports before being confident in the more hawkish possibilities for the Fed.

There was some early insight into Kevin Warsh’s likely approach as the Fed’s new chairman from the statement on 17 June. The word count was cut significantly from the norm under Jerome Powell and the syntax and vocabulary were overall much simpler than what one would normally expect from a central bank. Dr Warsh has criticised the Fed’s tendency to give too much forward guidance indirectly, so it seems that he’s started to do something about this.

Euro-Dollar might have more room to fall

On the four-hour chart of euro-dollar, the down candle around the Fed’s meeting and press conference is clear and accounts for almost all of the loss on 17 June, with the price having briefly touched a low of nearly three months before a modest recovery. While the ECB hiked its rates less than a week before the Fed, the divergence between the main refinancing rate and the Fed’s funds rate remains 1.1-1.35% and is now unlikely to shrink much if at all by the end of 2026. Overall economic conditions seem to favour the dollar with higher inflation, a stronger job market and much better growth in the USA compared to the eurozone.

The obvious longer term target for selling would be around $1.14 but it’s questionable whether the price might continue that far in the near future. However, with volume having remained relatively low apart from during the Fed’s comments on 17 June and the moving averages bunched closely together not far above the price, an ongoing strong bounce also seems unlikely. Traders are looking ahead to PCE and final US GDP for the first quarter on 25 June for the next possible data-driven movement.

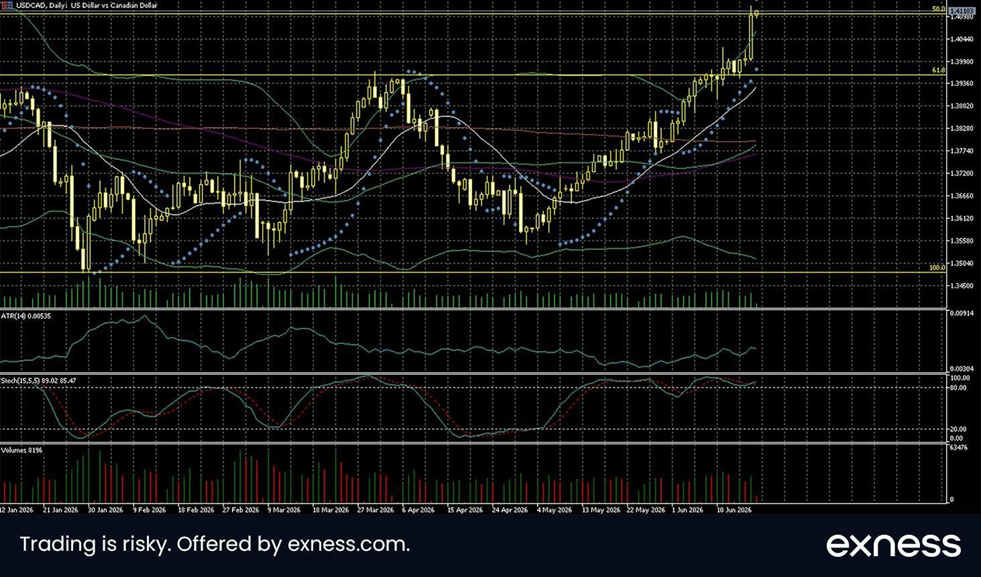

Dollar-loonie’s decisive breakout

Dollar-loonie reached seven-month highs above $1.41 on 18 July in the aftermath of the Fed’s meeting. The Fed raised its forecasts for inflation significantly while commenting on the overall robust job market in the USA. Meanwhile the Bank of Canada held at 2.25% at its last meeting and commented that inflation is likely to rise to around 3% later this year before declining. The difference in rates of 1.25-1.5% currently is very likely to increase towards the end of the year, favouring the US dollar.

The recent breakout above resistance has been extremely strong and might be running out of steam. $1.396 was the area of a likely strong resistance for much of 2026 so far having been late March’s high and the zone of the 61.8% weekly Fibonacci retracement. Now that it’s been broken and the price is testing the 50% Fibo, failure to break further above might lead to a short-term move down back towards $1.40 before the uptrend possibly resumes.

Immediate, strong continuation seems questionable given the force of the overbought signal from both the slow stochastic and Bollinger Bands while volume overall hasn’t increased strongly. The 38.2% Fibo around $1.425 might be a potential stretch target after a retracement lower and consolidation above $1.40. The 50 SMA from Bands is about to golden cross the 200. The primary focus on the calendar in the next few days is Monday 22 June’s Canadian inflation but traders will also monitor trade and US-Iranian talks.

Author

Michael Stark

Exness

Michael has been investing since 2007 and trading CFDs since 2013. He favors considering both fundamental and technical analysis where possible, with a focus on swing and position trading.