Gold faces credibility test as hawkish Fed reshapes expectations

Key takeaways

Gold enters the European session after a volatile Federal Reserve reaction that ultimately left the metal trading near key resistance levels rather than extending lower.

Markets focused less on the unchanged policy rate and more on a hawkish shift in economic projections, higher inflation expectations and a more restrictive policy outlook.

Treasury yields and the US dollar remain the dominant transmission channels influencing gold positioning.

The current structure suggests markets are reassessing credibility pricing rather than engaging in outright liquidation.

Gold enters a new credibility phase after the Fed

The Federal Reserve delivered one of the most closely watched policy decisions of the year.

The rate decision itself contained few surprises.

The broader message did.

Investors entered the meeting focused on the possibility that easing inflation and moderating growth could support a more accommodative policy trajectory over the coming quarters.

Instead, policymakers delivered a framework that appeared more cautious regarding future easing and more attentive to lingering inflation risks.

Updated projections reflected firmer inflation expectations and a policy path that remains restrictive for longer than many investors had anticipated.

The immediate market response reflected that adjustment.

Treasury yields moved higher.

The US dollar strengthened.

Rate expectations shifted.

Gold reacted accordingly.

Yet the most interesting aspect of the reaction was what happened next.

The initial decline failed to develop into a broader liquidation event.

Instead, the market stabilized and rapidly recovered much of the post-announcement weakness.

That behavior suggests investors are reassessing positioning rather than abandoning the metal.

Treasury yields remain the dominant transmission channel

The most important consequence of the FOMC meeting is the renewed emphasis on yields.

Gold continues operating primarily through a credibility framework.

The transmission mechanism remains straightforward.

Federal Reserve expectations influence Treasury yields.

Treasury yields influence real yields.

Real yields influence the opportunity cost of holding non-yielding assets.

That process remains the central driver of gold pricing.

The latest Fed projections reinforced the idea that policymakers remain unwilling to declare victory over inflation.

As a result, markets have become more cautious regarding future easing expectations.

The adjustment has been visible across rates markets, dollar positioning and broader asset allocation decisions.

For gold, that environment creates a more challenging monetary backdrop.

At the same time, it also increases the importance of credibility as an investment theme.

Investors continue evaluating whether inflation is genuinely moving toward long-term policy objectives and whether current policy settings can maintain that trajectory.

Gold remains directly exposed to those questions.

Positioning remains more resilient than the headlines suggest

A superficial reading of the FOMC outcome would suggest a straightforward bearish development for precious metals.

Market behavior tells a more nuanced story.

The rapid recovery from the post-announcement decline indicates that participation remains active.

Investors are not treating gold as a simple directional trade on policy expectations.

The metal continues attracting interest as a reserve asset and macro barometer during periods of policy uncertainty.

That distinction matters.

Gold is not only responding to current interest rates.

It is responding to confidence in the long-term credibility of the policy framework itself.

The stronger the debate surrounding future inflation, growth and monetary policy, the more relevant that role becomes.

This helps explain why the market recovered despite higher yields and a firmer dollar.

Positioning appears more balanced than the immediate headlines imply.

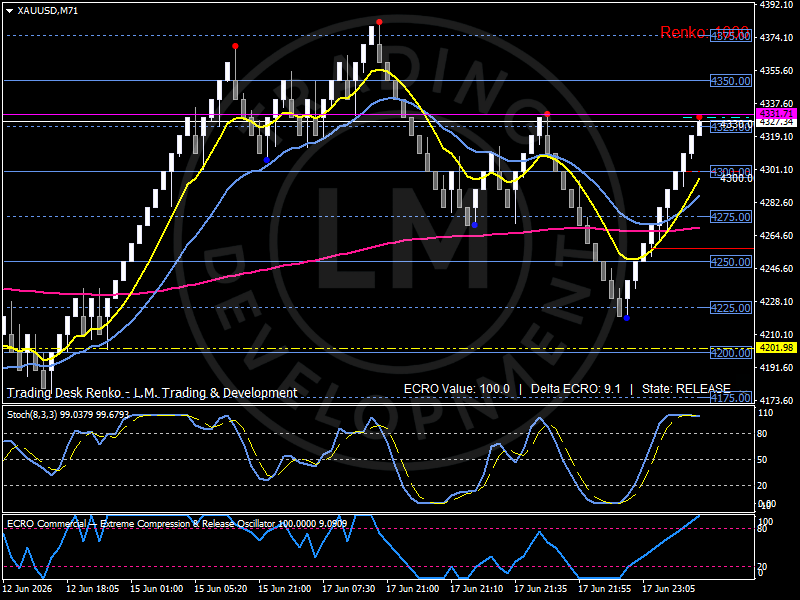

Technical structure: Gold challenges resistance after absorbing the Fed shock

The technical structure reflects a market that has absorbed a significant macro catalyst without breaking down.

On the H4 framework, the immediate post-FOMC decline was sharp but short-lived.

Price quickly recovered toward the center of the broader trading range, suggesting that downside conviction remains limited.

The Renko structure reinforces that interpretation.

Following the decline toward the 4225 region, participation returned aggressively.

Gold reclaimed the 4250 level and subsequently advanced toward the major participation corridor around 4325–4335.

The ECRO indicator has reached 100 and remains in a release state, highlighting exceptionally strong participation conditions.

Momentum remains elevated.

Resistance now concentrates around 4325–4335, followed by the broader structural ceiling near 4350.

Support remains anchored near 4250, while deeper stabilization continues developing around 4225 and 4200.

The overall configuration remains consistent with a market testing resistance after a significant macro repricing event.

Bird’s eye view

Gold currently operates inside a credibility-driven market where Treasury yields, Federal Reserve expectations and dollar positioning remain tightly interconnected.

Yesterday's FOMC meeting shifted attention away from the policy rate itself and toward a more restrictive long-term policy outlook. Treasury yields moved higher and the dollar strengthened, increasing the importance of credibility pricing across financial markets.

Structurally, gold has recovered from the post-FOMC decline and is now challenging the 4325–4335 resistance corridor, while 4250 remains the primary participation pivot and 4200–4225 the broader stabilization zone.

The dominant variables remain Treasury yields, real yields, dollar positioning and inflation credibility.

Outlook

Gold enters the remainder of the week facing an environment where policy expectations have become more restrictive but investor participation remains resilient.

The Federal Reserve has reinforced the importance of inflation credibility and long-term policy discipline.

Markets must now determine whether higher yields and a stronger dollar can generate sustained pressure on precious metals or whether investors continue viewing gold as a strategic reserve and credibility asset.

The next directional phase will likely emerge from the interaction between Treasury yields, dollar positioning and evolving expectations regarding inflation persistence.

Author

Luca Mattei

LM Trading & Development

Luca Mattei is a market analyst focusing on FX, metals, and macroeconomic trends. He develops trading tools for retail and professional traders, coding indicators and EAs for MT4/MT5 and strategies in Pine Script for TradingView.