Global macro transmission monitor – Week ending May 15, 2026

How macro shocks propagated through FX, commodities and rates last week

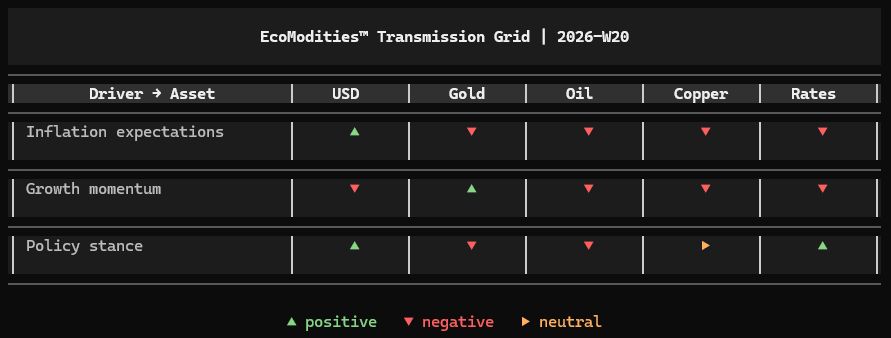

Executive transmission map

US inflation data dominated the macro transmission chain last week as CPI stabilized while producer prices accelerated materially above expectations. Real yields remained broadly stable, supporting USD resilience and limiting upside momentum across metals and cyclical commodities.

Growth signals softened through weaker Retail Sales momentum, creating divergence between defensive flows and cyclical positioning. Oil corrected primarily through demand repricing and positioning adjustments rather than physical deterioration, while copper remained more resilient through structural supply constraints.

Policy transmission remained relatively contained after the Fed Chair nomination vote passed without market disruption. Cross-asset alignment remains incomplete, with inflation pressure still dominating while growth confirmation continues weakening beneath the surface.

1. Macro shock layer

A. Inflation shock

What moved

US CPI remained broadly in line with expectations, while Core PPI and headline PPI accelerated sharply above consensus.

- CPI y/y: 3.8% vs 3.7% expected

- Core PPI m/m: 1.0% vs 0.3% expected

- PPI m/m: 1.4% vs 0.5% expected

Why it matters

The inflation layer shifted from consumer stabilization toward renewed upstream pricing pressure. Markets interpreted the move as a signal that disinflation remains incomplete across the production chain.

Transmission Path

- USD stabilized through firmer inflation expectations

- Real yields remained firm but relatively contained

- Gold lost part of its upside momentum

- Commodities faced renewed pricing pressure

FX Transmission

DXY stabilized after previous downside pressure, while inflation-sensitive FX pairs saw reduced directional conviction. EURUSD lost momentum while commodity-linked currencies became more selective.

B. Growth shock

What moved

US Retail Sales slowed materially from previous readings, while UK GDP surprised positively.

- Retail Sales m/m: 0.5%

- Previous: 1.6%

- UK GDP m/m: 0.3% vs -0.1% expected

Why it matters

Consumption momentum showed signs of moderation despite stable inflation conditions. Markets began reassessing the strength of demand transmission into cyclical assets and industrial commodities.

Transmission path

- Oil weakened on softer demand expectations.

- Copper faced pressure from weaker cyclical momentum.

- Defensive positioning supported gold.

- Rates volatility remained subdued.

FX transmission

AUD and CAD lost relative momentum against the USD, while GBP outperformed through stronger domestic growth data.

C. Policy shock

What moved

The Fed Chair nomination vote passed without disruption, reinforcing continuity expectations around monetary policy communication.

Why it matters

Markets interpreted the outcome as a stabilization event rather than a catalyst for aggressive repricing.

Transmission Path

- Front-end rate expectations stabilized

- USD retained relative support

- Gold volatility compressed modestly

- Copper remained broadly neutral to policy transmission

FX transmission

Carry positioning remained relatively stable while major FX pairs traded inside tighter macro ranges.

2. Cross-asset transmission grid – 2026-W20

3. Market alignment check

Cross-asset alignment remained only partial during the week.

Stable real yields and resilient USD pricing limited upside momentum across metals, while oil failed to confirm the broader inflation narrative as demand expectations weakened through softer consumption data.

Copper remained relatively resilient despite weaker cyclical signals, reflecting the continued importance of structural supply constraints inside the industrial metals complex.

The macro chain currently shows stronger inflation transmission than growth confirmation.

4. Forward pressure points

USD

Pressure remains concentrated around real yield stability and inflation repricing sensitivity.

Gold

Gold remains highly sensitive to breakeven dynamics and USD resilience.

Oil

Demand expectations remain fragile as positioning reacts more aggressively than physical fundamentals.

Copper

Supply constraints continue balancing weaker cyclical momentum across industrial metals.

Rates

Rate volatility remains compressed despite stronger upstream inflation pressure, increasing medium-term repricing sensitivity.

One-line takeaway

The macro transmission chain remains incomplete, with inflation pressure still dominating while growth signals continue weakening across cross-asset positioning.

Author

Luca Mattei

LM Trading & Development

Luca Mattei is a market analyst focusing on FX, metals, and macroeconomic trends. He develops trading tools for retail and professional traders, coding indicators and EAs for MT4/MT5 and strategies in Pine Script for TradingView.