Global inflation: What this week’s data will reveal

As the world continues to digest the economic shockwaves from the conflict in the Middle East, and how the situation will unfold, a wave of inflation reports from major economies lands this week. Here is what investors and policymakers are watching.

Canada

After a notable drop to 1.8% in February from 2.3% the prior month — partly explained by base effects tied to the expiry of temporary tax relief in early 2025 — Canadian inflation is expected to rebound sharply in March. TD Securities forecasts headline CPI will accelerate to around 2.5%, driven primarily by the surge in gasoline prices following the outbreak of hostilities in the Middle East.

The key question for markets is how much of that energy shock bleeds into core prices. TD Securities strategist Robert Both argued that spillover into core CPI is likely to remain limited, making it unlikely to force a shift in the Bank of Canada’s tone.

Bank of Canada Governor Tiff Macklem acknowledged on Friday that March inflation almost certainly picked up, though he expects it to stay below 3%. He stressed the central bank faces a delicate balancing act: moving too soon on rates risks weighing on an already fragile economy, while moving too late risks allowing inflation to become entrenched. "You don’t want to be late and let inflation get a hold and become entrenched," Macklem told reporters.

Statistics Canada releases the March CPI reading on Monday, shortly after which the Bank of Canada will publish its quarterly survey of business and household sentiment, the first window into whether inflation expectations are drifting higher. The Bank of Canada’s next rate decision follows on April 29, with officials paying close attention to the frequency and scale of price increases being passed through by businesses.

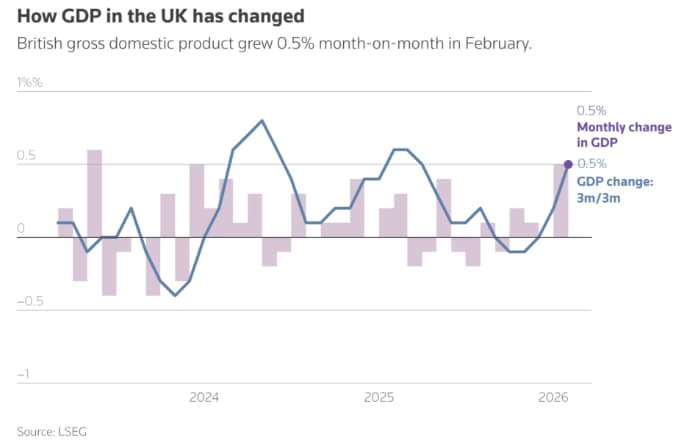

United Kingdom

Heading into the conflict, the British economy was performing better than many had feared. GDP expanded 0.5% month-on-month in February — the strongest gain since January 2024 and well ahead of the 0.2% that economists polled by Reuters had pencilled in. Yet despite that resilience, the UK remains particularly exposed to the fallout from the Middle East war, given its heavy reliance on imported energy. The IMF delivered the steepest downward revision to growth forecasts among large advanced economies to the UK, citing the Iran conflict as a primary driver.

On the inflation front, the annual rate held steady at 3.0% in February, in line with January’s reading, according to the Office for National Statistics. Food inflation, while still elevated, eased to 3.4% year-on-year in March according to British Retail Consortium data. However, the UK Food and Drink Federation has warned that food price pressures could intensify significantly, with inflation in that category potentially reaching 9% to 10% by the end of the year, as energy cost increases and supply chain disruptions in the Strait of Hormuz feed through the system.

Chief Economist Huw Pill from the Bank of England said on Friday that returning inflation to the 2% target must remain the central bank’s primary focus, even as growth risks mount. "The primacy of keeping inflation towards target and keeping it there needs to be emphasised," Pill said. Governor Andrew Bailey, speaking earlier this month, struck a somewhat broader note, emphasising that the Bank cannot afford to ignore the risks to growth and employment when calibrating its next move on rates.

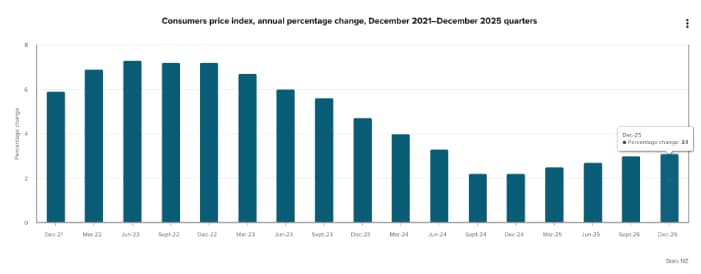

New Zealand

New Zealand entered the Middle East crisis in a fragile state. Annual inflation ticked up to 3.1% in the December 2025 quarter — the highest level since mid-2024 — against a backdrop of sluggish growth, high spare capacity and elevated unemployment, conditions that would typically dampen inflationary pressures.

The Reserve Bank of New Zealand held its benchmark rate at 2.25% at its last meeting, but the discussion has clearly shifted. Governor Anna Breman signalled that the central bank is prepared to raise rates forcefully if the conflict drives sustained inflation, and official commentary made clear that developments in the Middle East had materially altered both the inflation outlook and the balance of risks. The RBNZ’s dilemma is acute: the country was only just beginning to emerge from years of economic underperformance — a hangover partly attributed to aggressive post-pandemic rate hikes — when the crisis erupted.

Finance Minister Nicola Willis added to the cautionary tone at the end of March, warning that inflation could rise "much higher" this year and remain outside the central bank’s target band if the conflict proves prolonged. The latest Treasury modelling, she said, points to inflation peaking at a higher level than previously expected under a scenario involving an extended conflict and deeper supply chain disruption.

Japan

Japan presents perhaps the most nuanced picture among the four. Core consumer inflation came in at 1.6% in February, slipping below the Bank of Japan’s 2% target for the first time since March 2022. At face value, that gave the BOJ more breathing room before its next move. Yet the Iran war has complicated that calculus considerably, given Japan’s deep dependence on imported energy.

Markets are struggling to read the central bank ahead of its April 27–28 policy meeting. Bank of Japan Governor Kazuo Ueda declined after last week’s IMF meetings to commit explicitly to an April rate increase, but left the door open while emphasising the need to monitor how the Middle East situation evolves. A Reuters poll found that nearly two-thirds of economists still expect the BOJ to raise its benchmark rate to 1.00% by end-June, with an April or June move seen as roughly equally probable.

With Japan’s policy rate at 0.75% still below the estimated neutral rate and inflation having stayed above target for most of the past four years, the BOJ risks allowing the economy to overheat if it keeps real borrowing costs deeply negative. The conflict has solidified a hawkish stance by intensifying concerns over energy-linked inflation and a further depreciation of the yen. A Reuters poll found that 62% of economists expect the Iran conflict to push Japan’s core CPI higher by between 0.2 and 0.4 percentage points on a cumulative basis over the next year, with median forecasts for core inflation revised upward across every quarter through mid-2026.

Stay up to date with what's moving and shaking on the world's markets and never miss another important headline again! Check ActivTrades daily news and analyses here.

Author

Carolane de Palmas

ActivTrades

Carolane graduated with a Masters in Corporate Finance & Financial Markets and got the AMF Certification (Financial Markets Regulator in France). Afterward, she became an independent trader, investing mostly in European and American stocks/indices.