GDPNow forecast rises to 2.7 percent annualized despite weak economic data

Much unexpected in this corner, the GDPNow forecast for third-quarter GDP rise today.

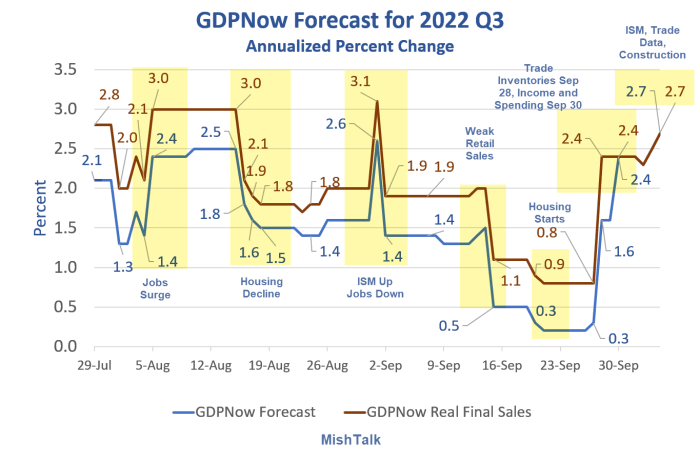

GDPNow data from Atlanta Fed, Chart by Mish

I was pretty sure a miserable constriction spending would weigh on today's GDPNow report, but nope. The forecast rose a bit with half of it on what I consider to be a very questionable ISM report.

Please consider the latest GDPNow Forecast for the third quarter of 2022, emphasis mine.

The GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the third quarter of 2022 is 2.7 percent on October 5, up from 2.3 percent on October 3. After recent releases from the US Census Bureau, the US Bureau of Economic Analysis, and the Institute for Supply Management, the nowcasts of third-quarter real personal consumption expenditures growth and third-quarter real gross private domestic investment growth increased from 0.7 percent and -4.1 percent, respectively, to 1.1 percent and -3.6 percent, respectively, while the nowcast of the contribution of net exports to third-quarter real GDP growth increased from 2.21 percentage points to 2.24 percentage points.

Base forecast vs real final sales

The real final sales (RFS) number is the one to watch, not baseline GDP. RFS ignores changes in inventories which net to zero over time.

Both the base GDPNow forecast and the RFS forecast is currently 2.7 percent.

If this is in the ballpark toss aside recession calls.

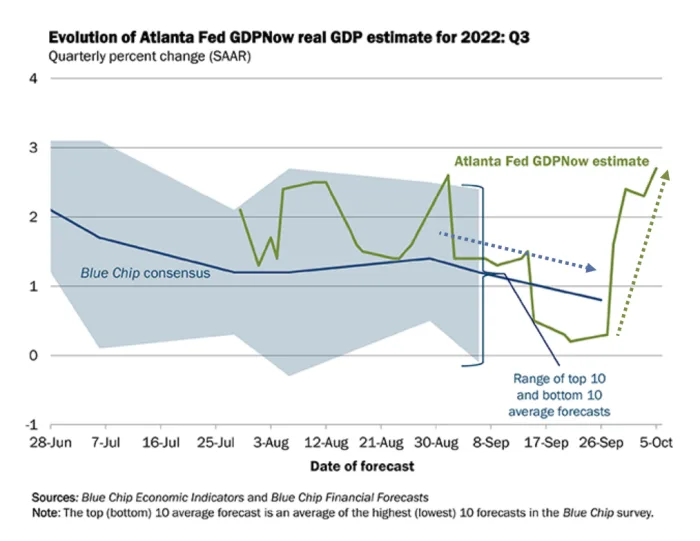

GDPNow vs blue chip forecast

Understanding the GDPNow strength

- US dollar exports account for most of the GDPNow forecast.

- Government spending accounts for all but 0.1 percentage points of the rest.

- Final sales to domestic purchasers is 0.5 percent.

- Final sales to private domestic purchasers is a mere 0.1 percent.

The Blue Chip forecast is lagging a bit timewise, but not that much. It will be interesting to watch this divergence over the next month.

For discussion of ISM services, please see ISM Services Remain Strong in August But Comments Tell a Different Story.

For the divergence between ISM and the S&P please see ISM Services Remain Strong in August But Comments Tell a Different Story.

Conflicting data is more than a bit confusing. Has the GDPNow model gone haywire?

Author

Mike “Mish” Shedlock's

Sitka Pacific Capital Management,Llc