From lows to lows: The Indian Rupee’s downward spiral has no end in sight

The Indian Rupee is slipping deeper into uncharted territory, hitting a fresh record low against the US Dollar and keeping the dubious title of Asia's worst-performing currency. With the Iran war raging on and Oil prices increasing, the Rupee’s downward spiral isn’t expected to subside anytime soon.

A weak INR acts as a double-edged sword. It causes significant inflationary pressure through expensive imports – particularly Crude Oil prices – and provides only limited advantages to exporters. This is troublesome for India, which is among the economies most sensitive to rising Oil prices.

Stagflation fears creep in

India is extremely sensitive to Oil prices as it imports over 80% of its energy consumption needs. Crude Oil prices have been rising due to the escalating Middle East war. As a result, the cost of importing goods becomes more expensive, leading to imported inflation across the economy.

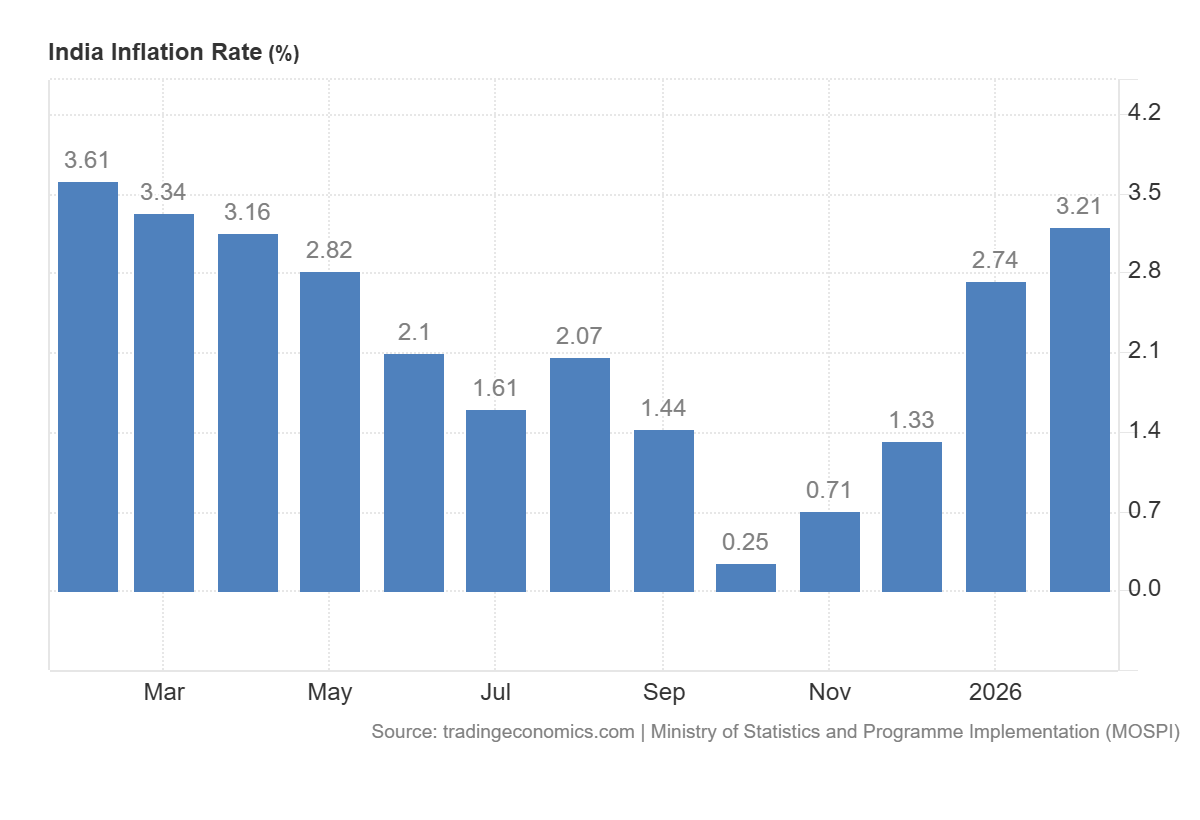

Inflation in India, currently at around 3.2%, is well within the Reserve Bank of India’s band of between 2% to 6%. But price growth has been accelerating for four months in a row, and it is reasonable to expect that it will continue to do so in the next few months unless the situation in the Middle East changes dramatically – a scenario that looks unlikely for now.

A rise in energy prices inflates domestic input costs, causing businesses to hike prices. This, in turn, reduces aggregate consumer demand and could lead to a condition that most economists fear: stagflation – a combination of high inflation and slower growth.

A widening current account deficit and higher financial burden for firms

Given India's heavy reliance on energy imports, the war in West Asia is widening its current account deficit as elevated Oil prices increase the country's import bill. Higher Oil prices increase demand for US dollars to repay these imports, further weighing on the INR.

-1773829552667-1773829552669.png)

Moreover, the INR weakness significantly increases the financial burden on Indian companies with unhedged USD-denominated debt, which could further dampen foreign investors' confidence. This could prompt capital outflow, which, in turn, might trigger a domino effect and continue to put intense downward pressure on the INR.

In this scenario, the Indian Rupee is expected to continue to weaken to 95.00 against the US Dollar over the next year, according to Santanu Sengupta, Goldman Sachs Group chief economist for India. In an interview with Bloomberg, Sengupta said that if higher Oil prices and a weaker Rupee filter through to consumer prices, the Reserve Bank of India will need to tighten. “That question will come up further down the line rather than now,” he said.

Such a move by the central bank could slow India’s healthy pace of economic growth. For now, the RBI has already stepped in to slow the pace of the Rupee’s depreciation, partly cushioning the slide, but its moves haven’t been able to reverse the broad downtrend.

Does a weak INR really benefit exporters?

The INR downfall could act as a tailwind for exporters as it makes Indian goods cheaper globally. Still, that provides little help amid a harmful backdrop: a lot of Indian exporters depend on raw materials imported from abroad, and a weak currency only benefits export-based nations.

If high inflation finally forces the Reserve Bank of India to raise interest rates, this would increase the cost of credit for exporters, making it expensive to produce goods and reducing their competitiveness.

Unless Oil prices retreat, the forces driving the Rupee’s decline are unlikely to reverse anytime soon. With external imbalances widening and inflation risks building, the currency’s slide risks feeding on itself, turning weakness into a prolonged downward cycle.

USD/INR Technical Analysis: Weakness set to continue

-1773829651482-1773829651483.png)

The strong move up for the USD/INR pair since the July 2025 low has been along an ascending channel, which points to a well-established uptrend.

The Moving Average Convergence Divergence (MACD) line stands above its signal and in positive territory, though the histogram has started to contract, hinting at moderating upside momentum rather than a reversal. The Relative Strength Index near 70 remains in overbought territory, signaling stretched conditions as the pair approaches the channel ceiling, which could slow the advance.

This makes it prudent to wait for a sustained breakout through the trend-channel hurdle before placing fresh bullish bets around the USD/INR pair. This would open the way toward fresh highs within the bullish structure.

On the downside, initial support aligns with the lower bound of recent consolidation and the channel’s lower band near 91.18, with a daily close below this level undermining the current bullish bias and exposing deeper retracement toward prior lower closes. As long as price holds above 91.18, dips are likely to be treated as corrections within the prevailing upward channel.

(The technical analysis of this story was written with the help of an AI tool.)

Author

Haresh Menghani

FXStreet

Haresh Menghani is a detail-oriented professional with 10+ years of extensive experience in analysing the global financial markets.

![How Wall Street rigs the game [Video]](https://editorial.fxsstatic.com/images/i/market-chaos-01.jpg)