Five fundamentals for the week: Fed, ECB and US GDP try to compete with Trump

- Donald Trump will continue rocking markets in his second week in office.

- January ends with a blast, featuring decisions from major central banks.

- US GDP and Core PCE will provide data points for investors to chew on.

The gift that keeps on giving – United States (US) President Donald Trump continues to be "generous" with market volatility, but this week, he'll face competition from the Federal Reserve (Fed). A rate decision in the Eurozone, the first release of US Gross Domestic Product (GDP) for the entire 2024, and the Fed's favorite inflation gauge will all rock markets. Fasten your seatbelts..

1) Trump tariff tantrums will continue shaking markets

The 47th President has unfettered access to the media, which makes every comment on tariffs a major market mover. Refraining from immediate action and mentioning only a 10% levy on Chinese goods boosted sentiment last week – but talking about slapping Canada and Mexico with 25% tariffs hurt them. His threats on Colombia on Sunday also ruffled investors' feathers.

Trump's tariff comments will continue dominating headlines, with calmer tones supporting Stocks, while worrisome ones buoying the US Dollar (USD). Gold moves with Stocks in response to tariff talks, but has a less straightforward path.

I expect President Trump to refrain from wild action because he deeply cares about the valuations of equities. Markets can respond with a tantrum of their own to any nasty comments by Trump, and that is a deterrent.

Trump may also influence markets through immigration policy. Investors do not care about newcomers, but deporting people working in America may hurt the economy. Also here, I expect measured action.

2) Fed may hit markets with another hawkish hammer

Wednesday, 19:00 GMT, press conference at 19:30 GMT. The Federal Reserve is set to keep interest rates unchanged at its first meeting of 2025. Officials conveyed that message repeatedly, and it is fully priced in. Markets will move in response to the central bank's tone on future moves.

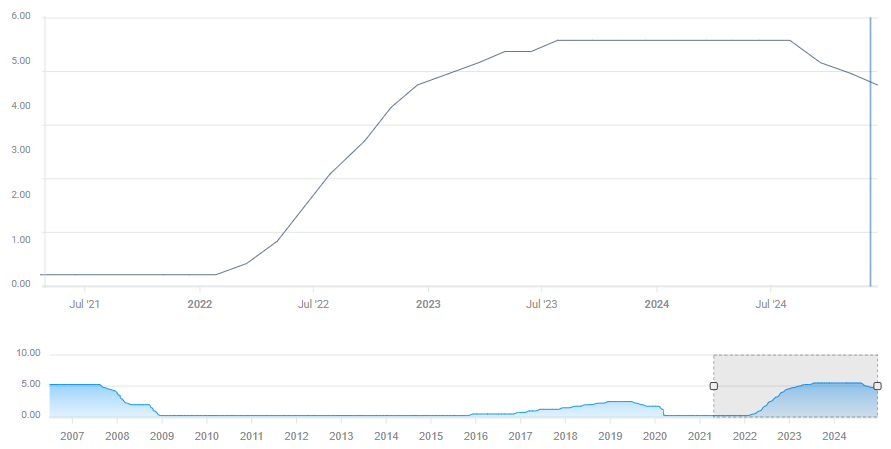

US internet rates. Source: FXStreet

Back in December, the world's most important central bank slashed borrowing costs by 25 basis points (bps), but accompanied it with a starkly hawkish message. The Fed's forecasts for interest rates in the Summary of Economic Projections (SEP) – aka "dot plot" – pointed to only two cuts in 2025. That was half the projections in September.

Moreover, Fed Chair Jerome Powell seemed confident about the US economy and the labor market while worrying about inflation raising its head once again. Perhaps the most striking part was his comment related to the incoming administration. Powell said members took Trump's potential policies into account – hinting the Fed forecasts higher inflation due to President Trump's policies.

Since then, the December Nonfarm Payrolls (NFP) report pointed to a sizzling hot labor market. However, Consumer Price Index (CPI) inflation marginally missed estimates, allowing bond markets to remain hopeful for two cuts in 2025.

At their January meeting, officials do not publish new forecasts, but their carefully crafted words will still rock markets. Powell may try conveying a message of "nothing to see here, move along" – but that never works.

The path of least resistance is to the hawkish side. Why? Markets are now less worried that the Fed will refrain from any rate cut in 2025 and still expect two moves. Repeating the hawkish tone would cause a rethink – with fresh expectations of only one cut.

If my prediction is correct, Gold and Stocks will tumble, while the US Dollar would jump.

What is the opposite scenario? If Powell says that the assumptions in the dot plot are still intact – meaning two cuts in 2025 – markets would cheer and the US Dollar would fall.

All in all, the key is to change the expectations for interest rate cuts later this year.

3) ECB set to cut rates, hope for no damage from tariffs

Thursday, decision at 13:15 GMT, press conference at 13:45 GMT. Inflation has dramatically fallen in the Eurozone, justifying another rate cut. Similar to the Fed, officials at the European Central Bank (ECB) have been conveying this message, so a 25 bps reduction in borrowing costs is fully priced in.

The questions for markets are: why cut, and what's next?

If the Frankfurt-based institution merely adjusts interest rates to falling inflation, it is a positive sign for the 20-strong currency union, which can enjoy looser conditions.

However, if the main motivation for cutting rates is a weaker economy or fear of US tariffs, the Euro would suffer. ECB President Christine Lagarde will surely be asked about potential tariffs from Trump, who laments about America's trade deficit with the EU and sees antitrust action from Brussels as hostile to his country.

While Lagarde may refrain from directly engaging in politics, tariffs have an impact on the economy and monetary policy. I expect Lagarde to be optimistic, thus supporting the Euro.

And, what's next? After a series of interest rate cuts, the ECB may take a pause in March. While it is unlikely to commit to any specific move – the central bank is "data-dependent" and decides on a "meeting-by-meeting" basis – that may be the tone. The bank has a good reason to refrain from commitment: its staff publishes new forecasts in the March meeting, and it could lean on those projections to make a decision.

Another reason to expect a hint of a pause next time – a move that would boost the Euro – is to give the hawks at the Governing Council something. The doves have outnumbered them in recent months, and consensus-building is part of the European game.

4) US GDP set to show a strong economy

Thursday, 13:30 GMT. Sandwiched between the two parts of the ECB decision, investors will get the first look at the preliminary US Gross Domestic Product (GDP) figures for the fourth quarter of 2024. As it is the last quarter, it will be a chance to look at overall American expansion in the year that just ended.

This is an opportunity to remember that US growth is exceptional, the driver of a robust stock market and a rising US Dollar.

The economic calendar points to an annualized growth rate of 2.8% in Q4, down from 3.1% in the prior quarter. That would still exceed most developed-world peers, with Spain being the only exception.

Any figure above 3% would further support the Greenback and weigh on Gold and Stocks – which prefer softer data and lower interest rates.

On the contrary, a drop toward 2.5% would be disappointing for the economy, but would boost Gold and Stocks. I expect an upbeat figure of around 3%.

5) Core PCE to test Fed inflation assumptions

Friday, 13:30 GMT. Last but not least, the Fed's preferred measure of inflation. The Personal Consumption Expenditure (PCE) report uses a different methodology for calculating changes in prices, which is more attuned to changes in consumer activity. It adapts to changes, which makes it more trustworthy for the central bank, despite its publication after the parallel Consumer Price Index (CPI) report.

The Fed aims to have core PCE – which excludes volatile energy and food – at 2%. After falling quickly from the peak, the "last mile" of declines is frustratingly slow, and core PCE even rose in the second half of 2024.

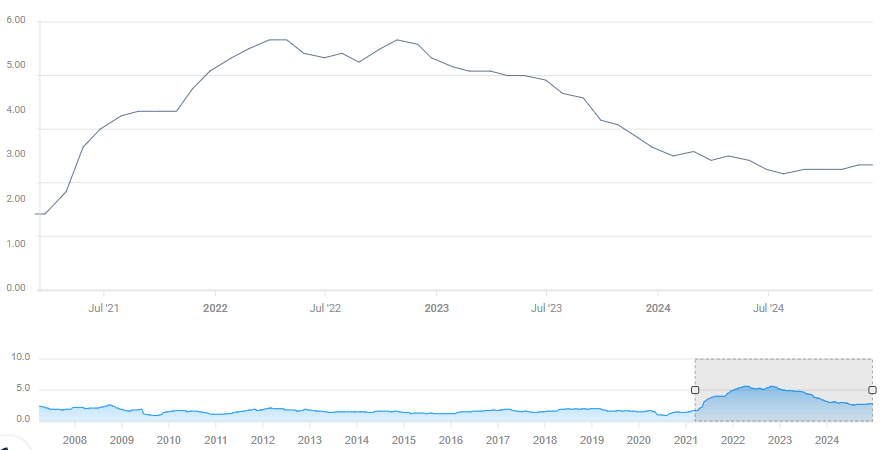

US Core PCE. Source: FXStreet

The economic calendar points to another read of 2.8% year-over-year (YoY) in December, a repeat of November. Any 0.1% difference matters. A drop would send Gold and Stocks up, while another increase would keep the US Dollar bid.

The release would have a greater impact if it contrasts with what the Fed signaled. For example, if Powell seemed calm on inflation and it rose, markets would be more alarmed. In case the Fed is worried about rising prices and they fall, investors would breathe a collective sigh of relief.

Final Thoughts

Headlines from the White House can land anytime, which means high uncertainty and whipsaws. Trade with care.

Author

Yohay Elam

FXStreet

Yohay is in Forex since 2008 when he founded Forex Crunch, a blog crafted in his free time that turned into a fully-fledged currency website later sold to Finixio.