Fed September Preview: Terminal rate projection is key

- Fed will announce its monetary policy decisions on Wednesday, September 21.

- US central bank is widely expected to raise its policy rate by 75 bps.

- Investors will pay close attention to terminal rate projection in dot plot.

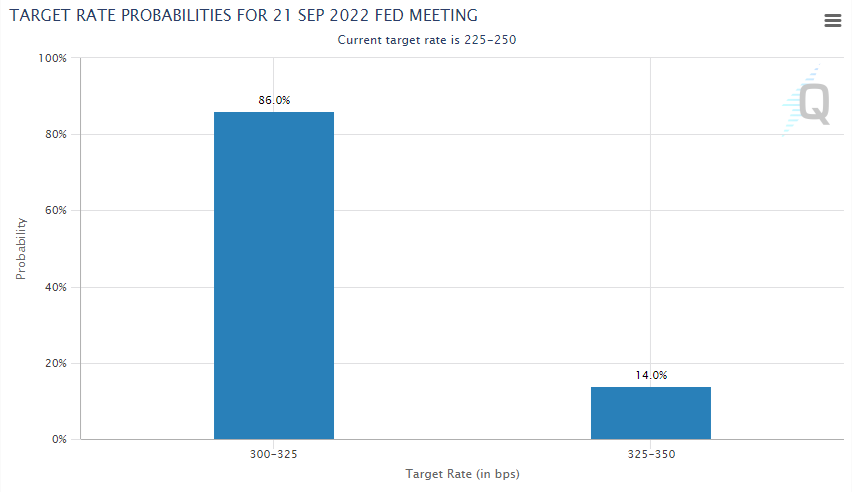

The US Federal Reserve is widely expected to hike its policy rate by 75 basis points (bps) to a range of between 3%-3.25% on Wednesday, September 21. The market positioning following the upbeat employment and stronger-than-expected Consumer Price Index (CPI) figures for August, however, suggests that there is a 14% probability of a 100 bps increase. The Fed will also release its updated Summary of Economic Projections (SEP), the so-called dot plot, alongside its policy statement.

Source: CME Group

The US Dollar Index (DXY), which tracks the greenback’s performance against a basket of six major currencies, has gained over 4% since mid-August and touched its highest level in nearly two decades at 110.78 on September 7 before going into a consolidation phase.

Since July’s 75 bps hike, FOMC policymakers reiterated that they will make policy decisions on a meeting-by-meeting basis and reaffirmed their commitment to battle inflation. While speaking at the Jackson Hole Symposium on August 25, FOMC Chairman Jerome Powell noted that the restrictive policy will remain in place for ‘some time’ for them to be able to restore price stability. “These are the unfortunate costs of reducing inflation but failing to restore price stability would mean far greater pain,” Powell said, reminding markets that they will prioritize taming inflation even if their actions were to weigh on economic activity.

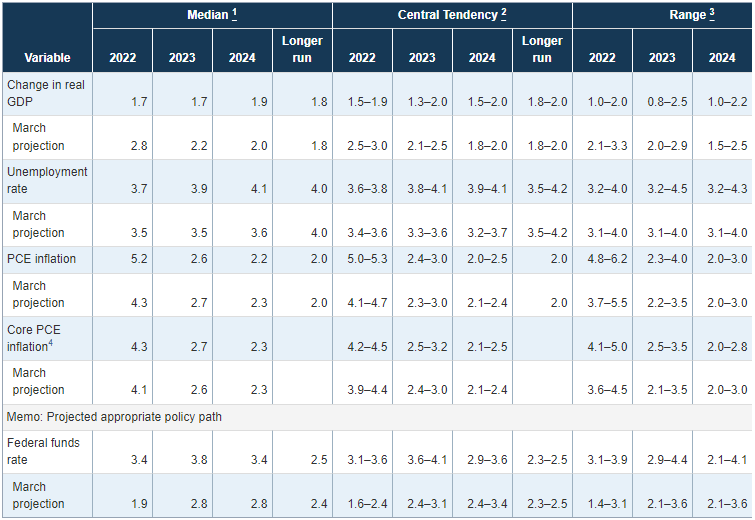

June Summary of Economic Projections

Source: US Federal Reserve

Neutral scenario

In case the Fed raises the policy rate by 75 bps as expected, the dot plot will be scrutinized by investors for fresh clues regarding the policy outlook. June’s SEP showed that the terminal rate in 2023 was expected to be 3.8%. Given the worsening inflation outlook and July’s 75 bps hike, it wouldn’t be surprising to see a much higher estimate for the terminal rate. If the publication reveals that the policy rate is forecast to peak somewhere between 4.5% and 5% next year before starting to decline in 2024, that would suggest that the Fed is likely to continue to frontload rate hikes early next year and stay on hold rather than looking to ease the policy prematurely. In the neutral scenario, the dot plot is likely to reveal a downward revision to the Gross Domestic Product growth for 2022, which stood at 1.7% in June’s projection. Unless the Fed outright forecasts a recession, however, that would signal that the US central bank should be able to stay on its tightening path.

Dovish scenario

A 50 bps rate hike, which is extremely unlikely at this point, would be a significant dovish surprise and trigger a long-lasting dollar sell-off. If the Fed opts for a 75 bps hike as expected, a terminal rate forecast below 4.5% could also force the greenback to lose strength against its rivals. An optimistic inflation outlook combined with a recession forecast in 2023 could cause investors to start pricing in a policy shift in the second half of next year.

Hawkish scenario

Clearly, a 100 bps hike would be a hawkish outcome and fuel another dollar rally in the short term. A terminal rate at or above 5% in 2023 alongside a 75 bps increase in September would also offer an even more aggressive Fed rate hike path than what markets are currently expecting. A significant upward revision to the 2023 PCE inflation forecast with an unchanged growth expectation for the same could also provide a boost to the dollar.

Summary

Since the most probable outcome of the September FOMC policy meeting is a 75 bps rate hike, the location of the projected terminal rate is likely to drive the market reaction. Around mid-July, markets were optimistic that the Fed could take a dovish turn in the second half of 2023 and the DXY moved in a downtrend for a few weeks until mid-August. With FOMC policymakers arguing that the markets were getting ahead of themselves by expecting rate cuts next year, the selling pressure surrounding the greenback abated. Strong labor market data and dissipating hopes of inflation having peaked this summer reassured markets that the US central bank has no other option than frontloading rate hikes. The DXY rally that started in mid-August suggests that a 75 bps hike with a terminal rate of between 4.5% and 5% next year, as noted in the neutral scenario, is largely priced in. Hence, the dollar could weaken in the short-term amid a ‘buy the rumor sell the fact’ market action. Nevertheless, it will be only a matter of time before investors fail to find a better alternative than the USD in the current market environment, especially when considering the widening policy divergence between the Fed and other major central banks.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Eren Sengezer

FXStreet

As an economist at heart, Eren Sengezer specializes in the assessment of the short-term and long-term impacts of macroeconomic data, central bank policies and political developments on financial assets.