European and US futures waver as earnings jitters and tariff fears shape market mood

Where are markets today?

European and U.S. stock futures are mixed this morning, with slight weakness prevailing across key benchmarks. Futures for the DAX, CAC 40, and FTSE 100 are hesitating after five straight winning sessions for Europe, while U.S. indices like the S&P 500 and Nasdaq 100 are pointing toward a softer open. This cautious mood is fueled by growing investor anxiety over the broader impact of proposed U.S. tariffs, which threaten to reignite global trade tensions at a fragile economic moment. A heavy week of earnings releases also keeps sentiment in check, as traders weigh corporate resilience against these emerging external risks.

Firstly, fears around U.S. tariff policies under Trump’s influence are casting a long shadow. While the Stoxx 600 recovered impressively year-to-date, the resurgence of protectionist rhetoric could easily choke the rebound, making investors reluctant to push markets higher without clearer direction. Tariffs introduce cost pressures across supply chains, which earnings season is now beginning to reveal, especially for companies heavily reliant on international trade.

Secondly, despite stronger-than-expected Q1 corporate earnings in some sectors, the tone of company guidance has turned more cautious, reflecting uncertainties around future consumer demand and input costs. In the U.S., today’s economic data deluge—particularly the CB Consumer Confidence and JOLTS job openings—poses a wild card, said Aaron Hill, the Chief Analyst at FP Markets . Any sign of weakening confidence or labor market softening could reinforce fears that the economy is more vulnerable than equity markets have priced in. With Europe’s industrial-heavy indices and America's tech-led benchmarks both sensitive to growth trends, futures are showing the strain of investors trying to balance hope with hard realities.

Major indexes snapshot

S&P 500: Closed at 5,611.85, marking a 0.06% increase.

Dow Jones Industrial Average: Ended at 40,227.59, up by 0.28%.

Nasdaq Composite: Finished at 17,366.13, experiencing a slight decline of 0.03%.

Russell 2000: Closed at 2,135.00, reflecting a modest gain.

Drivers behind the market move

As of Tuesday, April 29, 2025, European and U.S. markets are displaying a cautious stance, with futures indicating a mixed opening. This reflects investor apprehension stemming from recent geopolitical developments and upcoming economic data releases.

1. Geopolitical tensions and trade policies

President Trump's recent remarks suggesting potential deals with Ukraine and expressing disappointment in Russia have introduced a layer of geopolitical uncertainty. Additionally, the U.S. administration's consideration of imposing tariffs on Canada and Mexico has unsettled markets, particularly in Europe, where companies like Porsche have already adjusted their sales outlooks in anticipation of trade disruptions.

2. Anticipation of economic data releases

Investors are closely monitoring upcoming economic indicators, including the Spanish Flash CPI, S&P/Case-Shiller Home Price Index, JOLTS Job Openings, and CB Consumer Confidence data. These releases are expected to provide insights into inflation trends and labor market conditions, which are critical for assessing the economic outlook amid ongoing trade tensions.

3. Corporate earnings and market sentiment

The current earnings season is pivotal in shaping market sentiment. Companies with significant international exposure are particularly under scrutiny, as investors assess how trade policies and geopolitical developments are impacting corporate performance. The combination of earnings reports and economic data is likely to influence investor confidence and market direction in the near term.

In summary, today's market movements are influenced by a confluence of geopolitical uncertainties, anticipated economic data, and corporate earnings reports. Investors are navigating these factors cautiously, leading to a tentative market opening in both European and U.S. markets.

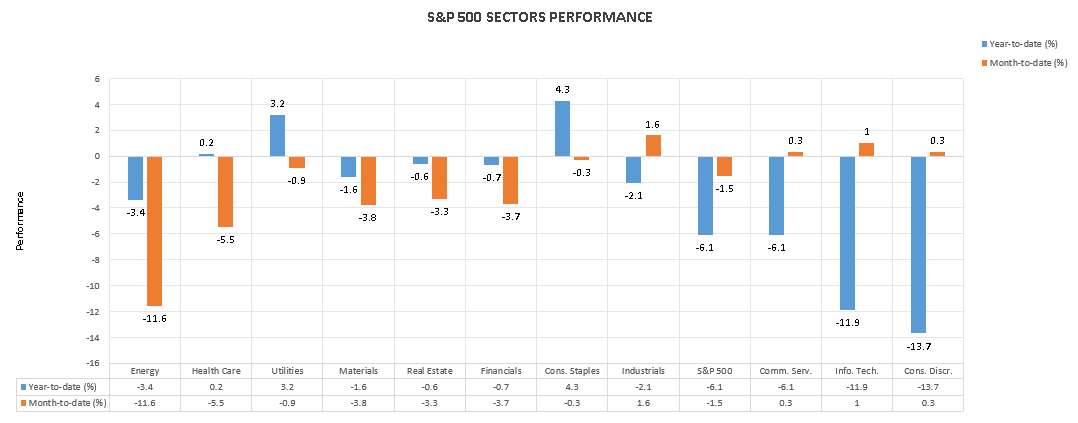

The strongest sector in all these indices

Consumer staples and utilities lead amid broader market weakness

Chart by Zaye Capital

Despite continued market volatility, select defensive sectors outperformed in 2025. Consumer Staples and Utilities stood out with positive year-to-date gains, while the broader S&P 500 struggled.

- Consumer staples:

+4.3% YTD | -0.3% MTD

Consumer Staples remained the strongest sector, with a +4.3% year-to-date increase. Month-to-date performance was slightly negative at -0.3%, but the sector’s resilience reflects ongoing investor preference for defensive exposure.

- Utilities:

+3.2% YTD | -0.9% MTD

Utilities posted a +3.2% YTD gain. Although the sector slipped -0.9% month-to-date, it continues to benefit from its defensive characteristics, attracting capital amid economic uncertainty.

- Health care:

+0.2% YTD | -5.5% MTD

Health Care managed to stay marginally positive year-to-date at +0.2%, though it suffered a significant -5.5% decline month-to-date, highlighting increased volatility within the sector.

Meanwhile, sectors like Consumer Discretionary (-13.7% YTD) and Information Technology (-11.9% YTD) remained the largest laggards, reinforcing the rotation toward safer assets.

Author

Naeem Aslam

Zaye Capital Markets

Based in London, Naeem Aslam is the co-founder of CompareBroker.io and is well-known on financial TV with regular contributions on Bloomberg, CNBC, BBC, Fox Business, France24, Sky News, Al Jazeera and many other tier-one media across the globe.