Energy shock: Dashboard 2026 vs 2022 – Eurozone special issue (June 2026 data)

Will the same causes produce the same effects? In other words, will the war in Iran and the resulting surge in oil and gas prices lead to an inflationary shock comparable to that seen in 2022? Will their negative effects on growth be the same as those of the war in Ukraine and the subsequent energy shock?

We have selected a set of indicators to track the impact of this new energy shock — caused by the war in the Middle East — on activity and prices in the Eurozone, the United States, oil and gas markets and emerging countries, and to see how much the current situation resembles that of 2022 at the outbreak of the conflict in Ukraine.

This dashboard features charts and comments that will be updated on a monthly basis for as long as necessary.

The expectation that the surge in inflation, driven by this new energy shock, would be more moderate than in 2022 (with demand being less dynamic and supply less constrained) is confirmed. However, following the Memorandum of Understanding signed in mid-June between the United States and Iran, inflationary risk has eased but has not disappeared. This MoU has reduced the risk of a severe escalation of the conflict, but the resurgence of tensions and military strikes in mid-July shows that the situation is far from resolved.

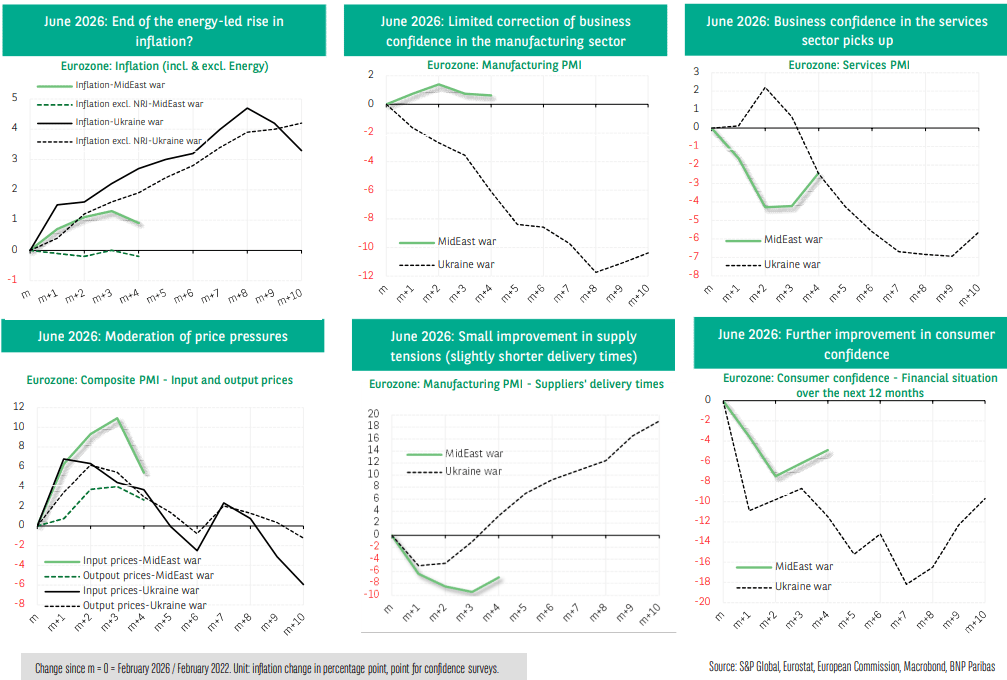

When we compare the impact on economic activity of the current energy shock with that of 2022 (following the conflict in Ukraine), the favorable point in 2026, for the euro area, is the business climate in the manufacturing sector, which is holding up better than in 2022. Consumer confidence has fallen sharply but to a lesser extent in 2026 than in 2022. As for the deterioration in the business climate in the services sector, it was immediate in 2026, whereas it occurred with a few months' delay in 2022.

Eurozone: The drop in Oil prices drives inflation in its wake, tempers inflationary pressures and supports confidence surveys

We have selected two inflation measures (with and without energy) and six survey indicators: business confidence, as measured by the PMIs in the manufacturing and services sectors; the “input prices” and “output prices” components of the composite PMI (in order to identify direct inflationary pressures); the “suppliers’ delivery times” component of the manufacturing PMI (a direct indicator of possible supply difficulties and supply-demand imbalance, and therefore, indirectly, of inflationary pressures in the making); household confidence, as reflected in its “assessment of financial situation in the next 12 months” component (in order to capture the impact of inflation on purchasing power). The trends in each of these indicators are observed relative to month m=0, corresponding to the start of the conflict. Each line does not represent the level of the indicator, but its cumulative variation compared to month m=0.

The assessment of the June data is positive and reinforces the encouraging signals from May data. Symmetrically to its rise, which was largely driven by the ”energy” component, inflation has significantly receded due to the marked drop in oil prices in June. According to PMI business climate surveys, inflationary pressures have also eased. Delivery times are also benefiting from the supportive impact of the MoU (signed in mid-June between the United States and Iran) and are improving slightly. The business climate in the manufacturing sector has slipped again but marginally. Business confidence in the services sector and consumer confidence continue to recover. The expected improvement due to the reduced risk of a severe escalation of the conflict in Iran is materializing. It remains to be seen whether it will withstand the persistence of uncertainties and the resurgence of tensions in mid-July.

Author

BNP Paribas Team

BNP Paribas

BNP Paribas Economic Research Department is a worldwide function, part of Corporate and Investment Banking, at the service of both the Bank and its customers.