Easy does it: Bank of England leaves bank rate on hold at 5.0%

‘Easy does it’ was today's primary message from the Bank of England (BoE).

Unlike the US Federal Reserve cutting rates by an outsized 50 basis points (bps) yesterday, the BoE is clearly in no rush to ease policy, with most policymakers backing a slow and steady approach.

In an 8-1 majority vote, the BoE left the Bank Rate on hold at 5.0% (external member Swati Dhingra, a known dove, opted for a 25bp cut). This follows August's meeting's 25 bp reduction, its first rate cut since 2020. The central bank also unanimously voted that the Committee would decrease its government bond purchases by £100 million over the next 12 months.

Amid the hold and hawkish vote split, the rate announcement triggered a bid in sterling (GBP) versus major G10 currencies. GBP/USD refreshed year-to-date peaks just north of US$1.33, touching levels not seen since early 2022.

BoE Governor Andrew Bailey emphasised that the economic picture is evolving as expected and rates would be reduced ‘gradually over time’, and added: ‘It's vital that inflation stays low, so we need to be careful not to cut too fast or by too much’.

Headline inflation remains just north of the BoE’s target

UK CPI inflation (Consumer Price Index) was unchanged in August for both YoY and MoM measures on the headline front. The Office for National Statistics revealed that UK headline inflation rose by +2.2% (YoY), flirting just north of the BoE’s inflation target of 2.0%, reached in May this year. Core and services inflation, however, ticked higher in August, with the latter still a thorn in the side of the BoE. It is worth noting that the rise in services inflation was largely due to base effects.

Wages continued to pull back in the three months to July; the unemployment rate also dropped to 4.1% from 4.2% in June (BoE forecast unemployment will hit 4.8% in two years), and employment growth jumped to 265,000 from June’s reading of 97,000.

Regarding growth, the BoE now forecasts real Gross Domestic Product (GDP) to ease to 0.3% in Q3 24, a touch south of the 0.4% August forecast. While the economy grew 0.5% in the three months to July 2024, albeit softer than the market’s median estimate of 0.6% and lower than June’s reading of 0.6%, real GDP flatlined again in July, defying economists’ expectations of 0.2%.

Cautious vibe

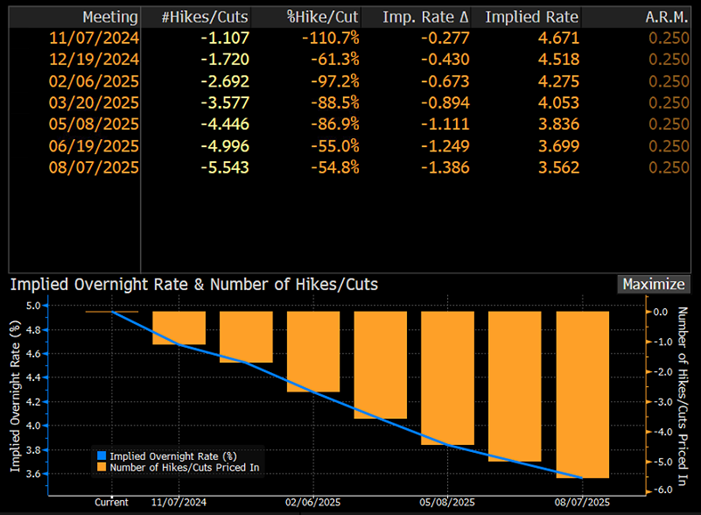

The central bank’s cautious vibe has seen markets pare rate cut bets for this year. OIS traders (Overnight Index Swaps) are fully pricing in a 25bp rate cut in November, with a total of 43bps of cuts for the year.

Where does this leave the GBP?

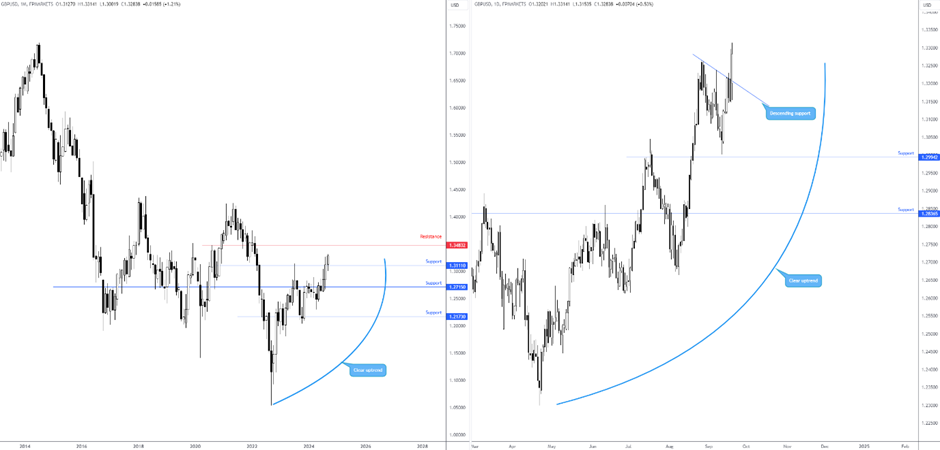

The British pound versus the US dollar (GBP/USD) is in a favourable spot on the monthly chart. Following the break of resistance at US$1.3111 (now possible support), this technically swings the pendulum in favour of further upside for the currency pair, targeting resistance at US$1.3483.

The trend also supports the bulls, exhibiting clear-cut uptrends on the monthly and daily charts, therefore any corrections will likely be viewed as dip-buying opportunities. Supports of interest are the monthly base mentioned above at US$1.3111, positioned near a local daily descending support line, extended from the high of 1.3267.

Author

Aaron Hill

FP Markets

After completing his Bachelor’s degree in English and Creative Writing in the UK, and subsequently spending a handful of years teaching English as a foreign language teacher around Asia, Aaron was introduced to financial trading,