Dumb Bellwether: Don't fret about May Retail Sales

Summary

Retail sales fell 1.3% in May. Mask mandates were lifted mid-month and what emerges is exactly what we should hope to be seeing: splurging on big-ticket items and fixing up the house is out (for now); going out to eat and reconnecting with family and friend sis in. A soft patch in retail sales is perfectly in line with our expectation for a recreation renaissance this year.

What is it good for?

The monthly retail sales figures are typically a good proxy for consumer spending more broadly, but because of the unique characteristics of this cycle and where we are in terms of returning to some semblance of normal consumer activity, it may not be the best barometer for a few months. Retail sales fell 1.3% in May,although the blow was cushioned by the fact that April figures were revised from flat to +0.9%.

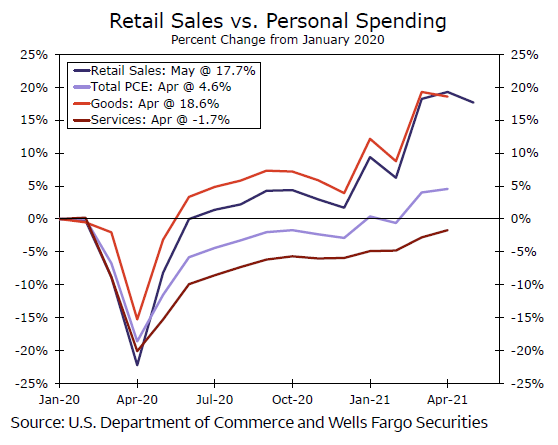

Most of the heavy lifting when it comes to consumer spending will be done on the services side and as seen in the top chart, retail sales stend to track goods spending more closely. Services do show up in some places in retail sales - spending at bars & restaurants for example shot up 1.8%. But because the report is a better reflection of goods spending, we expect it to be hit-and-miss for the next several months.

There is a story in the details of today's retail sales report for May.The days of spending money online and splurging on durable good sand home furnishings is pivoting toward getting ready for trips to see grandma and grandpa at the lake or the beach and evenings out reconnecting with friends at bars and restaurants.

What goes up...

Some of the best performing store types during the pandemic posted the largest monthly declines in May. Spending at motor vehicles & parts dealers, which represents the largest category of retail sales, slipped 3.7%. The motor vehicle category was one of the hottest areas for spending over the better part of the past 15 months. There was a sudden drop in ridership and public transit,so many rideshare drivers were without work and the federal government provided jobless benefits for those and other gig-economy workers. Demand for autos remains strong, too strong in fact. Demand is outstripping supply and some automakers have had to shut down assembly plants for want of semiconductor sand other scarce input components. We expect the supply chain constraints to act as a governor on the pace of auto sales for the foreseeable future.

Another category that was big winner during the pandemi but has seen a softening in sales more recently is building materials &supply stores where sales dropped 5.9%, the most of any category.With nothing else to do and nowhere else to go, many homeowner sturned to the yard and garden or took on a remodeling project.While a one pastime with nothing else going on, who wants to mow the lawn when a long overdue vacation beckons?

We expect many of these retail sales categories to see on-again,off-again growth in coming months as the services side of thee cono my sees the full effect of more than a year's worth of pent-up demand.

Places to go, nothing to wear

There were a few silver linings in today's report, other than the rise in restaurant sales. After a year at home, consumers are starting to ven ture out and many of the categories that posted higher sale sin May suggest consumers first want to improve their appearance.Spending at clothing stores rose 3.0% in May, as we now have places to go but nothing to wear. This gain, however, was likely partly boosted by higher prices during the month, as last week we learned from the separately released CPI data, that consumer prices for apparel leaped 1.2% in May. Further indication of consumers gearing up for normal life was a pop in department store sales(+1.6%) and health & personal care retailers (+1.8%).

These categories of goods spending support a return to normal social activity and are encouraging signs that consumers are it ching to get out and spend. The May report for retail sales therefore does not change our expectations and actually remains supportive for a boom in Q2 consumer spending.

Author

Wells Fargo Research Team

Wells Fargo