Dovish BoC Remains a Risk Ahead of Rate Decision

Are investors getting ahead of themselves on the number of Bank of Canada rate hikes in 2018?

A small percentage of Canada ‘bears’ believe there’s a strong possibility that Governor Poloz could surprise Wednesday (10 am EDT) with a ‘dovish’ view of economy. For sure, employment data has been strong, but the NAFTA dissolution risk has not dissipated either.

There is a possibility that tomorrow’s BoC statement could emphasizes their cautious outlook, which will only drive two-year bond yields lower and cause weakness in the recent high flying loonie (C$1.2442).

Elsewhere, the ‘mighty’ USD has strengthened a tad, rebounding from its lowest close in three-years as the JPY and EUR both fell in the overnight session. Euro and Asian stocks have advanced, some to new record highs, along with government bonds, while it is a mixed picture across commodities.

1. Global equities on the rise

In Japan, the Nikkei hit its highest level since 1991 as the dollar weakening is temporary halted. The Nikkei ended +1% higher, while the broader Topix was up +0.55%.

Down-under, Australia’s S&P/ASX 200 slid -0.4%, though, with mining companies falling as metals prices lost some of the dollar-driven gains they made in yesterday’s session.

In Hong Kong, the benchmark Hang Seng Index rose to a record closing high overnight, led by index heavyweight Tencent Holdings. At close of trade, the index was up +1.81%, while the Hang Seng China Enterprises index rose +2.54%.

In China, stocks rallied on Tuesday, with the blue-chip index closing at a 30-month high, led by a surge in real estate firms, and this despite poll backing investor expectations that growth in China will slow in 2018. At the close, the Shanghai Composite index was up +0.79%, while the blue-chip CSI300 index was up +0.81%.

In Europe, regional indices are trading higher across the board, with the DAX outperforming following weakness yesterday, after higher closes in Asia and stronger indicated opens in the U.S.

Futures on the S&P 500 Index have increased +0.5% to a new record.

Indices: Stoxx600 +0.4% at 399.6, FTSE +0.2 at 7782, DAX +0.8% at 13302, CAC-40 +0.4% at 5531, IBEX-35 +0.6% at 10530, FTSE MIB +0.6% at 23690, SMI +0.2% at 9560, S&P 500 Futures +0.5%.

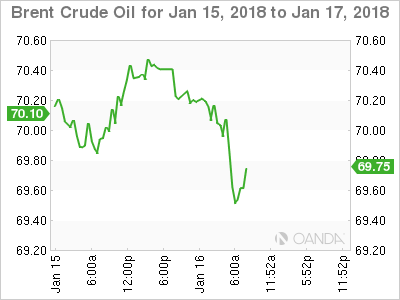

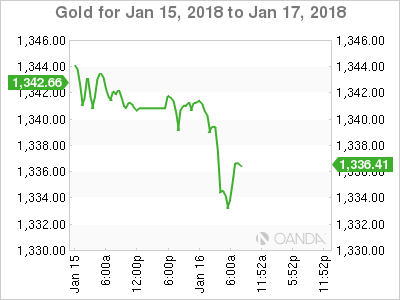

2. Oil prices near three-year highs, gold lower

Crude oil prices have dipped a tad ahead of the U.S open, but remain near their three-year highs.

Oil production curbs in OPEC nations and Russia, as well as strong demand thanks to healthy economic growth have driven up recent prices.

Brent crude futures fell -54c, or -0.77%, to +$69.72 per barrel. Brent hit +$70.37 yesterday, a high from December 2014, when markets were at the beginning of a three-year decline.

U.S West Texas Intermediate (WTI) crude futures are at +$64.18 a barrel, down -12c, or -0.19%. WTI hit a December 2014 peak of +$64.89 a barrel in earlier trading.

Growing signs of a tightening market has boosted confidence among traders and analysts that prices can be sustained near current levels. Other factors, including political risk, have also supported crude.

Gold prices have eased from their four-month peak as the ‘big’ dollar fights back. Spot gold is down -0.1% at +$1,341.28 an ounce, after touching its strongest since Sept. 8 at +$1,344.44 the session before.

3. Euro QE premiums fading lifts Bund yield

Are forward Eonia (Euro overnight index average) rates reflecting a too aggressive path of interest rate hikes by the European Central Bank (ECB)? Currently, the Eonia curve reflects a +70% probability of a +10 bps rise in the deposit rate in December 2018. It also has fully priced in a +15 bps rise in Q1, 2019 and expects an additional +10 bps rise in Q3, 2019. If the ECB ends its net asset purchases in September 2018, and assuming that “well past the horizon of the net asset purchases” means six-months later, the first rate rise would not follow until March 2019.

Many expect the 10-year German Bund yield to rise to +1.0% by the end of 2018, as it gradually removes the embedded premium related to the ECB’s quantitative easing (QE) program.

Overnight, Germany’s 10-year yield sank -2 bps to +0.57%. The yield on 10-year U.S notes fell -1 bps to +2.53%, the lowest in more than a week, while in the U.K, the 10-year Gilt yield decreased -2 bps to +1.305%, the largest pullback in a fortnight.

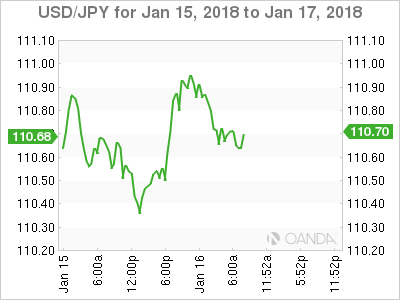

4. Dollar finds a toehold

The U.S dollar’s weakness is trying to find a reprieve in early January trading. The greenback’s global supremacy is being challenged by the Chinese yuan as the pricing medium for energy and other commodities, while domestically; the USD is also facing political headwinds as U.S GOP leaders face their most difficult government shutdown deadline to date.

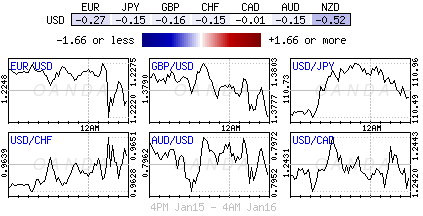

Overnight, the EUR/USD (€1.2231) has retraced from recent three year high just under the €1.23 area. The German SPD party is showing divide on alliance with Merkel – Germany Berlin SPD chapter is said to reject coalition talks with Merkel bloc citing results of the exploratory talks.

Note: The recent EUR rise seems to have been accepted by the ECB. Hansson’s comments that “Euro appreciation no threat to inflation outlook” came just as the market had pushed the currency to the highest level since the ECB began its QE.

GBP/USD (£1.3755) consolidated in the session after testing above 1.38 on Monday following reports late last week that Netherlands and Spain were open to a deal for Britain to remain as close as possible to the trading bloc. Intraday focus was on last months U.K inflation data (see below).

Elsewhere, the yen (¥110.72) has temporarily halted its five-day increase amid a warning from Japan’s finance minister about excessively rapid moves in the currency market.

Bitcoin (BTC) has slumped again, down -16% to +$12,255, the lowest level since Dec. 5 as China escalates its crackdown on crypto trading.

Note: BTC earlier was down by more than -40% percent from its record high in mid-December. Rival cryptocurrencies has also tumbled, with Ripple diving as much as -28%.

5. U.K inflation eased in December, but topped BoE target

Data in the U.K this morning showed that annual inflation eased a tad last month, but exceeded the Bank of England’s (BoE) target for the eleventh consecutive month, highlighting the ongoing squeeze on consumers pressured by the pound’s steep fall after the Brexit vote in 2016.

Consumer prices rose +3% on the year in December, compared with a rise of +3.1% a month earlier.

Digging deeper, there are mixed signals on inflationary pressures in the wider economy: prices charged by companies at the factory gate rose +3.3% on year in December – a faster annual rate than the previous month. Companies’ raw-material costs rose only +4.9% on year to mark the slowest pace of growth since July 2016, which was a month after U.K’s Brexit vote.

Note: The December print was fuelled by increases in prices of food, alcohol, tobacco and furniture.

Author

Dean Popplewell

MarketPulse

Dean Popplewell has two decades of experience trading currencies and fixed income instruments. His market analysis skills were honed during his tenure as global head of trading for firms such as Scotia Capital and BMO Nesbitt Burns.