CPI delayed, the shutdown deepens – And more data could still go dark [Video]

- CPI pushed to October 24, as the U.S. government shutdown halts key data releases and forces the Bureau of Labor Statistics (BLS) to recall limited staff.

- NFP remains postponed to November 7, while other major reports risk further delay if the shutdown extends.

- Markets now operate in a data vacuum, relying on yields, Fed speak, and sentiment - until the economic lights come back on.

![CPI delayed, the shutdown deepens – And more data could still go dark [Video]](https://editorial.fxsstatic.com/images/i/CPI_3.png)

A market operating without its compass

The U.S. economy’s pulse just went silent.

As the government shutdown stretches into its third week, the data flow that anchors global markets is grinding to a halt.

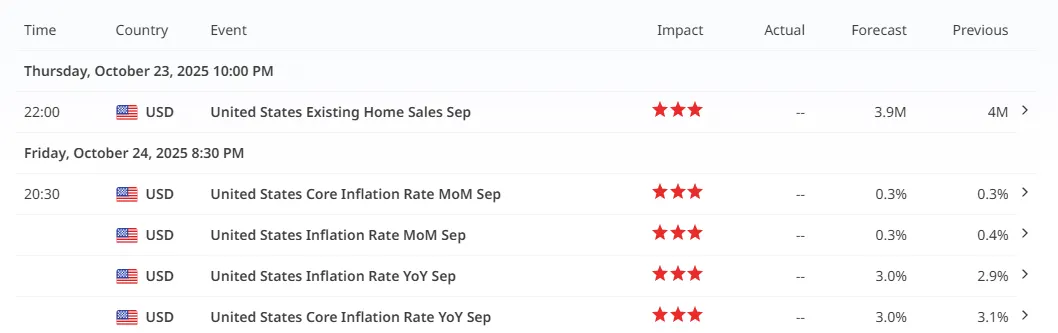

The September CPI report - originally due this week - has now been rescheduled for October 24 at 8:30 AM ET, according to the Bureau of Labor Statistics (BLS). Only a skeleton crew has been called back to publish this single, critical report, ensuring the Social Security Administration can calculate its 2026 Cost-of-Living Adjustment (COLA) on time.

Beyond that, everything remains in limbo.

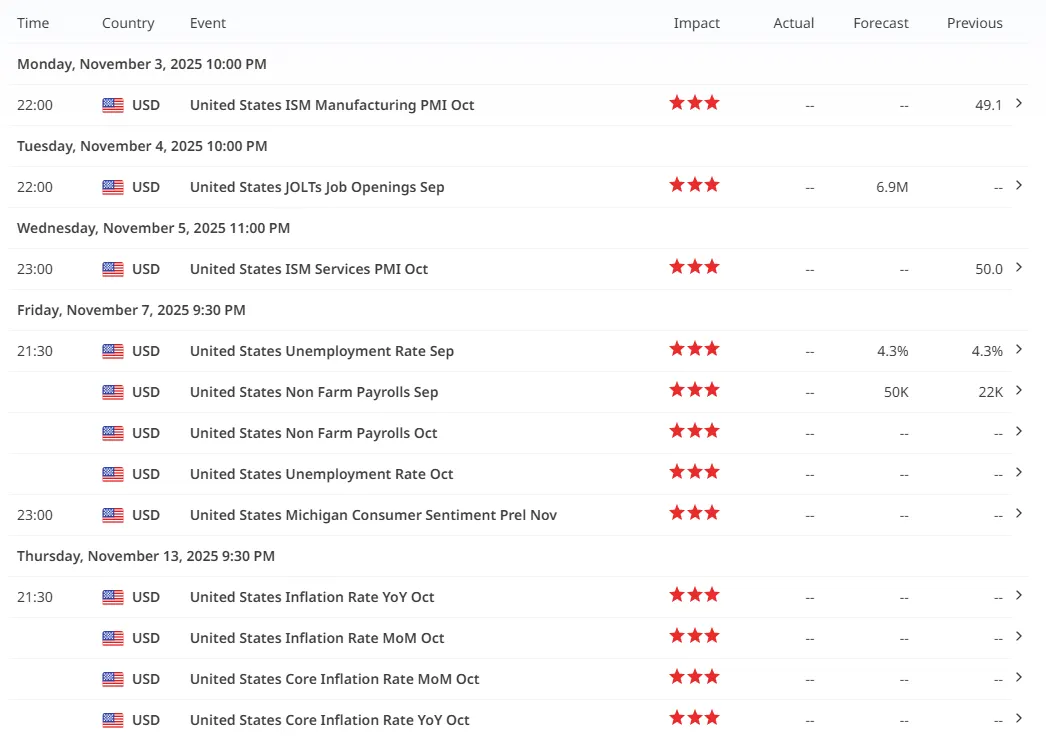

The Nonfarm Payrolls (NFP) report is now pushed to November 7, while the Producer Price Index (PPI), Retail Sales, and Housing Starts are still flagged as “tentative.”

If the shutdown drags further, even the October 24 CPI release could slip again.

That uncertainty is weighing heavily on the markets.

With no official inflation, jobs, or growth data, investors are navigating in the dark - pricing moves based purely on expectations, not evidence.

The broader impact: A spreading data blackout

The U.S. government shutdown isn’t just a political standoff - it’s a systemic blackout of information.

Federal agencies like the BLS, Census Bureau, and Bureau of Economic Analysis have furloughed most of their staff, leaving critical reports stalled.

That means traders no longer have access to real-time updates on:

- Inflation (CPI, PPI).

- Labor strength (NFP, JOLTS, Jobless Claims).

- Consumer trends (Retail Sales, Housing Starts).

Without these metrics, forecasting inflation or Fed policy becomes an exercise in guesswork.

It also reduces liquidity and amplifies volatility, as traders hedge uncertainty with gold, reduce risk in equities, and seek safety in the U.S. dollar - even if fundamentals are unclear.

This is why October 24’s CPI release now carries so much weight.

It won’t just show where inflation stands - it will decide whether the Fed’s 2025 rate path remains on track, or if the market must reprice everything from scratch.

The overall impact: Confidence, volatility, and global spillovers

The effects of this data freeze extend far beyond Washington.

When the U.S. stops publishing data, the entire global financial system loses its most important reference point.

From Tokyo to Frankfurt, central banks, investors, and multinational corporations rely on U.S. data to assess risk, adjust exposure, and calibrate decisions.

The absence of reliable data has three major implications:

- Investor Confidence Weakens – Institutional traders and portfolio managers depend on U.S. releases to validate positioning. Without them, confidence wanes, liquidity thins, and smaller market shocks produce outsized reactions.

- Volatility Gets Trapped, Then Explodes – In periods of data silence, volatility often compresses as traders sit out - only to surge violently when new information finally arrives. Expect the October 24 CPI to become one of the most heavily traded data prints of the year.

- Global Repercussions Intensify – Emerging markets, commodity exporters, and dollar-sensitive economies all depend on U.S. policy visibility. The longer the shutdown lasts, the greater the cross-market dislocation in FX, bonds, and commodities.

In short, this isn’t just a domestic data issue - it’s a temporary blindfold on global risk assessment.

Every central bank, fund manager, and retail trader is waiting for the same number: CPI.

Technical outlook – Markets in suspension

Market structure narrative

The U.S. Dollar Index (DXY) remains locked in a narrow H4 range, reflecting the broader uncertainty gripping global markets. With CPI delayed and NFP off the calendar, volatility has compressed into a coiling structure. Gold, meanwhile, continues to attract defensive inflows, staying firm above $4,200 amid fading real yields.

Gold outlook

Gold remains buoyed by data uncertainty and real yield stagnation.

- Bullish Case: If CPI faces another delay or prints softer-than-expected, gold could extend toward $4,300–$4,350.

- Bearish Case: A sharp rebound in yields or resolution of the shutdown could cap the rally near $4,180–$4,150.

Final thoughts

The market isn’t just quiet - it’s tense.

Every day without data builds more pressure beneath the surface.

Liquidity is thinning, traders are waiting, and the longer the shutdown persists, the sharper the eventual reaction will be when the lights come back on.

CPI on October 24 now represents far more than an inflation report - it’s the reset button for confidence, volatility, and direction.

And if the shutdown continues? Even that date could fade into uncertainty.

Author

Jasper Osita

Independent Analyst

Jasper has been in the markets since 2019 trading currencies, indices and commodities like Gold. His approach in the market is heavily accompanied by technical analysis, trading Smart Money Concepts (SMC) with fundamentals in mind.