Coffee still caught in the trade war crossfire

The coffee sector is still facing supply chain disruptions due to US tariffs; green coffee from Brazil and roasted coffee from Switzerland are particularly disadvantaged. American consumers are largely yet to see the tariff impact. EU coffee roasters are also reconsidering their strategy as trade flows shift.

The tariff commotion in the coffee trade

The coffee industry continues to experience significant disruptions due to a series of tariffs imposed on key coffee-producing and exporting nations. Notably, Brazil and Switzerland, ranked first and third, respectively, in terms of coffee export value to the United States, are subject to steep tariffs of 50% and 39%. While both countries are actively negotiating with the US to ease these trade barriers, the current situation places Brazilian and Swiss exporters at a marked disadvantage. In contrast, other coffee-producing nations such as Colombia and several Central American countries face a comparatively modest 10% tariff, giving them a competitive edge in the American market.

Brazil and Switzerland are worst off with current US tariffs

Top 10 coffee exporters* to US, ranked according to total export value in 2024.

*includes coffee beans, instant coffee and roasted coffee

Source: International Trade Administration, Eurostat, ING Research

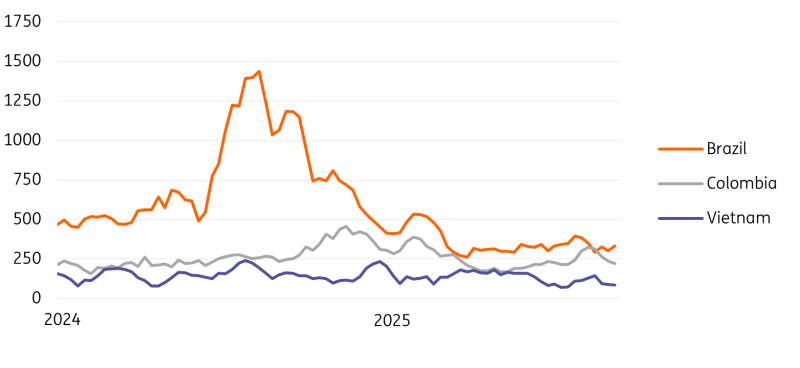

Ongoing market uncertainty, combined with the diverse characteristics of coffee from different origins, is causing a slow adjustment among US. buyers. Recent trade data offers an early glimpse into these shifts: coffee exports from Brazil to the U.S. dropped by over 75% in August compared to 2024 levels, as Brazilian traders hold onto stocks and farmers delay sales in anticipation of higher prices. In contrast, exports from Colombia and Vietnam remained stable through September. As a result, American coffee supplies are tightening. The disparity in tariff rates is expected to drive US buyers to reallocate sourcing away from Brazil toward more favourably taxed origins.

Brazilian coffee exports to the US down by more than 75% compared to last year

Coffee shipments to the US (TEU = standardised container unit), on a weekly basis.

Source: Vizion, ING Research

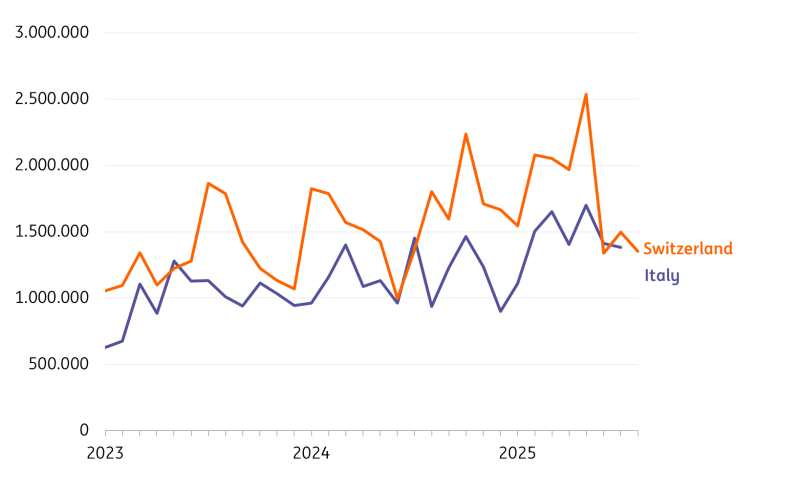

As for roasted coffee, Canada is the largest exporter to the US in volume (mainly decaf coffee), while Switzerland is the largest in value, with Italy completing the top three. Swiss exports of coffee capsules have been growing over the past few years, amounting to 1.1 billion EUR in 2024. These exports showed a steep drop over the summer, while Italian exports proved to be more stable. Even though coffee roasters in the EU who export to the US also face tariffs, for now, their competitive position has actually improved against Swiss competitors.

Steep reduction in Swiss coffee exports to the US; Italian exports prove more stable

Roasted coffee exports to the US in kilograms, up to August (Switzerland) and July (Italy).

Source: Swiss Impex, Eurostat, ING Research

US consumers: the worst tariff hit is yet to come

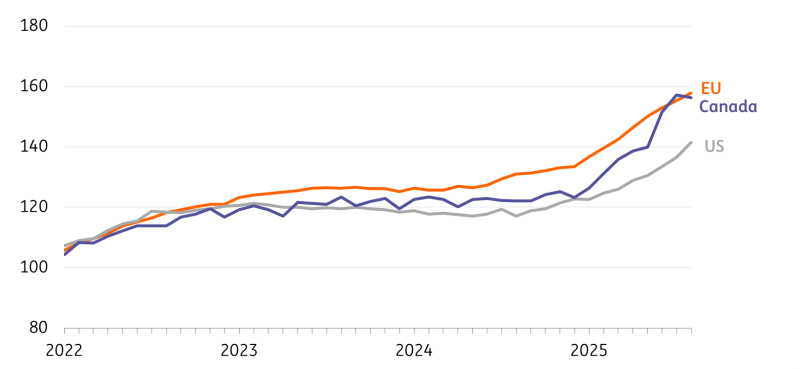

At the consumer end, rising coffee prices have been making headlines on both sides of the Atlantic as supplies are strained due to consecutive bad harvests in key coffee-growing countries. Consumer price indexes for coffee are up by 20% in the EU, the US and Canada. Up until July, prices in the EU and Canada went up at a much faster rate compared to the US, but that picture is starting to shift. In the States, ‘high-tariff’ coffee hasn’t yet hit the shelves. Roasters are using existing inventories first. The 50% tariff rate on Brazilian exports took effect on 6 August, and then it takes about a month to ship the coffee, which then needs to be roasted, packed and distributed to retailers. So, expect the tariff impact to start hitting those retailers in the fourth quarter.

Roasters will be trying to renegotiate with their customers. If they stick with the same quality coffee, they'll want to pass on the higher input costs. Or, they may change blends and trade down to a lower quality coffee to maintain price levels. Either way, it's not pretty for American coffee connoisseurs.

Nor is it great when you look at the future demand outlook. US roasters, such as JM Smucker and Keurig Dr Pepper, reported that volumes were already under pressure in the second quarter of this year due to strong price increases. The combination of continued upward pressure on prices and a weaker outlook for US household expenditure makes it very likely that we’ll see more demand destruction as the year progresses.

Consumer prices for coffee have increased more in EU and Canada than in the US

CPI for coffee, index Jan 2017=100, data up until August 2025.

Source: Eurostat, BLS, Stat Canada, ING Research

What does this mean for Europe?

For the European coffee industry and consumers, these developments are a mixed bag. The strength of the euro is mitigating some of the coffee price increases, which is traded in US dollars. If we see more demand destruction in the US, that could release some pressure on the supply side and on prices. But we don’t see that yet in coffee futures, which continue to trade around record highs. Tariffs make it more attractive for Brazilian exporters to sell more coffee to European customers, so that's a little bit of positive news.

But Europe is also a trading and processing hub for coffee, and the US is an important export destination for European coffee traders and roasters. Germany, for example, is a big re-exporter of green coffee beans to the States, while Italy and Switzerland are large exporters of roasted coffee.

For traders, increased volatility and uncertainty generally provide an opportunity to accommodate changes in demand as long as they have the right positions. European roasters, however, have become less competitive in the US compared to North American companies, which do more post-tariff value-added activity locally. That’s a setback, since the US has been a lucrative growth market for years. For European roasters, conversations at boardroom level will centre on how to now approach the US market and whether it’s wise to set up shop or increase their presence in the US. This is something that companies like Lavazza and Illy have already been hinting at. More local presence could not only decrease the tariff impact but also reduce the compliance burden due to the new EU Deforestation Regulation. The drawbacks of more ‘local for local’ roasting are that it would require more investment, it takes years to set up a facility, and it would leave their European facilities with excess capacity.

Reshoring manufacturing in strategic sectors has been a priority for Donald Trump. While bringing additional coffee roasting facilities may not have been an explicit goal, it could be an ultimate caffeine-rich consequence of the current tariff policy.

Read the original analysis: Coffee still caught in the trade war crossfire

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.