China Shot The U.S. Equity Bull

Those who followed us know that our proprietary model concluded a high probability of entering a recession in 2020. The coronavirus outbreak came on top of that. It is most likely the straw that broke the camel’s back as it sent major parts of China into lockdown. The epidemic has distinct similarities to the subprime crisis in 2007. There is a general sense of public distrust as Chinese censorship and disinformation triggered fear during the past few weeks. The reaction to the virus may have been exaggerated as pictures of empty streets in Chinese metropoles reveal.

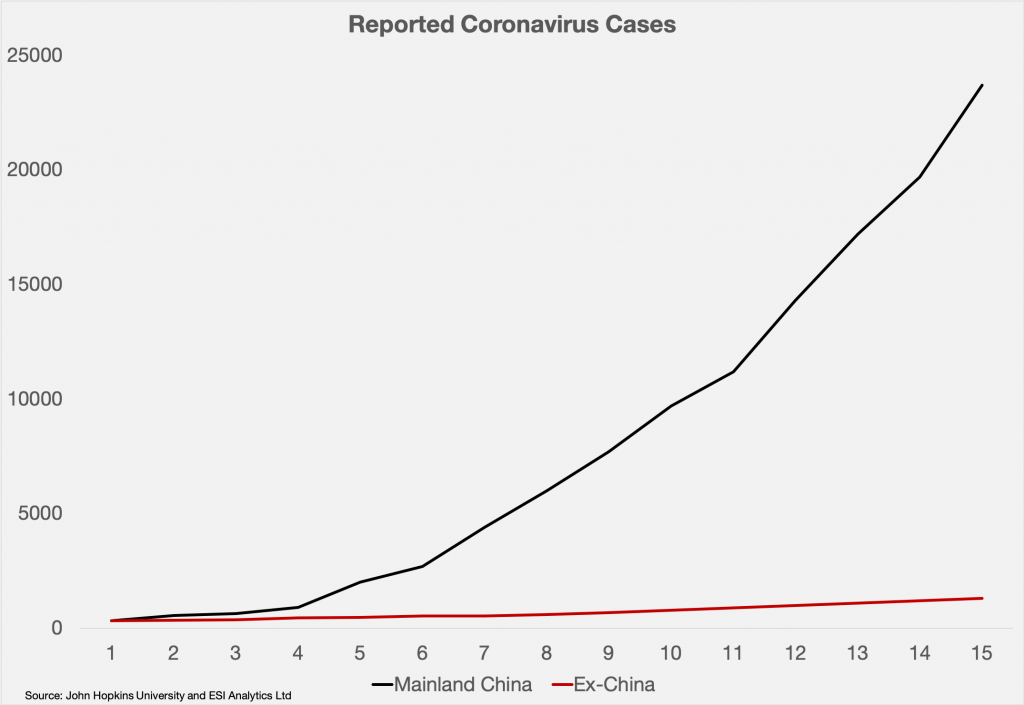

Nonetheless, Chinese authorities have a track record for reporting false data. That backfired in the case of the coronavirus outbreak as the government aimed to let everyone know that the situation is well handled and under control. Unfortunately, it was not as today’s statistics expose. Chinese authorities reported an increase from 300-31,200 during the period January 21st, 2020 until February 7th, 2020. Our chart shows the problem with Chinese statistics as it overlays cases reported outside of China with a lag. Ex-china data starts on February 7th, the day that recorded the same base of roughly 300 confirmed coronavirus cases outside of China. Two weeks later, a total of 1,300 cases were reported outside of China versus 23,700 in China. The chart below reveals that official Chinese data is statistically unrelated to evidence outside of China. Therefore, it should be no surprise that Chinese citizens distrust their government as it is most likely not giving them an accurate picture of a life-threatening situation.

Regardless of being exaggerated or reasonable, the most recent events have a negative impact on global economic activity. There have been recent headlines about supply chain disruptions. However, the damage goes beyond the supply side when China stays home and does not go shopping. Domestic car sales plunged, for example, 92% in the first half of February. The demand side is affected and China has been the top contributor to global growth during the last cycle. General distrust in China makes things worse than they are on a global scale. We will witness a large dent in Chinese growth during Q1 2020. Moreover, Japan’s GDP shrunk at a rate of 6.3% during Q4/2019 already. Additionally, South Korea’s president warned that emergency steps are necessary to prevent an economic crisis. Germany’s growth stagnated during the most recent quarter as well. Hence, the three largest economies after the U.S. are struggling with their GDP growth.

That will bring a strong headwind for the U.S. economy. The most recent apple sales warning is the best example of how interlinked the global economy is. Problems in Asia affect the U.S. economy and equity market eventually. Yet, there is still record complacency among investors and the media. The bad news is that the wheels seem to come on U.S. equities. Five out of the seven main S&P cyclical sectors have stagnated or are down since our write-up near the January high. Subsequently, investor’s favorite stocks such as Apple, Facebook, Intel, and Microsoft did not confirm the most recent highs.

Evidence that several degrees of trend are coming to an end builds up. Our macro outlook showed that the global economy enters into a stage that was historically at the epicenter of tipping into a recession. Moreover, sentiment and position indicators reveal exuberant expectations among market participants. Technicals have been getting on the same side of the ledger lately. The U.S. equity bull looks clinically dead at this stage.

Interested in more of our ideas? Check out Scienceinvesting for more details!

Author

Science Investing Team

Science Investing