China outlook: The choice between retaliation or de-escalation

Key points

-

China faces dual pressures from external tariffs and a domestic slowdown: The potential for new U.S. tariffs under Trump could trim China’s GDP by 1-2%, compounding existing challenges like a struggling property sector, weak consumer demand, and local government debt concerns.

-

Both retaliation and de-escalation paths carry risks: Aggressive retaliation (e.g., tariffs or export controls) could hurt China’s high-tech sectors and worsen global trade tensions. Even devaluation of the yuan comes with risks of capital outflows and damage to investor confidence. De-escalation may stabilize markets but require concessions on trade or currency. How far these concessions go will determine the rebound time for China.

-

Policy response will shape market outcomes: China is likely to deploy targeted fiscal stimulus and structural reforms to support domestic demand, but the yuan remains at risk of depreciation, while Chinese equities may see selective opportunities.

As 2025 kicks off, China faces two daunting challenges. First, the return of Trump brings with it the looming threat of hefty U.S. tariffs. The proposed 60% tariff on Chinese imports could spark a renewed trade wary. Second, even without external pressure, China’s domestic economy is struggling with a slowdown, characterized by weak consumer confidence, a battered property sector, and looming debt issues. The question is, how will Beijing respond?

China has two broad options: retaliate or seek to de-escalate tensions. Each path comes with distinct implications for equities, the yuan, and even the U.S. dollar. A tough stance might trigger short-term relief but worsen economic pain, while a cooperative approach could stabilize markets and bolster long-term growth prospects.

Tariffs: Take a swing or call for truce

Trump’s campaign promises included a tariff hike of up to 60% on Chinese imports. Whether the administration immediately enforces these tariffs or uses them as a bargaining chip remains uncertain. History tells us that when tariffs go up, China’s exports—and its GDP—take a hit. Some forecasts suggest that new tariffs of this magnitude could shave 1-2% off China’s GDP over the next year. If tariffs are imposed in phases or capped at a lower level, the damage could be manageable. However, a full-on trade war would amplify pressures on an already fragile economy.

China’s ability to retaliate with tariffs of its own is constrained by the trade imbalance with the U.S. While U.S. exports to China are a small share of U.S. GDP, China’s exports to the U.S. represent a significant portion of its economy. Retaliating with outright tariffs risks hurting China’s emerging industries, particularly in tech and high-end manufacturing, which remain strategic priorities. Any signs of a relief for Chinese assets in a retaliation scenario would likely be short-lived, as prolonged trade tensions would weigh heavily on growth.

However, China may also focus on non-tariff strategies, such as continuing its export restrictions on critical minerals like rare earth elements (REEs). Still, the impact of these measures has been limited so far, as alternative sources of REEs are emerging globally.

Another measure that China hinted at was the plan to allow yuan devaluation next year. The controlled loosening of the grip on the currency has made this look likely, but signals have still been mixed. Understandably, this is not an easy choice as it could undermine investor confidence, trigger capital outflows, and create challenges for businesses as import costs rise. Beijing may be better off focusing on keeping the yuan steady to safeguard financial stability and avoid full-blown currency wars as its best shot at recovering from its latest economic headwinds. Therefore, a more likely path for the yuan would be a slow-burn devaluation rather than a sudden one.

Conversely, if China pursues de-escalation and negotiates a deal, it could help to boost the yuan and potentially bring a decline in the overbought U.S. dollar. A weaker dollar, combined with lower trade uncertainty, could improve sentiment toward Chinese assets. However, a de-escalation would need concessions from China on trade or currency. These could include renewed Chinese purchase pledges, yuan appreciation, or Chinese cooperation in resolving geopolitical challenges such as the one in Ukraine, for example. How far these concessions go will determine the time it takes for China to rebound.

Domestic dilemmas: A combination of stimulus and structural reform

Even without external shocks, China’s domestic landscape looks grim. After a brief stimulus-driven rebound in late 2024, the economy now faces headwinds from weak local government finances and deflationary risks. The property sector crisis has wiped out household wealth, leading to reduced spending and weak private sector investment—classic signs of a balance sheet recession, where debt repayment takes priority over consumption and investment. In such conditions, rate cuts lose their effectiveness because lower borrowing costs don’t drive demand when balance sheets are under pressure.

However, there’s a positive shift underway: Beijing is focusing on fiscal stimulus rather than rate cuts, which could provide a more direct boost to growth. Key fiscal measures may be announced during the Two Sessions annual legislative meeting in March, making the first half of the year more about waiting for policy clarity, while the second half could be pivotal for an earnings rebound driven by fiscal reforms and potential trade war de-escalation with the U.S.

A key indicator to watch: inflation. If inflation picks up, it could signal demand recovery, which markets would view favorably.

A more structurally optimistic outlook for China could emerge if reforms are implemented. The property sector, which poses a significant challenge, needs attention. In the consumer sector, addressing high levels of precautionary savings and low consumer confidence is crucial to sustainably boost sentiment. This will likely require increased spending on welfare, pensions, and healthcare to strengthen the social safety net. Additionally, a comprehensive debt restructuring plan to assist local governments struggling with repayments would boost investment spending.

Equities: A lot of bad news is priced in

Despite ongoing risks, Chinese equities are not without hope. The MSCI China Index currently trades at a forward P/E of 9.7x, significantly below its 5-year average of 11.62x. This suggests room for upside, especially if policy clarity improves in H2 and trade uncertainty wanes.

Investors may recall that last September’s aid package powered MSCI China to a 16% gain in 2024, breaking a three-year losing streak. The rally was led by IT, communications, and financials, sectors that could see continued strength if fiscal stimulus is ramped up in 2025. If the fiscal measures are large-scale and consumer focused, there could be a rebound in staples, e-commerce, travel and sportwear sectors.

China’s key strategic sectors include technology (major internet and hardware players), advanced manufacturing, EVs and renewables. These remain a core focus for Beijing’s long-term growth strategy, with strong policy support expected.

However, sectors tied to property weakness may take longer to recover, limiting the scope of an immediate recovery in real estate, infrastructure and construction sectors as well.

Additionally, investors should keep an eye on regional fund flows. Markets have turned underweight on South Korea citing political risks, and neutral on India due to slowing growth. Taiwan’s rally, driven disproportionately by TSMC, now looks stretched. Even modest positive news out of China could trigger a reversal of flows back into Chinese assets.

Yuan outlook: Hard to call for sustained strength

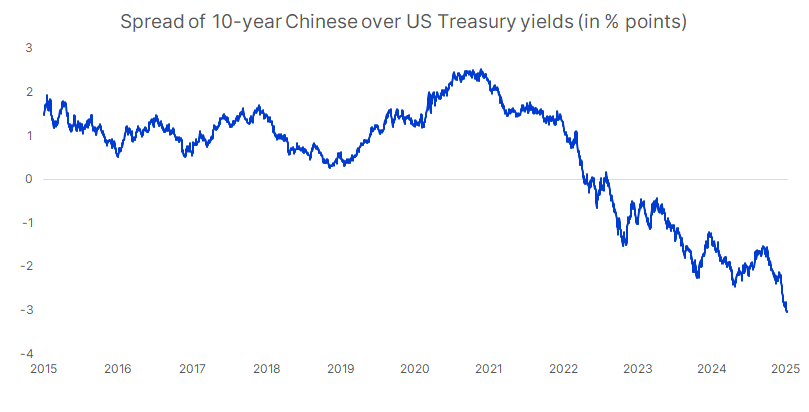

The Chinese yuan is currently under significant pressure due to China's ongoing bond rally, which has driven yields to record lows. The 10-year benchmark yield has dropped nearly 40 basis points over the past month, falling below 1.60% and widening the US-China yield gap to an unprecedented 300 basis points. This is exerting substantial pressure on the yuan. The currency's weakness is likely to persist due to China's economic challenges, the carry differential, and the strength of the US dollar. Additionally, China may need to keep the yuan weak to support its export sector.

Source: Bloomberg and Saxo

However, the yuan could see an appreciation if Beijing successfully negotiates a trade deal with Washington, reversing its recent weakness. Such an outcome would provide broad relief to Chinese assets and add downward pressure on the U.S. dollar. This could also open up room for stronger stimulus from the Chinese authorities.

Sustained strength in the yuan, however, would require a U.S. recession and steeper Federal Reserve rate cuts, and an improved economic outlook for China’s economy to close the wide interest rate differential to the U.S. That is a lot to ask for in 2025.

Read the original analysis: China outlook: The choice between retaliation or de-escalation

Author

Saxo Research Team

Saxo Bank

Saxo is an award-winning investment firm trusted by 1,200,000+ clients worldwide. Saxo provides the leading online trading platform connecting investors and traders to global financial markets.