Bad economic reports? Yes, but they were supposed to be bad

Factory orders and a terrible ISM report are in the news today. But numbers that would have been shocking in January, no longer are.

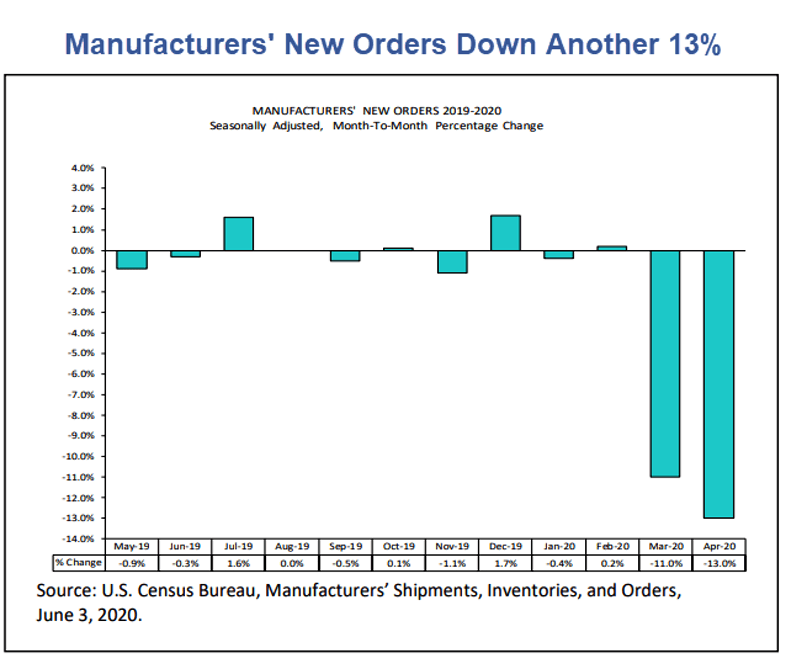

Factory Orders Plunge Another 13.0%

The Census Department's report on Manufacturers' Shipments, Inventories, and Orders for April was bad, as expected.

New Orders

New orders for manufactured durable goods in April, down three of the last four months, decreased $36.3 billion or 17.7 percent to $168.7 billion, down from the previously published 17.2 percent decrease. This followed a 16.7 percent March decrease. Transportation equipment, also down three of the last four months, led the decrease, $24.3 billion or 48.3 percent to $26.1 billion. New orders for manufactured nondurable goods decreased $21.2 billion or 9.0 percent to $215.6 billion.

Shipments

Shipments of manufactured durable goods in April, down three of the last four months, decreased $42.4 billion or 18.2 percent to $191.2 billion, down from the previously published 17.7 percent decrease. This followed a 5.5 percent March decrease. Transportation equipment, also down three of the last four months, led the decrease, $31.7 billion or 43.1 percent to $41.8 billion. Shipments of manufactured nondurable goods, down four consecutive months, decreased $21.2 billion or 9.0 percent to $215.6 billion. This followed a 5.4 percent March decrease. Petroleum and coal products, also down four consecutive months, led the decrease, $11.9 billion or 32.0 percent to $25.4 billion.

Unfilled Orders

Unfilled orders for manufactured durable goods in April, down two consecutive months, decreased $17.6 billion or 1.6 percent to $1,107.6 billion, unchanged from the previously published decrease. This followed a 2.1 percent March decrease. Transportation equipment, also down two consecutive months, led the decrease, $15.7 billion or 2.0 percent to $759.6 billion.

Inventories

Inventories of manufactured durable goods in April, up two consecutive months, increased $0.6 billion or 0.2 percent to $425.3 billion, unchanged from the previously published increase. This followed a 0.5 percent March increase. Transportation equipment, up twenty-one of the last twenty-two months, led the increase, $0.4 billion or 0.3 percent to $143.0 billion. Inventories of manufactured nondurable goods, down four consecutive months, decreased $3.2 billion or 1.2 percent to $261.2 billion. This followed a 3.5 percent March decrease. Petroleum and coal products, also down four consecutive months, drove the decrease, $3.7 billion or 12.1 percent to $27.1 billion. By stage of fabrication, April materials and supplies increased 2.3 percent in durable goods and decreased 1.2 percent in nondurable goods. Work in process decreased 0.7 percent in durable goods and 1.5 percent in nondurable goods. Finished goods decreased 1.2 percent in durable goods and 1.1 percent in nondurable goods.

Shocking? No

The Econoday consensus estimate was -14.0% nearly on the mark.

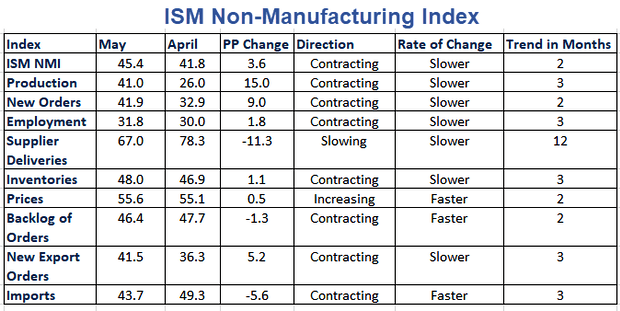

ISM Non-Manufacturing Index

The Econonday consensus was nearly on the mark a 44.0 ve the report NMI of 45.4.

The most noteworthy item was supplier deliveries slowing for 12 months.

That item tells you the economy was cooling rapidly even before Covid-19 hit.

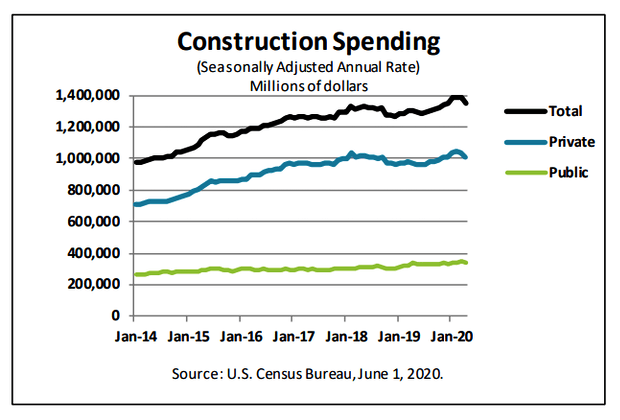

Construction Spending

Yesterday, the Census Department published the Construction Spending Report for April.

It was a little better than expected. The Econoday consensus was -5.5% and the report came in at -2.9%.

But the Census Department revised March down to 0.0% from +0.9% so the consensus estimate was close to the mark.

Here it is June, and we are looking at economic reports or revisions for March in the midst of a Covid-19 pandemic.

Complaints

Reader complaints are pouring in. People want me to talk about the economy even though most of the reports are useless.

Economic Synopsis

The reports are universally bad, understood in advance to to be bad, yet most will improve.

I am out of ways to talk about unermployment. I have talked about the V-Shaped recovery or lack thereof numerous times.

What's Important

- Like it or not, it's the election.

- Like it or not, it's military threats by president Trump.

- Like it or not, one cannot easily sepearate the economy from political actions.

- Like it or not, Trump is acting in many ways like a third-word dictator.

- Like it or not, the unfortunate fact is many of my readers cheer Trump's actions even though anyone with an ounce of sense is distancing themselves from Trump.

It you want to pretend this is not happening, or worse yet, you want to cheer Trump for actions that disturb a former chairman of the Joint Chief of Staff and even the current Secretary of Defense (more on that coming up), then bury your head in the sand or turn on Fox news.

But if you are concerned about what is really important, then tune in here.

Threats Don't Bother Me

I don't care how many readers threaten to leave. I will continue to discuss what I believe is important.

Unconstitutional or radical threats and actions by president Trump are at the top of my list.

If you disagree that Trump crossed the line, then open your eyes and read this: Something Changed for the Better: Trump's Bubble Just Shattered.

If you still support those actions, I pity you.

Author

Mike “Mish” Shedlock's

Sitka Pacific Capital Management,Llc