Asia week ahead: Inflation and PMIs in focus

Inflation and PMI indices across the region dominate the Asian macro news flow for the week ahead.

Inflation and central banks

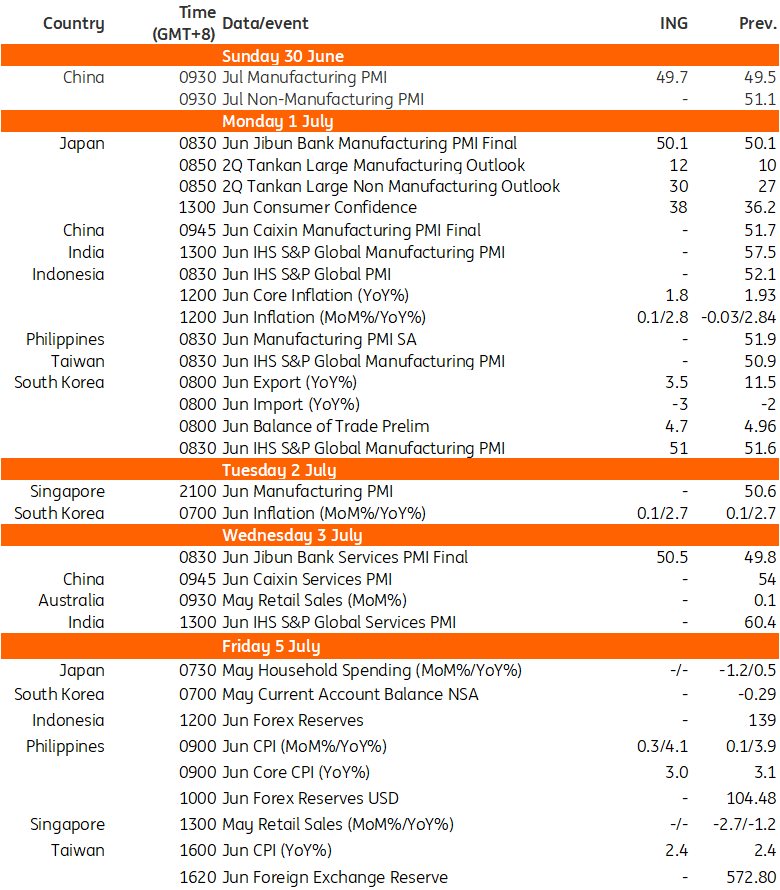

Australia: Following another set of poor inflation figures, markets will be poring over the Reserve Bank of Australia (RBA) minutes of the June policy meeting. RBA Governor Michele Bullock has already admitted that the central bank discussed rate hikes at that meeting, so any further indication of what conditions might be required to bring about a hike would be potentially market-moving.

Inflation: Both the Philippines and Indonesia publish inflation data this week. Philippine inflation will likely increase from the 3.8% year-on-year rate recorded for April and come in at about 4.1% YoY. Last May, the price level was depressed by sharp falls in transport costs and we don’t expect such a big decline this year. Rice prices appear to be rising at a slower pace, but there are likely to be some offsetting rises from seasonal fruit and veg prices that will result in about a 0.3% month-on-month increase in the price level from April. In Indonesia, we expect inflation to remain at about 2.8% YoY in June. While this is still low, the IDR’s slump may yet pressure Bank Indonesia to respond with further supportive rate hikes.

We expect Korean consumer inflation to stay at an elevated level of 2.7% YoY in June. Fresh food and manufactured food prices continued to rise but were partially offset by falling gasoline prices.

Taiwan also publishes inflation data. The June CPI and PPI inflation data are scheduled for Friday 5 July. We are looking for a small uptick in CPI inflation to 2.4% YoY (from 2.24% in May). There has been an abundance of caution on inflationary pressure after electricity prices and amid a reacceleration of housing prices, but it looks like inflation will remain within a manageable range and should pull back toward the 2% target level by the fourth quarter of the year.

Business activity

China: Various PMI data will be the focus for China in the week ahead. The National Bureau of Statistics publishes the official June China manufacturing and non-manufacturing PMIs on Sunday morning. We are looking for a slight uptick of the manufacturing PMI to 49.7 from 49.5 – a little more optimistic than the consensus forecast which expected no change. Markets are also looking for no change in the non-manufacturing PMI from last month’s 51.1 level. The Caixin PMI releases come later in the week, with the manufacturing PMI out on Monday. Markets are looking for a slight downtick from 51.7 to 51.5, and the services PMI is out on Wednesday.

Rest of Asia: PMI indices are also published for Taiwan, Malaysia, Philippines, Thailand, Vietnam, India and South Korea

Japan: The Bank of Japan's Tankan survey will confirm the improvement in business sentiment. A normalisation in auto production, a recovery in exports and tourism, and an optimistic outlook for consumption should all boost business sentiment. However, we believe the weak JPY is starting to eat into business confidence as excessive input price increases squeeze corporate profits.

Trade data

South Korean exports should grow solidly again in June on the back of strong chip exports. Early trade data showed a 50% increase in semiconductors. However, we think unfavourable calendar effects will cause export growth to slow from 11.5% in May to 3.5% YoY in June. The optimistic outlook for the semiconductor cycle will support the manufacturing PMI above the 50 level. But other manufacturing sectors are suffering from tight financial conditions and sluggish domestic growth, and the PMI should edge down to 51 from the previous month’s 51.6.

Key events in Asia next week

Source: Refinitiv, ING

Read the original analysis: Asia week ahead: Inflation and PMIs in focus

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.