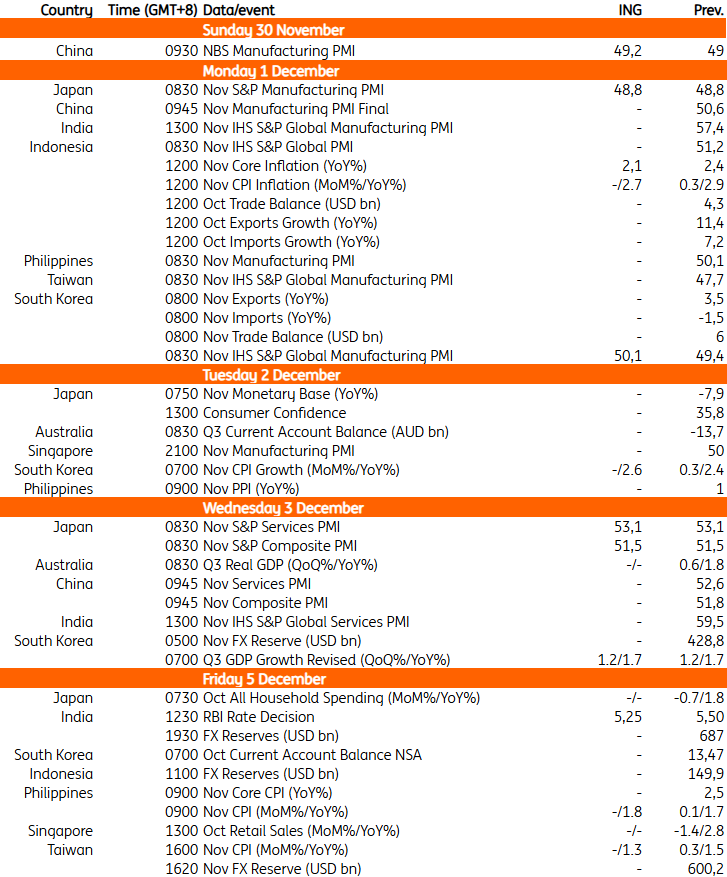

Asia week ahead: Indian rate decision and key data from China, Taiwan, South Korea

The Reserve Bank of India is expected to cut rates by 25 bps. Key economic data releases include China’s purchasing managers’ index, Taiwan's inflation, and South Korea's trade, PMI, and inflation.

India: RBI expected to cut rate by 25 bps

We expect the Reserve Bank of India to cut its repo rate by 25bps to 5.25% on Friday. Inflation has been very subdued, driven by lower food prices. Growth momentum, meanwhile, is set to moderate in the coming quarters amid external headwinds. The performance of exports has deteriorated sharply. Indian shipments to the US fell by over 30% in September compared to July after the imposition of 50% tariffs.

Taiwan: Inflation expected to decline

Taiwan releases its November CPI inflation data on Friday. We expect the CPI to moderate to 1.3% year-on-year, down from around 1.5% YoY in October. Inflation has remained below 2% since May. Despite this, we expect the central bank to remain on hold at its last meeting of the year in mid-December amid stronger-than-expected growth.

China: Manufacturing PMI expected to rebound slightly

China’s purchasing managers’ index, out Sunday, will be the highlight of the week. The official November PMI data comes out on Sunday. We expect a modest rebound in the manufacturing PMI to 49.2, up from 49.0 in October. The non-manufacturing PMI has recently been teetering on the edge of contraction territory for the first time since 2022.

South Korea: Exports expected to continue growing, while inflation rises

South Korea releases trade, PMI, and CPI data. Driven by robust semiconductor demand, exports are projected to continue rising in November. Early November data suggest substantial growth in automobile and ship exports as well. The October tariff agreement with the US likely boosted exports, and suggests the manufacturing PMI will move above neutral.

CPI inflation is projected to reach 2.6% YoY in November, mainly due to last year's low base from temporary fuel tax cuts. Gasoline prices rose sharply, largely due to a weaker KRW, while fresh food prices fell amid strong harvests.

Key events in Asia next week

Read the original analysis: Asia week ahead: Indian rate decision and key data from China, Taiwan, South Korea

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.

![How Wall Street rigs the game [Video]](https://editorial.fxsstatic.com/images/i/market-chaos-01.jpg)