$60 billion of forced buying: Who gets to sell SpaceX into it?

The Elon Musk-founded SpaceX (SPCX) has spent its first few sessions on Nasdaq doing exactly what an engineered float is built to do: holding firm because almost nobody is allowed to sell. The demand that hung over the June 12 debut was never the question; the queue was real and the open was a stampede.

The more telling question, now that the initial public offering (IPO) is priced and the stock trades, is the one the deal's own machinery answers: who is it built to pay, and who is left holding the stock when it has? The staggered lockup and the forced index buying are two halves of one mechanism, built to keep the float starved while the benchmarks are wired to buy, so that the early money can step out into a mechanical bid at the exact moment the last hands are obliged to step in.

The calm is the scarcity, not the conviction

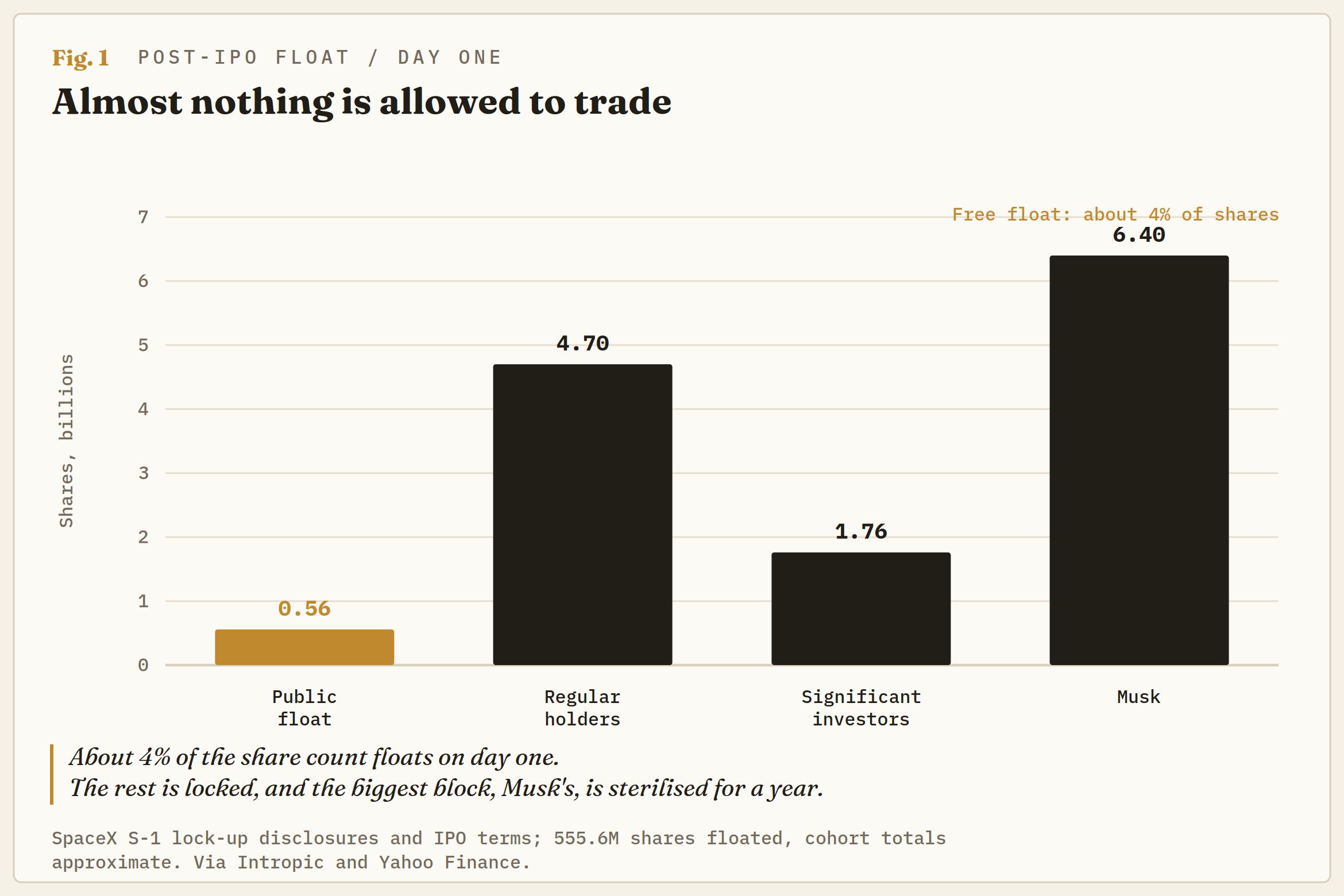

Treat the first week as a supply story, not a verdict on value. Only a thin slice of SpaceX can actually change hands right now. The public float is small against a company carrying a $1.75 trillion price tag, the insiders are locked, and the friends-and-family allocation is the one unlocked block, much of it sitting tight rather than being the hand that breaks the open. Set that against demand the company engineered hot, with 30% of the deal carved out for retail, three times the usual sliver, and the tape almost has to hold. It is bid because there is next to nothing offered. That is not the market blessing 90 times sales. It is the market discovering there is nothing to buy.

The winners booked their gains before you heard the bell

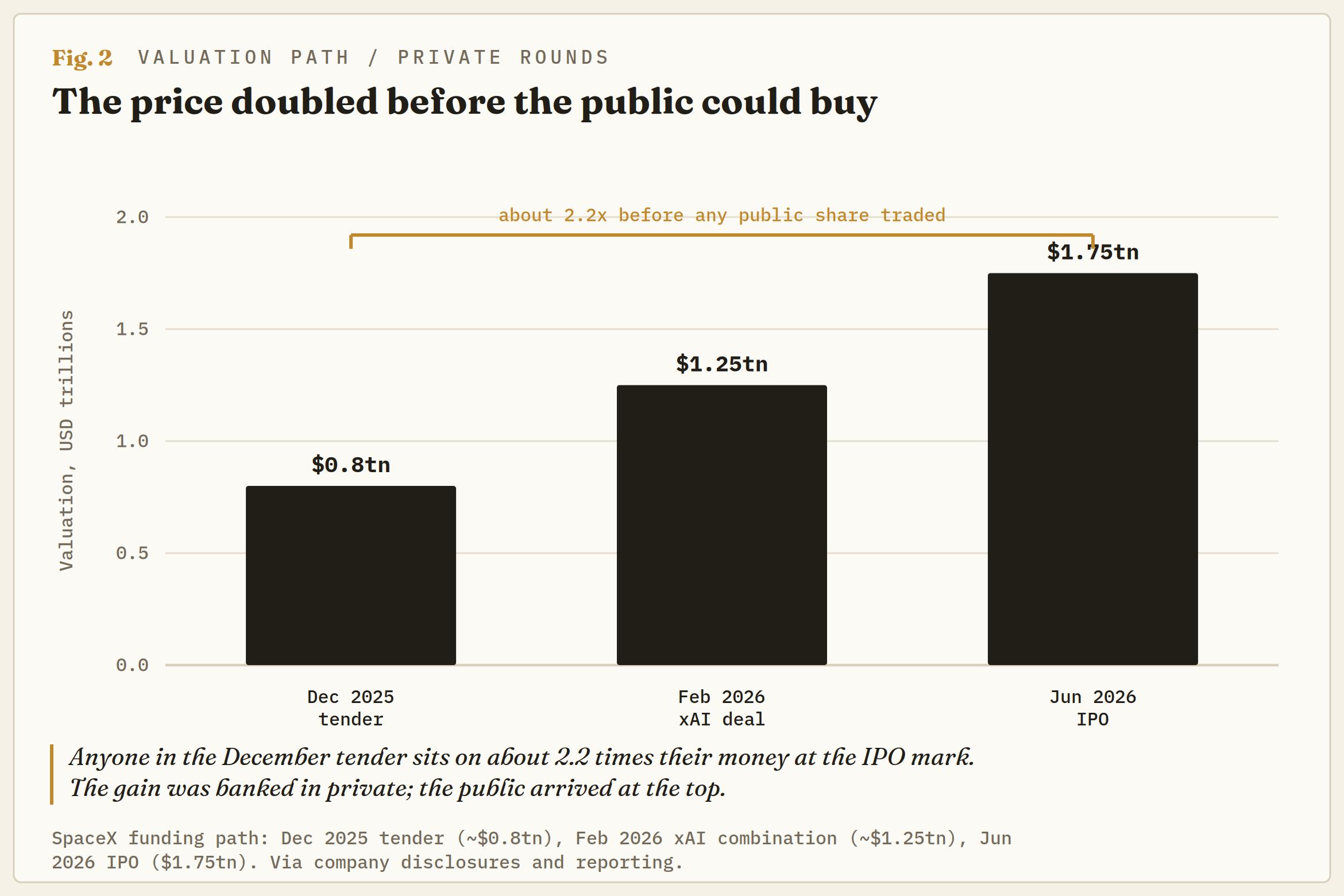

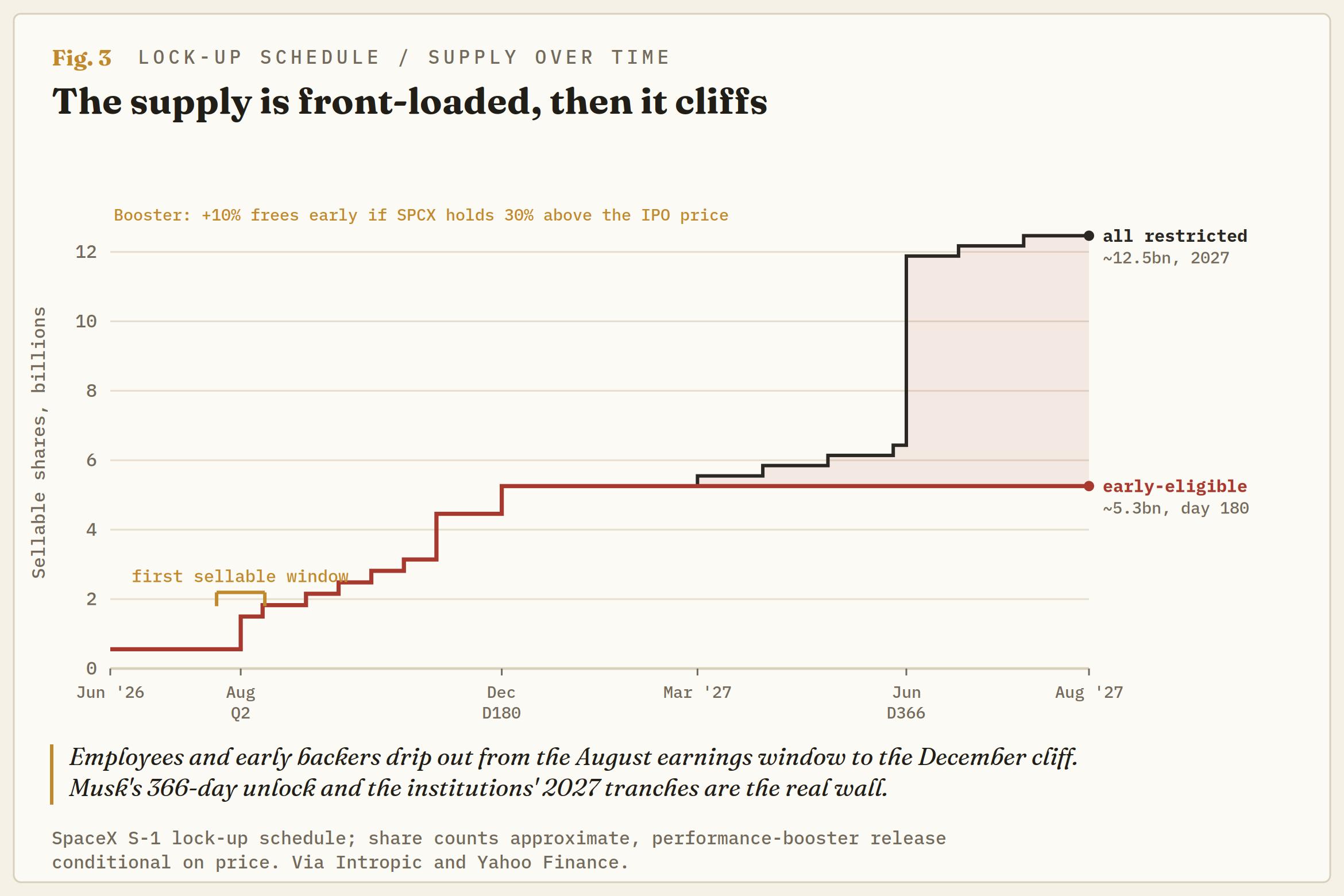

Run down who is positioned to profit and a pattern appears: they were all early, and the schedule lets them leave in an orderly line. Anyone who bought into the roughly $800 billion tender last December now sits on about 2.2 times their money at $1.75 trillion, on paper. Long-tenured employees hold grants struck against valuations a fraction of today's. The friends-and-family allocation can sell from day one. The employees and early backers, some 4.7 billion shares between them, sit on a staggered schedule that lets them start selling well before the standard 180-day cliff, in tranches rather than all at once.

Musk and the institutional backers are locked far longer, Musk for a full 366 days, though their paper gains dwarf everyone else's. Goldman Sachs and the syndicate already have their fees and a greenshoe. And the fast money that does this for a living is front-running the index event, buying ahead of the forced bid it knows is coming. None of these gains is locked in by conviction. Each is locked in by timing, and the timing is the part SpaceX wrote itself.

The forced buyers never got a vote

Every seller needs a buyer, and SpaceX has arranged for a very large one that cannot say no. For now, S&P Dow Jones has kept its profitability rule and left the stock out of the S&P 500. Nasdaq did the opposite, bending its rules to wave SpaceX into the NASDAQ-100 roughly 15 trading days after listing, with the Russell indices close behind. Every fund built to track those benchmarks then has to buy, at more than 90 times sales, not because a manager judged the price fair but because the rulebook says so.

Those funds are the index trackers sitting inside millions of 401(k) and pension accounts, more than $30 trillion of largely passive money that must own SpaceX once the benchmark does. Estimates of that forced buying run from $22 billion to as high as $60 billion. It is patient, price-insensitive and obligated. In other words, it is exit liquidity.

The exits are timed to the bid

The mechanism only works because the dates are stacked in the right order. The index run-up comes first, as trackers position for inclusion into early July. Then comes the part that breaks from convention. Rather than the standard 180-day lockup, the employee and early-backer block runs on a staggered schedule that opens as early as the second trading day after the first quarterly earnings as a public company, likely around August, then drip-feeds the float through a run of time-based tranches into the 180-day mark in December.

That early unlock does double duty. It widens the float, which lifts the index weighting, forcing the passive funds to buy still more, at the very moment those holders are first cleared to sell. There is even a price trigger written in: an extra slug frees if the stock holds 30% above the IPO price after earnings, so the forced bid can manufacture the very supply it then has to absorb. Index-flow analysts have flagged how neatly the unlock and the forced-buying calendars overlap, which is roughly the point at which the word passive stops meaning anything.

The template is Tesla (TSLA) in 2020: front-running money drove the inclusion run-up, the forced bid filled, the buying exhausted, and the stock drifted, leaving the benchmark holder long at the top. SpaceX has simply written that sequence into the deal.

The calendar to trade, and the hands left holding

There is a tradeable calendar here even without a single price print on the screen. The first marker is the inclusion run-up into early July, as the trackers build positions ahead of the forced buy. The second is the supply that arrives around the August earnings unlock, the first window in which insiders can sell into all that passive demand. The third is the 180-day cliff in December, when the rest of the employee and early-backer stock comes free. The biggest blocks land later still: Musk's stake unlocks in one go at day 366, in mid-2027, and the large institutional holders release in tranches through the spring and summer of that year.

That is the real supply wall, and it arrives long after the forced bid has done its buying. The lean is straightforward: the bid under SpaceX is mechanical and finite, so the risk-reward for anyone buying late skews against them into each of those events, the more so for a company that lost $4.9 billion last year and $4.3 billion in the first quarter alone, with little under the price but the story once the forced bid is filled. The tape stays bid only while the float stays starved; the line in the sand is whether real, discretionary demand turns up before the locked shares do.

That is the tension the first quiet week is hiding. The calm is not a verdict, it is a countdown. When the float finally opens, either fresh buyers step in to replace the ones the rulebook compelled, or the last hands in the queue, the index-tracking retirement money that never got a say and the retail crowd that chased the open, are left holding the parcel once the early entrants have gone. On this deal you are early, or you are the exit, and the calendar already knows which.

Author

Joshua Gibson

FXStreet

Joshua joins the FXStreet team as an Economics and Finance double major from Vancouver Island University with twelve years' experience as an independent trader focusing on technical analysis.