Why Goldman Sachs and JPMorgan think this payrolls report could rattle markets

Thank you for reading my posts. You may have noticed that some articles are now appearing behind a paywall.

Going forward, my trader interpretations of leading Wall Street banks’ actual research and institutional strategy notes ( and eventually those notes themselves) will become a much bigger part of The Dark Side of the Boom. These are often the ideas that move markets before the headlines catch up, and I believe they offer some of the most valuable insights for traders and investors trying to stay ahead of the curve.

Non-premium content remains free, in line with my commitment to keeping my blog accessible to everyone..

If you’d like to bypass the paywall entirely, you can either open an Axi trading account or subscribe directly through Substack.

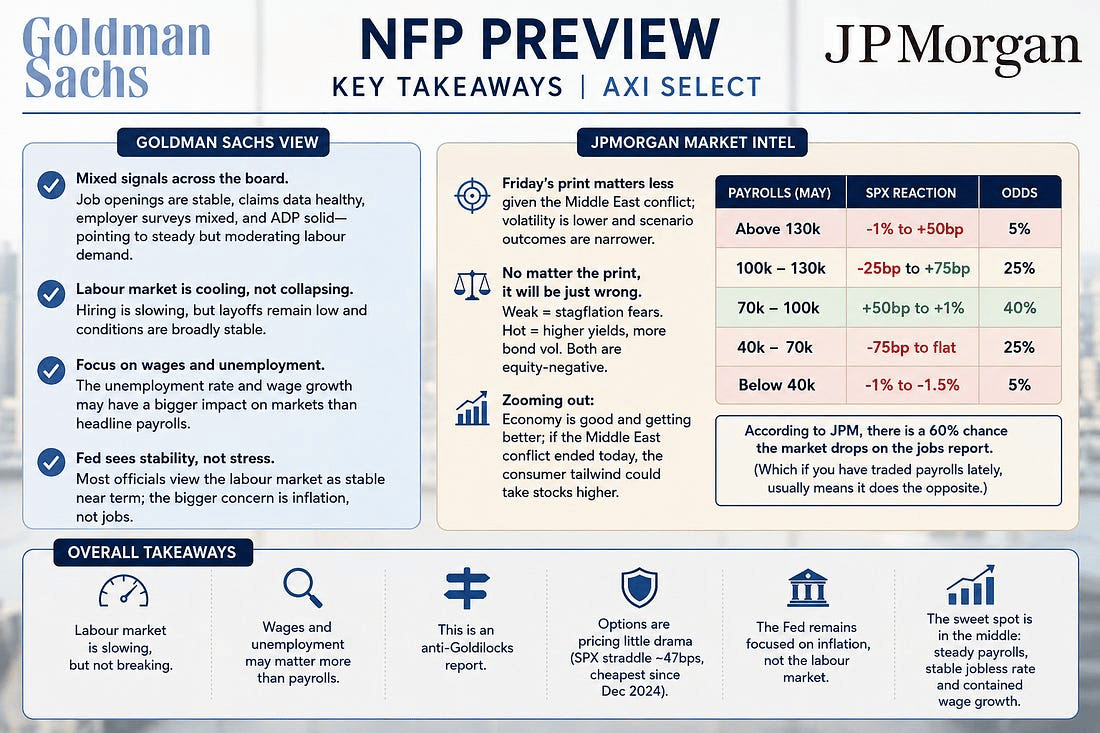

- The labour market is slowing, but not breaking. Most indicators point to a gradual cooling in hiring rather than a sharp deterioration in employment conditions.

- Wages and unemployment may matter more than payrolls. A stable jobless rate and moderating earnings could be more important for markets than the headline jobs number itself.

- This is shaping up as an anti-Goldilocks report. A weak print risks reviving stagflation concerns, while a strong print could push yields higher and pressure equities.

- Options markets are pricing very little drama. With the S&P straddle near its cheapest level for an NFP release since late 2024, the risk may be that investors are underestimating the potential for a larger move.

- The Fed remains focused on inflation. Policymakers broadly view the labour market as stable, leaving energy prices, tariffs and inflation expectations as the primary drivers of the policy outlook.

- The sweet spot remains somewhere in the middle. Payroll growth that is neither too hot nor too cold, combined with stable unemployment and contained wage growth, remains the outcome most likely to support risk assets...

Author

Stephen Innes

SPI Asset Management

With more than 25 years of experience, Stephen has a deep-seated knowledge of G10 and Asian currency markets as well as precious metal and oil markets.