What will Q2 earnings season show?

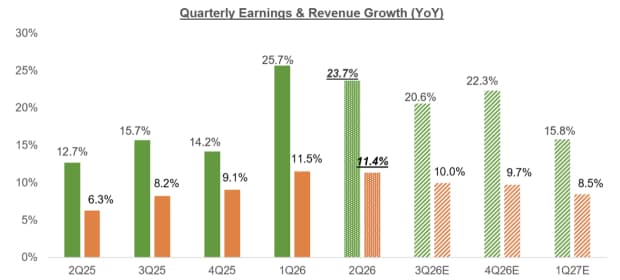

Total S&P 500 earnings are expected to increase by +23.7% in the June quarter from the same period last year, on +11.4% higher revenues.

The chart below shows the Q2 earnings and revenue growth expectations in the context of where growth has been in the preceding four quarters and what is expected in the coming three quarters:

The revisions trend remains positive, as we have experienced in the last two quarters as well. Aggregate earnings estimates for the S&P 500 index have steadily moved higher since the quarter got underway in April, as the chart below shows:

Q2 earnings estimates have increased for 5 of the 16 Zacks sectors since the quarter got underway, which offset negative revisions at the remaining 11 sectors.

The Energy sector has enjoyed the most obvious earnings outlook upgrade, with aggregate earnings estimates for the sector up more than +90% since the start of April. Earnings for the Zacks Energy sector are currently expected to increase by +126.9% from the year-earlier period. Other sectors enjoying favorable estimate revisions include Tech, Basic Materials, Utilities and Business Services.

Excluding the positive revisions to either the Energy or Tech sectors, the aggregate Q2 revisions trend would have been negative.

Of the 11 sectors whose estimates have been under pressure since the start of April, the ones experiencing the most negative revisions are Transportation, Medical, Consumer Discretionary, Autos and Construction.

The chart below shows the overall earnings picture on a calendar-year basis:

The revisions trend for full-year 2026 is even more positive than we noted in the case of Q2, with estimates for 11 of the 16 Zacks sectors going up since the start of March. The Energy, Tech and Basic Materials sectors are the most notable beneficiaries of an improving earnings outlook, but estimates have increased across the board.

The sectors that have suffered negative estimate revisions since the start of March are Transportation, Autos, Consumer Discretionary, Consumer Staples and Medical.

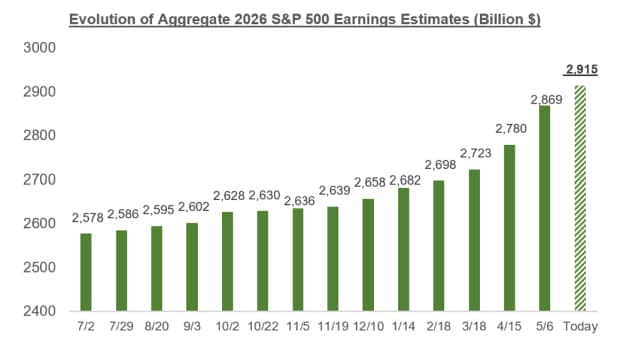

The chart below shows how full-year 2026 aggregate earnings estimates have evolved over the past year:

2026 Q2 earnings season scorecard

The Q2 earnings season will really get going when JPMorgan (JPM) and other major banks come out with their quarterly results on July 14th. But officially, the Q2 reporting cycle has already started, as companies with fiscal quarters ending in May have been reporting quarterly results in recent days, and those fiscal May-quarter reports get counted as part of the June-quarter tally.

Through Friday, June 26th, we have seen such fiscal May-quarter results from 13 S&P 500 members, including bellwether companies like Micron Technologies (MU), FedEx (FDX) and others. We have another four S&P 500 companies with fiscal quarters ending in May on deck to report results this week, including Nike (NKE) Constellation Brands (STZ) and others.

Total earnings for these 13 companies are up +179.5% from the same period last year on +29.5% higher revenues, with 84.6% beating EPS estimates and 69.2% beating revenue estimates.

The comparison charts below put the growth rates for the companies that have reported with what we had seen from this same group of companies in other recent periods:

The comparison charts below put the Q1 EPS and revenue beats percentages for this group of companies relative to what we had seen from them in other recent periods:

Want the latest recommendations from Zacks Investment Research? Download 7 Best Stocks for the Next 30 Days. Click to get this free report

Author

Zacks

Zacks Investment Research

Zacks Investment Research provides unbiased investment research and tools to help individuals and institutional investors make confident investing decisions.